Double digit gains in all your stock positions is very impressive. What criteria do you use when stock picking?

Also, you you to be very well diversified in all your holdings.

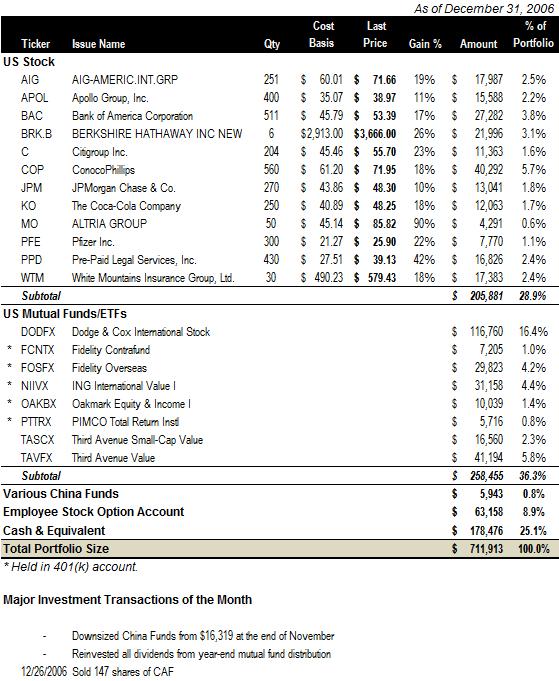

If my math is right, your current STOCK portfolio is up $35131.62 or 20.57%

Looks like it is heavy on dividend payers

few comments/questions...

1) is your stock options account vested, current appreciation, or exercised?

2) probably will do this in future months but the delta on the investments would probably be interesting.

3) interesting that you have quite a bit of interational exposure. you at all thinking about notching that back or increasing?

4) the 178k in cash and equiv seems fairly high. given your age, sticking it into a "conservative" mutual fund would probably yield better results.

5) may also want to shift things around - e.g. having more international in your 401k given the higher appreciation rate, and moving the OAKBX allocations outside of the 401k since it is a bit more conservative - i also hold this and it is a absolutely solid mutual fund returning 10-15% on average.

6) noticed that you have quite a bit of your portfolio in financial services - AIG, BAC, JPM, and C... did you recently do this or have you been doing this all along. with the exception of C, all of them seem to have done well in 2006. given the consolidation currently going on, i suspect that they will continue to do well in 2007.

7) as with you have been up until recent, i've been rather bullish on the china market. yes, it appears to have STARTED to cool but i believe the apac region is still pretty decent. check out MAPTX - decent diversification across apac.

DrChunger:

1) Stock option account only includes the value of vested but unexercised options.

3) I think I'm at the right level -- Buffett educated us that exposure in interntional equity earns from both the stock appreciation and dollar depreciation.

4) Yes I'm considering that ... actually I didn't realize I stashed such a big cashpile until I tabulated my portfolio yesterday. On the other hand, 5% risk-free isn't too bad too.

5) Will think about that.

6) I started my position in AIG in May 05 and added BAC and C in November/December 05 (after I sold my house). JPM was bought fairly recently -- August 06. I believe they will all do great ... I'm considering to add more AIG now.

7) Yes, I pocketed 40% return on CAF in a month, and all my domestic funds are doing great too. However, I think the bubble is about to burst (market P/E is close to 30 now; blue chips are trading at 40-50 P/E), so I'm playing it safe (of course I wished I rided the 100%+ gain in 2006 but I only tested water starting in August). Thank you for the MAPTX recommendation.

MM - I think in #6 above you are refering to May/November/December of 2005? Isn't that when you sold your house?

I'm surprised that I don't see much/any indexing in your portfolio. I assume you don't want to start a debate on whether or not to index, but do you have a few quick thoughts? In 2006 index funds beat 81% of the actively managed funds, and 40% in 2005. My theory on this is that the un-transparent and lightly-regulated hedge funds have increased the efficiency of the market to such an extent that traditional managed funds are having a much harder time keeping up.

In any case, your portfolio is pretty awesome, if based on nothing but its sheer size and your age. At $630k, you have a net worth approximately 5.5x mine of $115k, and you're only a few years older than me (I'm 26). I'm looking forward to seeing how your 2007 turns out.

Thank you CPA1298 for commenting regularly. Yes, you are right that it is 05 instead of 06 ... one couldn't get my cost basis if one only buys in 06 -- I'm making make the correction.

On this indexing vs actively managed fund/stocks topic, I'm trying to write a post but haven't sorted out the structure of the post yet. In short:

1) First, I am a firm believer of value investing and do believe value funds can create a consistent alpha vs market performance with less risk.

2) One level further, for net worth increase, one needs absolute return instead of relative return, so marketing beating or not is not that important. As long as I can get 8-10% absolute return year in year out (which can be achieved by investing in companies with good fundamentals and low P/E), I'm a happy man.

3) While stock market over the long run can truly deliver 8-10% on average, we are talking about a long time span over decades and 8-10% is a bet on how the world (economy, geographic conflicts, technological breakthroughs) will shake out in the next few decades, and I admittedly don't have a crystal ball on that. I'm born pessimistic so instead of holding onto the religion of long-term stock market performance, I am feeling more comfortable clinging to some tangible things I can understand (good cash flow, good business, low P/E and P/CF).

Very interesting.

I was about to ask if you had an asset allocation plan / model, but understanding your preference for value investing, seems like you pick globally.

What are your thoughts?

Regards,

makingourway

mm, what's the 100k liability that drags down your net worth? Is it zero interest credit card debt?

regards,

makingourway

If you read my month-end summary, the $60k is zero interest credit card debt and about $30k is the accrual of tax liabilities on unrealized gains.

hi mark - congrats on having a great game plan and executing it in a robust manner.

i like how you have a very focussed portfolio and a healthy selection of mutual funds (which seems to have a value bent). coincidentally, your individual stock portfolio and mine have very similar names (in particular, c, bac, ko - the ones i don't own i have contemplated buying apol, berks, mo, pfe and will probably buy in the future).

one thing i have to comment on is your statement in a previous post that you don't think msft has a lot of upside because as a mega cap, it's p/e is 15x (ie, you said it is priced to perfection). i am not sure if i buy into this. wouldn't this apply to most of your core holdings then (wmt, c, bac, pfe, etc.) all of these are huge companies. moreover, i appreciate that a big company will not grow as much as a smaller company owning to law of numbers but i think if msft is trading at 15x (which is below market), i really don't see why msft can not outperform the market especially since it has enduring competitive advantages and favourable business fundamentals. big companies can still grow, albeit not as quickly obviously as their smaller brethens. i don't know exactly when the consensus growth rate of msft is but i suspect it is 10%. at 15x p/e, given its sterling balance sheet, great competitive advantages, huge cash generative capacity, i am not sure if i agree with your statement that big companies should treat at lower p/e (i would agree only in the absence of growth).

thanks

Would it be possible to include the purchase date or the holding period of a given stock so one can better assess the percentage gain.

MM - thanks for providing some insight into your investing philosophy. It sounds like at some time in the future you might be interested in fundamental indexes (see URL for a recent article below).

http://news.morningstar.com/article/pfarticle.asp?keyword=indexfunds&pfsection=Index

I completely agree with your predictions for future returns on equity investments. Personally, I think we're entering a 50 year window of nominal US equity returns averaging 6-8%, with developing markets returning on average 8-10%. The equity markets are simply too vast and liquid with too many participants to justify the kind of returns they generated in the past.

Did you calculate your internal rate of return (IRR) for 2006? I assume that the returns you reported are over the lifetime of the entire portfolio. The IRR will give you a better idea of how you did vs. the market this year and in past years.

mm,

If you don't mind which brokerage firm you use? Also do you own Dodge & Cox fund and Third Avenue funds in this brokerage account or directly with fund company accounts? I always try to keep my portfolio managment simple but these funds are not NTF funds per my knowledge like other value funds.

mm,

If you don't mind which brokerage firm you use? Also do you own Dodge & Cox fund and Third Avenue funds in this brokerage account or directly with fund company accounts? I always try to keep my portfolio managment simple but these funds are not NTF funds per my knowledge like other value funds.

MM - What brokerage firm do you use?

joewatch- Portfolio IRR for 2006 is about 12% ... i took this directly from MS Money.

kb- I pay $17.99 to buy DODFX and TASCX from Ameritrade. Both Fidelity and BrownCo (now ETrade) offer TAVFX as NTF.

MLB- Most of my portfolio sit between Fidelity and Ameritrade now.

re brokers, i use firstrade and love it. ntf on most funds. $7 stocks/etfs. no hidden fees.

MM,

What type of analysis do you run on companies before buying or selling stock? Also, what types of initial screeners do you use to narrow down potential future investments?

Thanks for sharing the details of your portfolio. I just started reading your site, but it certainly provides good motivation (and loads of information).

I get a few new ideas each time I visit.

Hi MM,

I have been a advid fan of your site for some time, but this is my first time posting. You are the one site I have always identified with. In addition to a wonderfully written blog, you are asian (as am I), work at microsoft (I do something similar), and aspire for more than just being "OK" by the time you retire. I hope to set my goals to your level and even higher possibly. Please feel free to stop by my site and provide feedback.

I have 2 questions for you. What are your goals with the BRK.B stock, and what is with the lack of vanguard (no-load, low expense) funds?

|