Approximately one year ago, there was a time when I was glued to the social personal lending site Prosper.com every morning, seeking and funding good loan proposals. In a matter of a few months, I underwrote 163 loans with a total of $14,880 at an average interest rate of 17.6%. I was hoping to make double-digit returns on my cashpile, satisfy my loan shark ego, and, maybe, benefit one soul or two in this world who will either use my fund to pay for grandkids' tuition, or start up a garage business. (PFBlog report: here, here and decided to stop lending any more back in September. It seems that I made the right choice -- the performance of my loan portfolio only went downhill from that point on.

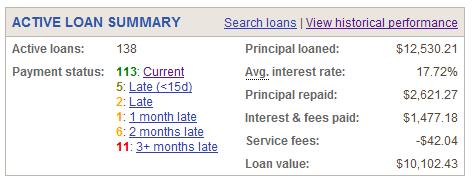

Out of the total 163 loans I made at Prosper.com, 25 borrowers have repaid the full balance. The rest 138 loans? 25 loans are at some stages of late payment, including 11 loans that are already more than 3 months late, and another 6 over 2 months late. Total principal exposure on delinquent loans (late by over a month) is $1,300.

If not for the high interest rate I demanded in the first place, my microloan portfolio would be an investment loss. Thanks to those who have been honoring their payment obligations, my Prosper.com portfolio still books a 4.4% gain even if I wrote off all delinquent loans. This is, of course, not what I was praying for when I indulge myself into the loan shark pipe dream a year ago -- a simple investment into money market funds will yield even a bit higher return, with much less time investment, and less tax trouble. (The tax trouble: I have to pay tax on the 18% APY returns, but cannot legally write off the losses until the corresponding loans are considered defaulted.

Anyway, I'm glad I only paid a small tuition (in terms of opportunity cost) for an interesting experiment. Will I try things like this again next time? Maybe.