I look at that and I think what a shame.

Two years ago I was telling all my friends to get out of their banks stocks and wrestling with my husband to let me sell his. I have grateful friends.

I have been 100% out of the market for 15 months now and I am not yet ready to enter it again.

Good call. Make sure you know when to get back in!

Your panic in selling most of your stocks just proves that you are not emotionally detached from your investments. Kind of goes against what you preach; you're already talking about getting back in the market with systematic purchases, but then why did you sell low?

I don't see why you sold AMEX, BoA, Ebay, JPM, COP, pfe, and some others if you are still investing for the long term. I anything buy up some of those depressed stocks and then sell the higher cost basis on some of them for a write off. Looks like you're going to be carrying those losses forward for decades!

I am courious why you have not considered taking the opportunity to loading up on low cost index funds.....? Seems to me that one thing many of us have learned is that it is TOUGH to beat the market. With that being said, you may as well minimize the one thing we can control... costs.

MM thanks for providing this detailed assessment.

I'd like to echo what Ed said; the additional cost of active management is at least $10,000/yr on your portfolio. Couldn't you just invest in VTI, VWO, VEU and BND exchange traded funds? Your record-keeping would be so much simpler and your after-tax, after-expenses returns would almost certainly be higher.

MM - in a comment to your 'annual update' you said you lost about 20% during the year. But, the loss you're showing above of $217,551 divided by your beginning actively managed investments of $706,212 (excl cash) is a loss of more than 30%. Even at this loss, you did have a better year than the indices. Have you been tracking your performance vs. benchmarks?

CPA1298, thanks for the question. A better way is to include the cash position too (it is a conscious decision at the start of the year to keep a higher-than-benchmark cash position). So it is $218k/$864k (or closer to $900k considering the cash that was generated from savings throughout the year).

No, i haven't calculated my performance vs benchmark.

You should not take into consideration your cash balance (earnings you made during the year from your job and side business). That should be excluded and only market securities counted when you compare gain vs loss. So you are in the 30-40% loss range like everyone else. If you are making $200k in cash from the job and side business you just made up for all your loss. In the given year you can say. I only lost 5%, but that is not true when you measure the performance of your securities. Which is what most of the people visiting this site are looking at, not your cash balance as if you were a company but rather your "investment" portofolio.

Dan, I respectfully disagree. Unless you are saying cash is not part of the asset allocation picture. Do you think Morningstar should strip off cash impact from those fund managers who consciously keep a lot of cash last year? And if we go down this line, shall we draw the line on money market funds, short term fixed income funds, or something else?

Anyway, yes, I lose 30%+ if I only count my stock and fund investment (and it is a valid yardstick in itself for stock or fund picking skills), but fortunately I didn't lose the 30% of my total net worth :-) The latter is probably what it counts for long-term survivorship.

Deborah, you have me by one month. I exited the market completely in December 2007, although I have put almost 20% back into the market over the past few months.

Damn crisis! Thanks for information. I think it is going worse next months.

|

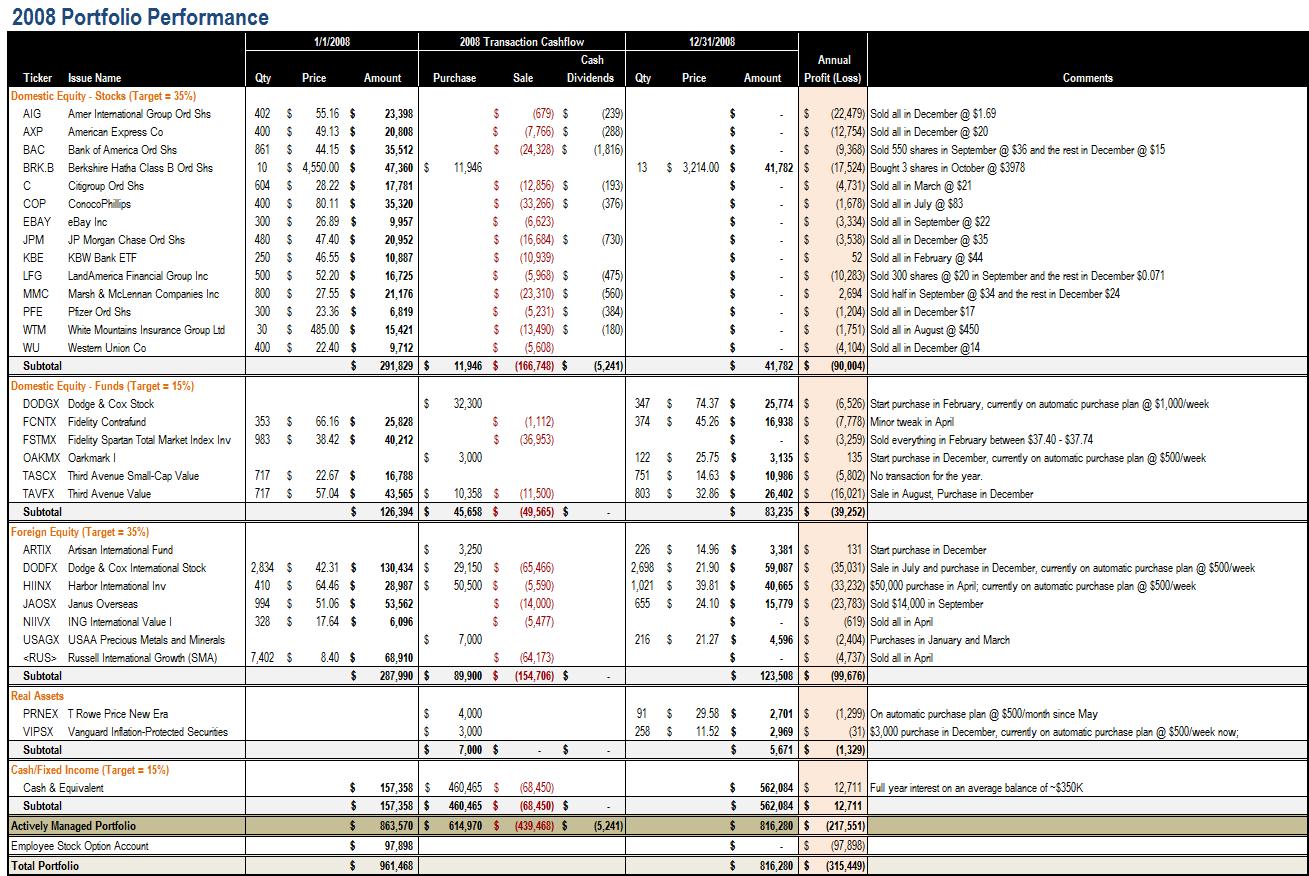

As a farewell bid to 2008, I compiled a full reconciliation table of the investment gains and losses in the unfortunate year of 2008.

As a farewell bid to 2008, I compiled a full reconciliation table of the investment gains and losses in the unfortunate year of 2008.