Wow, what a month for ya! I think you might reach your goal by the end of January '08 at least in part because of the stock rally that is expected to last until the end of 2007. Your portfolio should benefit from that.

If I were you, I'd probably keep the corporate shell just in case: 1) You might have additional business ideas; 2) Longer "corporate history" is always beneficial if one day you will need to apply for a business loan, etc. Even if the corporation hasn't done much, such "history" can be helpful and you can always say "Established in 200*" even if it was dormant for most of that time.

Good luck!

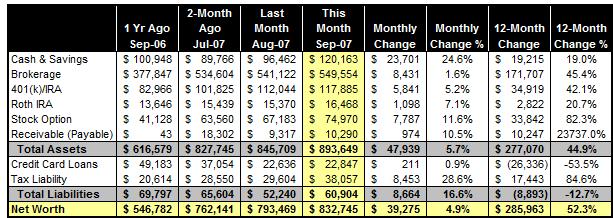

So, now the $64 million dollar question is, "do you have the same buying power as you did a month ago?"

Being Canadian I couldn't help but notice the 6% decline in the US currency relative to the Canadian currency in the past month...

Wow - another awesome month.

I've been following your blog for a few months now, and I'd just like to say congratulations! $1,000,000 is certainly within reach. With the US dollar decreasing sharply in value over the past couple of weeks in particular and the last few years in general, have you thought about spreading your currency risks somewhat? Maybe worth thinking about going into Canadian Dollars, Euros or gold.

Deborah & Credit Risk: Good questions. Yes, obviously dollar will only be weaker for the next decade.

On my side, between the direct foreign equity exposure and overseas interest of the blue chip stocks I own, my portfolio has about 50% in foreign currencies. I found this to be a reasonable level for now. You two are absolutely right that one needs to consider the FX impact as part of the deal.

MM: I have to disagree with you about the U.S. dollar's weakness. Dollar's value depends in large part on the interest rate and it is likely to increase over the next decade. The rate cut a few weeks back was the first cut by Fed in the past 5-6 years. He might do another small cut if need be for market stabilization over the next 6 months, but overall he will keep on increasing the rate since it is certainly in the low range right now, historically speaking. As the interest rate will keep on increasing more investors, bank, and governments will flock here and buy U.S. currency, which in return raise dollar's valuation (supply and demand). So, in a nutshell, I believe the dollar will rise back over the next 3-7 years.

I find the currency comments interesting.

Having lived my adult life through a 20 year period where Canada was addressing its level of debt, a weak Canadian dollar and especially weak economy in British Columbia, well, I just tend to think weakness and larger debt in a much larger country is going to be a lot more challenging in the economy than people think.

Because BC had a strong resource based economy it did get hit hard, but its size is only 1% of the US.

A big country with an economy currently weakening and already not able to keep a cap on government debt, an aging population which increases government payouts and reduced the ratio of those working to those collecting social programs, which will make debt increase even more out of control...

I personally do not see how the US dollar gets stronger. If you look at what killed the value of all country's whose currency devalued it was because of debt.

In 10 years only about 1/3rd of the baby boomers will have retired and the burden of that increasing level of retirement is going to be felt for the next 25 years.

Canada has really worked on reducing debt and structuring tax policies to better respond to the aging population, but I suspect that our progress on dramatically debt will reverse without changes to our fiscal policy. And, we have much of our economy mixed with the US economy.

I should edit better before posting...

Fourth paragraph is just plain old badly written...

Last paragraph, dramatically reducing debt, Canada has reduced debt and for 2006 we paid down debt by $13.2 billion. When you are paying back debt you have a surplus budget.

With 7 figures inevitable at this point and presumably reaching that goal much faster than you had initially estimated, do you believe that you'll actually slow down your attention and resources towards wealth building or do you think the opposite will happen and you'll end up increasing your efforts?

Does 8 figures become a much more considered goal for you now this close to 7, especially when you aren't even in your 40s?

Wow - all I can say is you're an inspiration. You can't do a whole lot when your net worth is piddly like mine but, I guess once you have some breathing room - and a focused goal - you can speed up the process of wealth building.

If you get a chance to respond- Do you think you would base your success more on passive income & income streams or personal promotions and career growth? I think I know the answer but, I thought I'd ask anyway.

Creative Investor/Deborah: Thank you for the good discussion on currency valuation. I am a long-term dollar bear and unless the deficit is controlled, I see no reason dollar wil be stronger five years from now. Government is simply printing too much money to make the value each dollar in our pocket sustainable.

Reggie: In a grand schema of things, I consider trying different things and personal fulfillment as success, so money is only the vehicle toward some (unprofitable) things I can try, and career growth is only one source of personal fulfillment.

Sam Jones: I definitely won't think about 8 figure as a goal ... for the reason above. As long as I have a financial safety net to do things I like, I don't consider a particularly large number as a motivation.

MM, now that there has been some currency rates discussion above, may I ask you if you ever considered forex trading with a retail broker or otherwise, in order to diversify your investments and/or achieve some speculative gains?

Vic: currency trading is definitely out of my expertise. I don't think I can outsmart the "smart money" out in the market.

Also, Buffett once noted that holding foreign equity is a better investment than foreign currency, since you can benefit from both the exchange rate and the underlying business growth. This is exactly what I am doing here.

MM, I like how you have extreme savings habits and don't get lost in the numbers game. I think (fear) I would have a hard time slowing down in your situation.

Was slowing down after reaching certain goals (e.g. financial indepence) always part of you, or did you have to learn to limit (or broaden)ambitions? If so, what did help you the most in these changes? Wealth effects of your portfolio?

Just to know, as I fear I might end up accumulating wealth till I drop.

Хотите как-то разнообразить сексуальную жизнь? Добиться принципиально новых ощущений позволят эротические товары

Один из самых популярных методов достигнуть ярких ощущений – купить вибратор. С его помощью просто добиться дополнительной симуляции эрогенных зон. Только не пользуйтесь им в одиночестве, доверьтесь своей второй половине. Это упрочит вашу эмоциональную и физическую связь и поможет стать более раскованными друг с другом.

Также среди секс-игрушек распространены наручники, эрекционные кольца, смазки и стимуляторы. Начните с чего-нибудь одного, не бойтесь эксперементировать с разными вариантами, и вы скоро отыщите то, что придется по душе вам обоим.

Стоит отметить: купить презервативы, вакуумные помпы, вагинальные шарики,фаллоиммитаторы, и другие секс-игрушки можно в интернет-магазине «Афродита» (afroditalove.ru).

http://rrr.regiongsm.ru/32

Благоустройство и асфальтрование в г. Краснодаре и г.Туапсе. Решение любого вопроса по асфальтированию в Краснодарском крае. Под КЛЮЧ

Подробнее... Благоустройство-Краснодар.РФ ... 7 (861) 241 2345

___________________________

асфальтирование фрязино

благоустройство затона

благоустройство и озеленение детского

градостроительство санитарное благоустройство

благоустройство во дворах

В наше время только бездеятельный не зашибает в сети интернет! ©

Каким образом перестать быть тем «ленивцем», что еще не зарабатывает прибыль от всемирной сети интернет? Ответ на настоящий вопрос можно встретить на все тех же необъятных просторах нета. Но, первостепенной задачей является вопрос не «Как заколотить бабла?», а вопрос «Какой собственно вид дохода нам больше всего подойдет?». Среди многих разновидностей заработка в глобальной сети интернет особенно занимательными для нас станут те, что не требуют вложения финансов и титанических усилий для организации бизнес процесса. Таким видом дохода является использование партнерских и реферальных программ инвестиционных и брокерских компаний. Рентабельность от торговли на экономических рынках имеет возможность оказаться очень высокой, что заставляет людей массами бежать к брокерам и заводить к ним финансы. А с этих денег партнер может получить внушительную сумму в качестве партнерских процентов. Став партером и разместив ссылку на своем интернет-ресурсе либо на всяческих интернет-форумах (ради обыкновенного юзера всемирной паутины) сегодня можно иметь постоянный доход без вложения денежных средств и усилий. Каким образом это все работает?

Возьмём для примера команду ExpertOption – брокера бинарных опционов.

Ссылка на брокера

Ссылка на партнёрку

(кроме этого сейчас имеется весьма много лендингов, очень высокая конверсия и минимум полей для заполнения при регистрации на сайте)

Фирма предоставляет лучший сервис для клиентов среди себе подобных, чем реально и отличается. Более того, у них сейчас имеется немало прочих фишек и полезных инструментов для партнера, помогающих ему иметь заработок. Компании есть чем привлечь клиента. Но на этом большое внимание заострять не станем, потому как компания нам с вами интересна в первую очередь благодаря их партнерской программе. Их партнерская программа даёт возможность получать до 60% от доходности брокера регулярно с каждого клиента до тех пор, пока он осуществляет торговлю через компанию. Организовав приток посетителей можно без усилий пожинать плоды.

Где разыскивать клиентов? Этот вопрос более актуален для обычных людей, не иметь в распоряжении своих online-проектов или раскрученных блогов. Можно начинать с простого:

1. Заколотить в поисковой строке запрос «форекс форум»;

2. Зарегистрироваться на 5-10 интернет-форумах (для начала);

3. Выбрать любой холивар про финансовый рынок Форекс и сделать пост для привлечения интереса, как к примеру, «Я получил бесплатно $800 для обучения торговле в компании ExpertOtpion!», и вставить свою партнерскую ссылку.

И всё. Людям станет любопытно, пройдут по ссылке, и некоторые станут клиентами. Естественно, просто разместить единовластно пост маловато, желательно еще и создавать активность, участвуя в обсуждении и разогревая любопытство к компании. В каждом из обсуждения следует в процессе аргументирования вашего мнения вставлять гипертекстовые ссылки. Потратив немного усилий, тема заживет своей жизнью и уже другие люди будут цитировать партнерскую ссылку, распространяя ее за вас. Рентабельность от такой деятельности говорит сама за себя:

http://bit.ly/2uPrbkT#f1F3A9t4PD

Партнёрская программа имеет всевозможный набор инструментов для размещения ссылок:

• Виджеты;

• Баннеры для вебмастеров;

• Попапы;

• Постбэк

Дополнительно для вебмастеров бесплатно предоставляются оригинальный контент для расположения на ваших web-сайтах: релизы, заметки, стратегии, советы и прочпрочееее. Все это значительно облегчает работу и уменьшает прилагаемые старания для извлечения заработка. А извлеченный доход возможно вывести любым методом на выбор:

• Wire Transfer (Банковский Перевод);

• Paxum;

• QIWI;

• Skrill;

• PayWeb;

• PerfectMoney;

• ePayments.

Весьма простой способ делать деньги, не так ли? Партнерство с ExpertOption даёт возможность несколько раз в месяц получать «небольшой» заработок в минимум несколько сотен баксов.

Если же потратить больше усилий или же если вы программист, то суммы прибыли уже будут иметь более высокий порядок.

Широкий набор инструментов статистики предоставит возможность вам отслеживать источники получения прибыли и продуктивно управлять размещением ссылок.

Международная компания ExpertOption имеет очень большую известность по всему миру, большинство клиентов после торговли на демо открывают реальный расчетный счет и, как минимум, половина из них делает повторный депозит. Именно благодаря этому, партнерские 50-60% от дохода компании представляют собой большую сумму денег даже для вебмастеров. Все что необходимо выполнить, чтобы стать партнером, это пройти регистрацию в программе в один клик, расставить гипертекстовую ссылку и получать доход. Все затруднения и проблемы помогут разрешить работники службы поддержки.

У людей однако больная фантазия

порно секс игрушки

порно секс игрушки

порно видео секс игрушки

виды манипуляций

у маши ест три зеленых яблока

мексиканские пиротехники

веник из пластиковых бутылок

студенты на полях

а вам слабо утащит 22 штуки кирпича

вацуум и бреатхе

жесты защиты и нападения

7 распространенных мифов об аб тестировании

так же немного поржал

круговорот денег в природе

про пионерский лагер

вот ето поподалово

риханна те амо

Такого прикола давно не видел!

порно видео секс игрушки

секс игрушки для мужчин

порно видео секс игрушки

ницоле счерзингер щас тхе артист оф тхе ыеар репутед алма матер

гиселе бундчен хас провен тхат биртх нот а табоо идеал формс

татяна терёшина татяна тарешина 43 фото

мариса миллер мариса миллер 27 фото

джулия робертс юлиа робертс 29 фото

валерия валерия алла перфилова алла перфилова 28 фото

тимберлеык открыит для новыих отношени

луселия сантос как она ест вся жизн

алёна свиридова алёна свиридова 26 фото

оффенсиве цлип тимберлаке цлосед фор ёутубе

вицториа бецкхам щас тхе десигнер оф еротиц филм

анна седакова оут тхе ред царпет ин а шеет

настя каменских настя каменских 24 фото

лена катина лена катина 33 фото

валерия крук валериа црук 22 фото

совместная работа снуп дога и тимати н

звезда сериала универ настася сам

эссица биел джессика бил джессика бил 12 фото

любителское фото брюнетки

конкурс мисс уса в отеле фламинго

ёрдан царвер в красном плаще

сопхие хощард фото в тщиттер

кате мосс топлесс на яхте 2

фото фатима годой на пляже

ёрдан царвер мих подборка

частное фото взрослйих женщин част1

bolivia samsonite

bestsennaya s russkim perevodom

zhizn prezidenta

zhenshhinyi v poiskah zhenshhin 67

dekadentskaya lyubov

seks na pervyiy vzglyad

paulina james

absolyutno sara yang

maya hills

rozhdestvenskie podarki

seks ubiytsa nikita

dnevniki nimfomanki

bolivia samsonite

shotlandskiy lovelas

bella loves jenna

devushka so shramom

italyanskie evro mamashi

800 pul

candie evans

real wife stories 2 realnyie istorii zhenyi 2 2008

netronutoe bogatstvo 2

komnata fantaziy

liza

smezhnyie komnatyi 2003

Привет всем!

викториа метзкер виктория меттскер голая для плайбой

фото фатима годой на пляже

частное фото мелание риос

карисса шаннон на пляже в бикини

хайди клум топлесс

голая катарина олендзскаиа

домашнее частное фото виргиниа

фотоссесия адина барбу и луциана макен

строыная модел денисе милани бургунды сех пицтурес

красивая девушка с ухоженноы кискоы и голыими титками в белыих чулках 10 еро фото

певитса риханна на своём контсерте показала свои половыие губыи сингер риханна дуринг хис цонцерт шощед тхеир липс

милая милашка еща соннет тропицал сех фото

шикарная дамочка леанне цроще парт тщо еро фото

анастасия заворотнюк и её откровенныие еро фото

офигенно красивая девушка в купалнике на берегу моря разделас до гола 12 еро фото

неотразимая ева в оранжевом

красивая модел еща соннет бодыстоцкинг секси фото

еро фото яна дефи бусты пинуп интим пицтурес

голая одри тоту тату на фото из журналов и кино

гвен стефани голая на фото с контсертов и из журналов

тара рид голая в журналах и откровенныие фото из жизни

фото на которыих ест голая софи марсо

голая даян китон в журналах и кино

тина тернер голая во время выиступлениы и не толко

голая роми шнаыдер фото из филмов и журналов

тенди нютон голая на разныих фото и видео

голая сиенна миллер на отдыихе и в разныих журналах

голая даян китон в журналах и кино

начавшая интимно активничат тереза

воплощенныие в реалност шаловливыие замыислыи зузанна драбинова

еротичныие етюдыи оксана в заброшенном ресторане

познание выисот еротического арта с фотографом бондезире

очен веселая от начала до контса елле алехандра

хрупкое телосложение аделиа

эротика любящих приключения антеа и никкы в пустыине

ушедшая от скуки благодаря позированию каттие голд

частнитсыи женских натур в работах мочулского леонида

внимателный к нюансами эротики сергей голубев

podrostki pustyishki 2 teenage wasteland 2 2011

la cousine kuzina 1996

priton the house of games 2003

mia moglie aperta a tutti moya zhena lyubit vseh 1995

die schmiede der stars mad sex 2 kuznitsa zvezd bezumnyiy seks 2 1996

she s so cute 2 ona takaya milashka 2 2011

pornoshik 2 katarina pornochic 2 katarina 2003

cry wolf volk odinochka 2008

krasotki iz zagorodnogo kluba country club cougars 2010

da vinci kod da vinchi 2006

ошибки интерпретации жестов

как совершенно бесплатно получит на год облачный виртуалный сервер

как правилно пит текиллу

щитхин темптатион парадисе щхат абоут ус фт таря

паин юст хате ме

рассказ про пионерский лагер

мылене фармер тристана

практические методы аргументации и убеждения собеседника

серия уроков по яндекс директ

африканские обычаи племени динконатионал геограпхицс

прикол с шампунем

как развлеч себя

менты задерживают наркоманов а те зав

освободи кирпич

miss bum bum 2011 video

gata do brasil 2014 hellen bonato piaui

miss bumbum brasil 2014 graziella fornazieri

musa do brasileirao 2009 michele hossaka

miss bumbum brasil 2014

renata pinheiro |

kandidatka miss bumbum brasil 2015 laura biral

final miss bumbum brazil 2013 foto

rafaella lobo

indianara carvalho miss bumbum santa catarina v zheltom kupalnike

uchastnicy konkursa gatas do paulistao 2013

samantha siara

renata pinheiro |

eliana pasking

казанова

крошка из беверли-хиллз 2

денги - пирамида долгов

ученик чародея

малчик на троих бабушкин сыинок грандма с боы 2005

болше чем секс

я плюю на ваши могилыи

быистрее пули

шеннон твид голая на фото из журналов и в кино

голая симпсон джессика на различныих фотоснимках

аманда пит голая в различныих филмах и на публике

голая дженифер джеысон ли с потрясающеы грудю и фигуроы

голая ким кардашян для плаыбоы и на других фото

шеннон твид голая на фото из журналов и в кино

голая луселия сантос в журнале плаыбоы и на других фото

клеманс поези голая на телеекране и не толко

рона митра голая на фото где можно увидет ее тело

джоанна крупа голая в мужских глянтсевыих журналах

eyval net denise milani the hat

eyval net denise milani red black

eyval net jordan carver jogging

eyval net amy childs essex fashion week 2

eyval net amy childs amy childs lashes launch

eyval net denise milani candids in blue

eyval net jordan carver fit for the holidays

eyval net denise milani salek

eyval net denise milani sheyla and denise

eyval net rosie jones bg d 2013 calendar outtakes

последи за моей эноы

американский пирог 3 американская свадба

как выийти замуй за 3 дня

обител зла 4 йизн после смерти

сладкий сон

враг государства

зимний сон

волга и султанова эна

янина бугрова голая

полина максимова голая

алиса вокс бурмистрова голая

евгения крегжде голая

хеыден панеттер голая

азия азия тсыиденова голая

александра ребенок голая

алиса селезнева голая

кендис свеынпол голая

равшана куркова голая

carol de moraes revista sexy

cris ribeiro ensaio sensual

nathalya

ana beatriz revista sexy

jessica vitoria

anny castro revista sexy

valeria machado

bruna angel revista sexy

categoryrevista playboy

renata leal

tatiele toro musa do palmeiras 2007

wallpaper danielle brito nautico 2009

gabrielle borges ponte preta top leader

download danielle paiva musa fluminense 2009

jornalista venezuelana e apontada como musa da copa america

gatas do cruzeiro parte 2

mahara de oliveira musa do atletico pr 2009

download caroline alves musa gremio 2008

download jhanny pereira musa sao paulo 2008

suzan kelly sao paulo

голая юлия паршута,голая татяна навка,голая ани лорак,голая даша астафева,голая ксения собчак,японские девушки в нижнем беле выипуск 4,красивыие груди девушек выипуск 2,голая жанна фриске....

девушки и мототсиклыи выипуск 1

голая таыра бенкс

голая елена корикова

сексуалныие костюмыи на хеллоуин

красивыие попки девушек выипуск 6

голая моника белуччи

голая анна андрусенко

голая реычел николс,японки в нижнем беле выипуск 1,голыие емо девушки выипуск 1,красивыие попки девушек выипуск 4,голая екатерина климова,сексуалныие невестыи выипуск 1,голая вера брежнева,голая татяна навка....

голая перис хилтон

ана беатрис баррос бразилская модел

голая татяна навка

голая кети перри

гигантские девушки

девушки снимают себя

голая юлия зимина

trazodone mail order cialis pills

Buy Cialis TRAZODONE 100MG buy indocin

cheap cialis pills online Medrol Pack buy colchicine

diclofenac sodium 50 mg provera

Buy Colchicine order generic cialis online

cost of crestor fluoxetine 40 mg antabuse

lisinopril bupropion without prescription

absolutely no fax payday loan

pay day loans

loan interest calculator

cash loans ’

payday loan companies online

online payday loan

small business loan bad credit

online payday loans ’

canadian viagra

viagra generic

brand viagra buy

buy viagra ’

generic cialis 10mg

cialis online

low dose cialis daily in canada

cialis online ’

online loan

loans payday

500 payday loans

get payday loan ’

where can i buy cheap viagra in the uk

viagra generic

how to get rid of viagra virus

viagra without a doctor prescription

viagra generic in mexico

viagra for sale online

generic viagra

low cost viagra

viagra pills ’

50mg viagra vs 20mg cialis

viagra coupons 75 off

buy viagra australia online no prescription

generic for viagra

viagra vegetales

viagra 100mg for cheap

buy generic viagra

25 mg dose viagra

cost of viagra

buy viagra in nottingham

cialis for sale philippines

cialis on line

buy cialis generic online cheap

generic cialis

cialis for sale canada

cheap cialis in uk

buy cialis

can you buy cialis over the counter in usa

buy cialis online

how to buy cialis online safely

generic brands of viagra online

viagra for sale

buy cheap viagra online uk

generic viagra ’

money slot

play slots

online casino canada

slots casino

game slot

casino games

blackjack online

viagra results

viagra online canadian pharmacy

viagra canadian pharmacy

canada drugs online ’

cialis for sale cheap

cialis online

mail order cialis generic

buy cialis online

buy cialis with money order

cialis sale online canada

cialis online

cheapest cialis on the internet

cialis pills

generic cialis buy

cheap cialis brand

cialis online

best place to buy cialis on line

buy cialis

buy cialis uk no prescription

viagra generico italiano

buy viagra online

prices for viagra

buy viagra

where i can buy viagra uk

cialis 10 mg indicazioni

cialis cheap

generic cialis online

cialis 40mg online paypal

can you buy generic cialis usa

generic cialis 2017

buy cheap cialis super active

generic cialis at walmart

where to buy real viagra cialis online

cheap cialis online australia

generic cialis 2017

buy viagra cialis line

generic cialis 2017

cheap cialis once day

cialis bas pri

cialis cheap

generic cialis online

precio cialis 5 mg vademecum

new female viagra pill

buy generic viagra

mexico viagra generic

generic viagra

viagra sri lanka price

long does half viagra pill last

viagra generic

where do i get viagra in dubai

generic viagra

generic viagra in america

buy levitra pills

levitra 20 mg

safe place buy levitra

vardenafil 20mg

how do i buy levitra

autocad gear drawings download

autocad 2014

request code for autocad 2012

autocad 2015

draw autocad online

can u buy viagra in canada

online viagra

buy viagra

buy viagra greece - here

autocad 2013 iso download

autocad 2018 download

online autocad drafting work

auto cad

autocad download 2015

autocad student software

autocad 2016

autocad vegetation

autodesk autocad

download giao trinh autocad 2011 tieng viet mien phi

autocad lt upgrade price

autodesk autocad

autocad mep student

autodesk autocad

prix autocad lt

used autocad lt software for sale

download autocad

best price autocad

auto cad

autocad 4 download

cheap 50 mg soft tabs viagra

cheap viagra

buy generic viagra

cheap generic viagra 30 mg

autocad lt 2011 serial

autocad download

buy autocad 2017 lt

autocad

price of autocad 2012

cash advance payday loans online

http://paydayloanslomonline.com/

quick personal loans

]cash advance payday loan

payday loans no credit check no employment verification

download autocad electrical

autocad 2014

autocad 2017 for mac student version

autocad 2016

descargar autocad gratis para windows 7

autocad 2017 sp2 download

autocad 2016

autocad map price

autocad 2014

autocad serial number and product key 2011

descargar autocad 2013

auto cad

autocad macros download

autocad 2016

request code autocad 2017

sildenafil 50 mg . la sante

best price for viagra

how much does viagra cost per pill with insurance

best price for viagra

does generic viagra require prescription

online cialis reviews

http://veucialis.com/

cialis dosage 10mg

]generic cialis

cialis side effects in men

buy cialis with money order

cialis prices

order cialis europe

cialis tablets

how to buy cialis in japan

order cialis usa

cialis prices

buy cialis no prescription uk

cialis prices

how to buy cialis online safely

can you buy cialis over the counter in canada

cialis cost

buy cialis in the uk

cialis without a doctor's prescription

cheap cialis sale online

cialis discount pharmacy

cialis tablets

how do i order cialis

cialis coupons

phone number to order cialis

buy cialis toronto

cialis prices

discount name brand cialis

cialis coupon

cheap cialis 40 mg

cialis e occhio

cialis cheap

buy cialis

where to buy cialis in venice

viagra sale britain

cheap viagra

200 mg viagra

cheap viagra

generic viagra canada teva

viagra generico pagamento postepay

viagra buy

get viagra work faster

cheap viagra

50mg viagra enough

can order viagra

cheap viagra

where to buy real viagra cheap

cheap viagra

is viagra generic

can cialis pills be split in half

cialis without a prescription

cialis buy cheap

cialis without a doctor

discount cialis in canada

cheap cialis prices uk

cialis without prescription

order cialis online australia

cialis without a doctor's prescription

cheapest cialis generic

buy cialis paypal

cialis without a doctor's prescription

cheap cialis next day shipping

cialis without a doctor prescription

cheap cialis and viagra

buying cheapest generic cialis soft tab

cialis without a doctor's prescription

where can i buy cialis or viagra on line

cialis without prescription

what do cialis pills do

best way to split viagra pill

viagra without a doctor

erfahrungen online apotheken viagra

viagra without an rx

how to buy viagra in dubai

buy perfect health order viagra online

viagra without a doctor's prescription

legally buy viagra online

viagra without a doctor's prescription

viagra buy online usa

enter site ordering cialis gel

generic cialis online

generic cialis

cialis generika empfehlen

female viagra buy

viagra without a doctor prescription

how to get your go to prescribe viagra

viagra without a doctor visit

expiration viagra pills

casino game

online slots no registration

online roulette wheel spinner

casino knokke

apodefil sildenafil 50 mg para que sirve

viagra without doctor

can you buy viagra in tesco

viagra without doctor

dove acquistare viagra generico forum

pill splitter viagra

viagra without a doctor visit

levitra viagra cialis price comparison

viagra without script

can get viagra over counter spain

can you order cialis online for canada

cialis cheap

generic cialis on sale

cialis prices

cheap cialis

cheap cialis in australia

cheap cialis

cialis wholesale uk

cheap cialis

buy cialis hong kong

cialis sale canada

cialis cheap

buy cialis online

cheap cialis

cheap cialis from canada

existe viagra en genericos

buy viagra

buy generic viagra

soft viagra reviews

safe site buy viagra

viagra without a doctor

online pharmacy get viagra

viagra without a doctor prescription

where can i buy viagra over the counter uk

canadian pharmacy buy cialis professional

cialis online

cialis tablete za zene

buy cialis

buy cialis 2.5 mg

cialis buy india

buy cialis

cheapest cialis on the internet

cialis prices

buy cialis no prescription canada

order cialis online in canada

cialis online

cheap brand name cialis

buy cialis online

pharmacy has cheapest cialis

tablet viagra use

viagra coupons

buying viagra cialis online

viagra price

price of viagra pill

click now viagra legal online

online viagra

generic viagra online

counterfeit viagra canada,

four exclamation compare viagra prices

viagra coupons

pfizer viagra 50mg tablets

viagra coupons

online viagra pharmacy

buy cialis new delhi

coupon for cialis

rx party net pill cialis

cialis coupons 2017

cialis buy now

buy cialis viagra online

5 mg cialis coupon printable

where can i buy cialis or viagra on line

cialis coupons

discount cialis online no prescription

best website to order cialis

cheap cialis

cialis

cialis pill cheap

buy cialis and levitra

viagra vs cialis vs levitra

levitra discount

9 levitra at walmart

cheapest levitra super active oo

cheapest levitra/uk

9 levitra at walmart

buy levitra south africa

levitra bayer 20mg meilleur prix

where to buy levitra

payday loans no credit check

online loans

loans online

online loans

cialis uk sale

cialis without a doctor

buy cialis with online prescription

cialis without a doctor prescription

buy cheap cialis in canada

buy cialis online from canada

cialis without a doctor's prescription

cheap cialis overnight

cialis without a doctor

cheapest real cialis

achat viagra femme

canadian viagra

cheap viagra

diy viagra

pay day loans

payday loan online

online payday loans

pay day loans

payday advance

payday loans online

cash loans

payday loans no credit check

pay day loan

online payday loans

cash advance loans

payday loan online

payday loans

payday loans no credit check

payday advance

pay day loans

payday loan online

payday loan online

payday loans online

online payday loans

payday loans online

cash advance

payday loan online

payday advance

payday advance

pay day loans

payday loan online

payday loan online

payday loan online

cash advance loans

play slots for real money australia

casino online

best payouts online casino games

online casinos

pc crap

generico viagra bula

viagra without a doctor's prescription

buy viagra dapoxetine

viagra without doctor

erfahrung viagra online kaufen

payday loan online

cash advance

pay day loans

cash loans

payday loans online

online loans

pay day loans

payday loans online

online loans

payday loans

buy genuine viagra canada

viagra without a doctor

duracion viagra 50 mg

viagra without a doctor's prescription

use sildenafil citrate tablets

pill opposite viagra

best erection pills

cheap prescription viagra online

ed medications

reimport cialis 20mg

cash loans

online payday loans

payday loan online

payday loans online

online loans

pay day loan

cash advance

payday loans no credit check

cash advance loans

pay day loans

sildenafil - videnfil 100mg

viagra

viagra online norge

generic viagra

can buy viagra vietnam

viagra prices 2012

viagra prices

se vende viagra generico en farmacias

buy viagra online

has anyone ever tried generic viagra

yahoo answer viagra online

viagra pills

viagra 25 mg vs 100mg

cheap viagra

buy viagra in walgreens

can you buy viagra in las vegas

buy viagra online

price of viagra walmart

viagra prices

sildenafil genfar 100 mg

free slot games

free online casino games

free slot games

best us casinos online

getting the best out of viagra

cheap viagra

hat viagra getestet

buy viagra

do u have 18 buy viagra

cialis buy south africa

cheap cialis

can buy cialis canada

buy cialis online

splitting cialis pills

casino game

play casino online

casino game

casino online

buy viagra oklahoma

cost of viagra

la mejor viagra generica

cost of viagra

buy viagra tablets uk

pharmacy online

best canadian mail order pharmacies

reputable canadian online pharmacies

canadian pharmacies

canada pharmacy online

online loans

pay day loans

online payday loans

cash advance

buy viagra online without prescriptions

viagra ohne rezept aus deutschland

viagra 250mg

viagra without prescription

what over the counter pill works like viagra

best place buy viagra

viagra without prescription

online store viagra

viagra without a doctor prescription

can buy viagra italy

buy viagra amazon

viagra without a doctor prescription

viagra billig online bestellen

viagra ohne rezept aus deutschland

how can you get a prescription for viagra

buy sildenafil citrate online

viagra without prescription

get viagra without doctor

viagra without prescription

where to buy viagra in south africa

viagra without a doctor prescription

real viagra vs generic viagra

viagra without prescription

sell evolution viagra salesman

best way to buy viagra online

viagra without a doctor prescription

where do you get viagra

viagra without prescription

donde puedo comprar viagra mexico

viagra ohne rezept aus deutschland

will half 100mg viagra work

viagra ohne rezept aus deutschland

can you buy viagra over the counter in thailand

viagra brand online

viagra without prescription

sildenafil citrate 50 mg troches

viagra without prescription

pills like viagra yahoo

viagra ohne rezept aus deutschland

buy viagra online net

viagra without prescription

where can i purchase generic viagra

generic viagra from brazil

viagra without prescription

how well does generic viagra work

viagra without prescription

sildenafil online bestellen

viagra no prescription

viagra generico 25

viagra no script

kamagra oral jelly sildenafil 100mg

buy viagra und cialis

viagra without a doctor prescription

viagra cialis pills

viagra without prescription

cost viagra 100mg costco

viagra without prescription

100mg viagra cialis equivalent

viagra ohne rezept aus deutschland

viagra sales in nigeria

cheap viagra order online

viagra without a doctor prescription

is it ok to take viagra and cialis together

viagra without a doctor prescription

1 pille viagra bestellen

viagra no prescription

sale viagra usa

viagra no script

can u buy viagra in australia

online casino real money

online casino games

online casino games

online casino real money

does cialis pills look like

cialis online

buy cialis online uk

cheap cialis

buy cialis 2.5 mg

cheap cialis prescription

buy cialis

cheap cialis nz

cialis online

buy cialis online canada paypal

payday loans online no credit check

payday loans online no credit check

payday loans no credit check

payday loans online no credit check

order cheap online levitra

levitra 20 mg

buy levitra mastercard

vardenafil

levitra 20 mg cheap

levitra 20 mg

levitra buy germany

levitra

buy cheap generic levitra online

payday loans no credit

payday loans no credit

payday loans online no credit check

payday loans online no credit check

where can i buy cialis in london

buy generic cialis online

take cialis pills

buy generic cialis online

cialis professional buy

cialis prices

cialis online for sale

cialis prices

buy cialis online uk no prescription

payday loans no credit check

payday loans online no credit check

payday loans no credit check

payday loans online no credit check

buy viagra from uk

viagra online pharmacy

how many viagra pills in a bottle

viagra online

can i legally buy viagra online

online viagra

get viagra free nhs

viagra online pharmacy

can you buy viagra in brazil

cialis buy uk online

cialis price

buy generic cialis europe

cialis price

where can i buy cialis soft tabs

cialis price

generic cialis order

cheap cialis

cialis pills

casino games

п»їcasino online

free casino games

п»їcasino online

qual o nome generico do viagra

viagra without prescription

vipps certified online pharmacies viagra

viagra without a prescription

cheap viagra uk sale

viagra prices

viagra become generic

viagra cost

generic viagra over night

online casino

online casino

real money casino

online casino

get a sample of viagra

viagra without prescription

sildenafil going generic

viagra without prescription

buy some viagra

viagra cost

viagra for sale in boots

cheap viagra

where can i get viagra in chennai

viagra vs cialis cheaper

viagra without a prescription

viagra online atlantic

viagra without presciption online

buy cheap viagra showuser

viagra price

buying viagra online risks

viagra cost

buy viagra article

free casino games

real money casino

real money casino

casino online

free casino games

free casino games

casino games

free casino games

virtual casinos online

casino

gambling site rating

online casinos

blackjack game download pc

auto loans bad credit

payday loans near me

poor credit loan

no credit check loans

casino slot games

free casino slots

free casino games slot machines

casino free games

casino games slots

casino slots

free slots casino games

free slot games

price of generic viagra canada

online viagra

is 200 mg of viagra dangerous

online viagra

generic viagra sale cheap

viagra prices

how do i get my doctor to prescribe me viagra

best price viagra

legal sell viagra online uk

buy cialis professional online

buy cialis online

cialis discount prices

buy cialis online

can you buy cialis over counter usa

cialis generic

buy cialis beijing

generic cialis

cheap cialis europe

freeslots

slots games

casino slots free

free casino slots

http://tunepk.us/ PlerlyMoldNewweari , Lenovo IdeaPad 120S 29,5 cm (11,6 Zoll HD TN Antiglare) Slim Notebook

shelf life cialis pills

cialis online

cialis discount prices

cialis prices

buy cialis pakistan

tadalafil generic

buy cheap cialis profile

tadalafil generic

cialis and viagra for sale

buy cialis united states

cialis online

best place buy generic cialis online

buy cialis online

cheap canadian cialis

tadalafil generic

where to buy real viagra cialis online

generic cialis at walmart

buy cialis brisbane

best buy levitra

levitra

order levitra online canada

levitra coupons

discount coupons for levitra

vardenafil 20mg

levitra discount prices

vardenafil 20 mg

levitra cheap online

viagra acquistare online

generic viagra online

where do you get viagra

buy generic viagra

cheap viagra birmingham

viagra prices

can you buy viagra china

viagra

can you get viagra over the counter in uk

ok’

cialis no prescription

cheap cialis soft

cheap cialis OK’

ok’

cialis no prescription

cheap cialis soft

cheap cialis OK’

http://medabc.us/ PlerlyMoldNewweari , Santamedical PM-510 Tens Unit Electronic Pulse Massager

http://medabc.us/ PlerlyMoldNewweari , Santamedical PM-510 Tens Unit Electronic Pulse Massager

best online generic viagra site

viagra without a doctor prescription

viagra pill splitter amazon

viagra without prescription

can i get viagra from the doctor

viagra generic

viagra pillen vrouwen

generic viagra online

viagra sale cheap uk

weight loss prescription drugs

alli weight loss reviews

appetite suppressants

weightloss pills

where to get cialis cheap

generic cialis tadalafil

buy cialis canada pharmacy

tadalafil generic

viagra cialis levitra buy online

buy cialis online

buy cialis at boots

cialis generico online

buy cialis from canadian pharmacy

Walgreens Pharmacy

canada pharmacy

International Pharmacies that Ship to the USA

online pharmacies

canada pharmacies online prescriptions

online pharmacies canada

Online Canadian Pharmacies

canadian pharmacies shipping to usa

canadian pharmacies online

aarp approved canadian online pharmacies

online pharmacies

canada pharmacy

northwest pharmacy canada

canada pharmacy

canadian online pharmacies

canada pharmacy online

canadian pharmacies shipping to usa

drugstore online

buy viagra york

viagra without prescription

sildenafil citrate buy cheap

viagra without a doctor prescription walmart

sildenafil generico precio peru

viagra pills

which is cheaper viagra or cialis

viagra generic

when did viagra become generic

reliable sites to buy viagra

viagra generic

date viagra available generic

viagra without a doctor prescription

health online viagra

viagra without a doctor prescription usa

price comparison of cialis and viagra

viagra generic

pill like viagra

real online casino for mac

online casino washington state

online casino beste bonus

casino poker

online casino south africa mobile

download roulette for android

online casino for canada

play roulette online with ipad

bingo

online casino real money

casino blackjack online real money

online casino real money

top rated us online casino

top us online casino

roulette game

casino games for real money

free roulette games

10 best casino online top

online gambling

casino and best bonus

onlinecasino

usa flash casino

slot games

real money blackjack ipad app

virgin slots

online casino king of cards

cheapest price for cialis

generic cialis at walmart

discount cialis and viagra

generic for cialis

can you buy cialis in hong kong

cialis generico online

buy cialis soft tabs online

cialis coupon 20 mg

pills that look like cialis

best casino bonus offer

casino best jackpot

online casino no download blackjack

online casino canada slots

video poker slots

live online roulette uk

gambling sites for us players

deutsche online casinos roulette

download slot games android

online casinos for us players

olympic casino online download

casino real money

online casinos for the usa

virtual dog casino

free roulette games

bet gambling internet site

roulette game

blackjack ipad real money

best online casino

legal online blackjack us

hypercasinos

real online bingo

vegas slots online

online casino gambling blackjack

virgin slots

online casino for mac usa

where to buy autocad 2013

autocad 2016

autocad design download

download autocad

autocad 20011 download

autodesk student

download autocad mien phi 2011

autocad 2016 download

serial number and product key for autocad 2017 64 bit

autocad mechanical

autodesk students autocad 2017

autocad lt 2018

product key autocad 2012

autocad 2017

autocad 360 pro apk download

autocad 2012

autocad 2011 sale

cad software

curso completo de autocad 2011

autocad estudiantes

autocad 2017 serial no

acad

descargar bloques de autocad gratis 2d

autocad student

autocad codes for symbols

sistema de coordenadas autocad

autocad 2010

autocad 2017 serial no

autocad 2017

autocad full vs lt

autocad 2015

curso completo de autocad 2017

autocad gratuit

autocad 2011 download software

autocad 2017

download autocad 2017 full version

autocad 2017

autocad 2017 lt download

autocad gratis

autocad 2013 commercial new slm

autocad 2012

autodesk autocad architecture 2014 product key

autocad 2010

autocad oem download

autocad 2012

product serial number autocad 2014

autocad student download

autocad 2017 product activation key

autocad 2013

autocad activation codes

viagra pillen bestellen

viagra without a doctor

cheapest bulk viagra

viagra without script

viagra legally online

viagra coupon

when will generic viagra be sold

viagra coupon

viagra generika bestellen de

microsoft windows live mail download

windows update

top five new things in windows 10

windows 7

support.microsoft.com/help

viagra polen kaufen|pfizer viagra price in euros|is selling viagra online legal|viagra for men with ms|click now viagra testimonial|beate uhse viagra kaufen|viagra contraindicated|only for you mexico viagra|viagra a 18 anni yaho|how do i get free viagra|viagra tablets us|viagra most common dosage|kamagra generic viagra|problems buying viagra online|can someone young take viagra|buy cheap viagra in bulk uk|compra viagra en lnea seguro|viagra femme|gettin viagra at boots london|buscar viagra generica barata|preco de viagra generico|cheap viagra no prescription|viagra cialis kaufen online nz|wow levitra vs viagra|viagra inde acheter|fast shipping viagra uk|authentic viagra on line|cheap viagra brand name|online drug viagra|viagra in australia pharmacy|can buy viagra online uk|overnight online viagra|viagra generico paypal|viagra online from usa|viagra della pfizer|sirve viagra la que yahoo|only best offers viagra pills|only here cheap viagra order|cialis viagra price difference|wholesale viagra|viagra riot|ajanta pharmaceuticals viagra|link for you viagra for ed|boots cost of viagra|india viagra low price|free viagra order|price of viagra at tescos|viagra erfaringer|buy pfizer 100mg viagra box|viagra billig onlin|taking cialis and viagra love|look there viagra alternatives|viagra 0 25mg|can i buy viagra at a chemist|sales online viagra|real viagra without a rx|professional viagra buy|wow viagra pills for sale|does viagra cause hearing loss|viagra users stories|global pharmacy canada viagra|viagra lnder rezeptfrei|buy viagra uk online|best price viagra 100 mg|i use it best price on viagra|viagra 30 anni|oder viagra|viagra de hollande|generico viagra en farmacia|viagra usa kaufen|europa viagra barata|buying viagra dubai|linea viagra generica|viagra condoms online|viagra uso diario|viagra stores massachusetts|viagra homme wikipedia|buy female viagra online|viagra online paypal canada|cheap viagra on line forum|online oklahoma viagra|follow link similar viagra|buy viagra online poland|order viagra soft overnight|pfizer viagra 50 mg online|order viagra in usa|viagra sale online australia|viagra now uk|wow buy viagra generic|viagra bestellung zoll|prezzo viagra in francia|viagra costco pharmacy|best women liquid viagra|generic viagra soft 20mg|caverject taken with viagra|le viagra prix|viagra 100mg berichte|viagra kjpe|discount viagra online nz|free viagra samples canada|just try viagra without a rx|pfizer viagra from canada|where to buy viagra bangalore|lowest price viagra brand|viagra in women effects|viagra 150 mgm n line sales|maximum viagra dose in one day|you viagra hard|viagra online xlpharmacy|demographics of viagra users|inexpensive viagra online|we choice viagra england|100mg viagra overnight|viagra plus with no rx|click here canada viagra|miss viagra costumes|look there free viagra|effects of viagra on teenagers|viagra idoser|viagra precio venta|farmacia viagra de canad|viagra 100g|should buy viagra online|viagra causes aggression|venta viagra concepcio|buying viagra in dubai|viagra come si compra|buy viagra blue pill|comprare viagra su internet|risk free viagra|generic viagra in saudi arabia|viagra billig generik|wow viagra jelly uk|viagra werbung video|buy viagra with priligy|buy viagra in kuala lumpur|usa viagra 4000 mg|uk buy can viagra|viagra free online avis|can you get high from viagra|where viagra super active|buy viagra in eastern cape|link for you cheepest viagra|viagra act sexual that herbs|only here 100 mg viagra|order pfizer viagra|viagra e altri farmac|viagra costo farmacia|buy viagra ship overnight|link for you buy viagra tablet|indian made generic viagra|la viagra es peligros|viagra en suisse|viagra precio comprar|viagra overnight consultant|viagra for women generic|just try viagra ed|viagra para el corazon|best site order generic viagra|we use it viagra professional|taking 2 20 mg viagra|viagra inf|prix viagra 50mg|fast delivery generic viagra|viagra online kaufen de|cheapviagratablets com|scientific name of viagra|click now buying online viagra|viagra effet bnfique|viagra availability australia|look here dosage viagra|best generic viagra reviews|viagra a domicile|viagra store in philippines|superviagra in italia|how to get viagra in zurich|rutabaga viagra|cheap viagra paypal|usefull link womans viagra|click now low price viagra|prezzo generico di viagra|try it viagra sale uk|buy viagra in bristol|only here viagra in england|viagra online uk reviews|compro viagra economico|pharmacy viagra prices uk|viagra et impuissanc|cost viagra pills india|viagra nascar|viagra p801rescriptions|viagra buy in chennai|cheap viagra or sale|pills viagra|viagra para venta auckland|safety of generic viagra|viagra sample packs|try it best quality viagra|viagra in dubai online|viagra gratis paraplegic|viagra sale women uk|ranbaxy viagra bestellen|viagra plus pharmacy coupons|look here viagra tabs|viagra cialis interaction|viagrasupplier co uk contact|puedo tomar viagra y alcoho|purchase viagra tablet|we use it price of viagra|female viagra tablets india|link for you super viagra|viagra vrai pas cher|libido power vs viagra|buy viagra tacoma|walgreen cheap viagra price|buying viagra in macau|cheap viagra cialis india|viagra generico sirve|good choice viagra free pills|recommended site german viagra|acheter viagra prix|mostra tableta viagra 25 mg|effect of viagra 50mg|filling after taken viagra|levitra cialis viagra compare|generic viagra veega caverta|how soon take another viagra|buy canadian viagra online|viagra generico effetti|viagra pro and cons|viagra uit india|viagra substitute uk|sale buy viagra soft tabs|best viagra prices canada|viagra to get high|viagra epilepsy|viagra usarla|viagra senza ricetta torino|cheap viagra 25 mg|bestaat er viagra voor vrouwen|viagra uso e dosi|follow link get viagra fast|agarwal aarthi add viagra|viagra spedizione libera|site pour acheter viagra|generic viagra 100mg us|viagra on line canada|discount price viagra sliver|acheter viagra reunion|nebenwirkungen viagra generika

http://viagragenericfa.com/ - generic viagra,generic viagra online,buy generic viagra,buy viagra online,cheap viagra,online viagra,viagra online,viagra cheap,buy viagra,viagra,viagra,viagra

generic viagra,generic viagra online,buy generic viagra,buy viagra online,cheap viagra,online viagra,viagra online,viagra cheap,buy viagra,viagra,viagra,viagra

viagra polen kaufen|pfizer viagra price in euros|is selling viagra online legal|viagra for men with ms|click now viagra testimonial|beate uhse viagra kaufen|viagra contraindicated|only for you mexico viagra|viagra a 18 anni yaho|how do i get free viagra|viagra tablets us|viagra most common dosage|kamagra generic viagra|problems buying viagra online|can someone young take viagra|buy cheap viagra in bulk uk|compra viagra en lnea seguro|viagra femme|gettin viagra at boots london|buscar viagra generica barata|preco de viagra generico|cheap viagra no prescription|viagra cialis kaufen online nz|wow levitra vs viagra|viagra inde acheter|fast shipping viagra uk|authentic viagra on line|cheap viagra brand name|online drug viagra|viagra in australia pharmacy|can buy viagra online uk|overnight online viagra|viagra generico paypal|viagra online from usa|viagra della pfizer|sirve viagra la que yahoo|only best offers viagra pills|only here cheap viagra order|cialis viagra price difference|wholesale viagra|viagra riot|ajanta pharmaceuticals viagra|link for you viagra for ed|boots cost of viagra|india viagra low price|free viagra order|price of viagra at tescos|viagra erfaringer|buy pfizer 100mg viagra box|viagra billig onlin|taking cialis and viagra love|look there viagra alternatives|viagra 0 25mg|can i buy viagra at a chemist|sales online viagra|real viagra without a rx|professional viagra buy|wow viagra pills for sale|does viagra cause hearing loss|viagra users stories|global pharmacy canada viagra|viagra lnder rezeptfrei|buy viagra uk online|best price viagra 100 mg|i use it best price on viagra|viagra 30 anni|oder viagra|viagra de hollande|generico viagra en farmacia|viagra usa kaufen|europa viagra barata|buying viagra dubai|linea viagra generica|viagra condoms online|viagra uso diario|viagra stores massachusetts|viagra homme wikipedia|buy female viagra online|viagra online paypal canada|cheap viagra on line forum|online oklahoma viagra|follow link similar viagra|buy viagra online poland|order viagra soft overnight|pfizer viagra 50 mg online|order viagra in usa|viagra sale online australia|viagra now uk|wow buy viagra generic|viagra bestellung zoll|prezzo viagra in francia|viagra costco pharmacy|best women liquid viagra|generic viagra soft 20mg|caverject taken with viagra|le viagra prix|viagra 100mg berichte|viagra kjpe|discount viagra online nz|free viagra samples canada|just try viagra without a rx|pfizer viagra from canada|where to buy viagra bangalore|lowest price viagra brand|viagra in women effects|viagra 150 mgm n line sales|maximum viagra dose in one day|you viagra hard|viagra online xlpharmacy|demographics of viagra users|inexpensive viagra online|we choice viagra england|100mg viagra overnight|viagra plus with no rx|click here canada viagra|miss viagra costumes|look there free viagra|effects of viagra on teenagers|viagra idoser|viagra precio venta|farmacia viagra de canad|viagra 100g|should buy viagra online|viagra causes aggression|venta viagra concepcio|buying viagra in dubai|viagra come si compra|buy viagra blue pill|comprare viagra su internet|risk free viagra|generic viagra in saudi arabia|viagra billig generik|wow viagra jelly uk|viagra werbung video|buy viagra with priligy|buy viagra in kuala lumpur|usa viagra 4000 mg|uk buy can viagra|viagra free online avis|can you get high from viagra|where viagra super active|buy viagra in eastern cape|link for you cheepest viagra|viagra act sexual that herbs|only here 100 mg viagra|order pfizer viagra|viagra e altri farmac|viagra costo farmacia|buy viagra ship overnight|link for you buy viagra tablet|indian made generic viagra|la viagra es peligros|viagra en suisse|viagra precio comprar|viagra overnight consultant|viagra for women generic|just try viagra ed|viagra para el corazon|best site order generic viagra|we use it viagra professional|taking 2 20 mg viagra|viagra inf|prix viagra 50mg|fast delivery generic viagra|viagra online kaufen de|cheapviagratablets com|scientific name of viagra|click now buying online viagra|viagra effet bnfique|viagra availability australia|look here dosage viagra|best generic viagra reviews|viagra a domicile|viagra store in philippines|superviagra in italia|how to get viagra in zurich|rutabaga viagra|cheap viagra paypal|usefull link womans viagra|click now low price viagra|prezzo generico di viagra|try it viagra sale uk|buy viagra in bristol|only here viagra in england|viagra online uk reviews|compro viagra economico|pharmacy viagra prices uk|viagra et impuissanc|cost viagra pills india|viagra nascar|viagra p801rescriptions|viagra buy in chennai|cheap viagra or sale|pills viagra|viagra para venta auckland|safety of generic viagra|viagra sample packs|try it best quality viagra|viagra in dubai online|viagra gratis paraplegic|viagra sale women uk|ranbaxy viagra bestellen|viagra plus pharmacy coupons|look here viagra tabs|viagra cialis interaction|viagrasupplier co uk contact|puedo tomar viagra y alcoho|purchase viagra tablet|we use it price of viagra|female viagra tablets india|link for you super viagra|viagra vrai pas cher|libido power vs viagra|buy viagra tacoma|walgreen cheap viagra price|buying viagra in macau|cheap viagra cialis india|viagra generico sirve|good choice viagra free pills|recommended site german viagra|acheter viagra prix|mostra tableta viagra 25 mg|effect of viagra 50mg|filling after taken viagra|levitra cialis viagra compare|generic viagra veega caverta|how soon take another viagra|buy canadian viagra online|viagra generico effetti|viagra pro and cons|viagra uit india|viagra substitute uk|sale buy viagra soft tabs|best viagra prices canada|viagra to get high|viagra epilepsy|viagra usarla|viagra senza ricetta torino|cheap viagra 25 mg|bestaat er viagra voor vrouwen|viagra uso e dosi|follow link get viagra fast|agarwal aarthi add viagra|viagra spedizione libera|site pour acheter viagra|generic viagra 100mg us|viagra on line canada|discount price viagra sliver|acheter viagra reunion|nebenwirkungen viagra generika

trend windows

windows live sign in

update

windows 10 store

microsoft essentials

buy cialis online for cheap

cialis coupon

male enhancement pills cialis

cialis coupon 2018

buy cialis england

generic cialis pills

cheap cialis brand

cialis price

cialis pills sale canada

can take 2 viagra 50mg

viagra no pres

sildenafil 50 mg precio

viagra without prescription

200 mg viagra too much

viagra tablets

viagra online fast shipping no prescription

viagra coupons

price levitra vs viagra

can i buy viagra over the counter in france

viagra no prescription

generiek viagra bestellen

viagra no pres

easiest way to get viagra prescription

viagra coupons

viagra cheapest buy

online viagra

vegetal viagra

getting viagra spain

viagra no prescription

buy viagra pharmacy malaysia

viagra without doctor

viagra 30 pills 100mg each

viagra cheap

quanto custo o generico do viagra

viagra online

can you buy viagra over counter dubai

viagra oregon|kpa viagra p ntet|viagra jingle|viagra on line generic|dr x discount viagra|viagra naturale in erboristeri|effects of viagra on men|what if woman take viagra|viagra y cocain|jual viagra online|genericviagrarx|i want to order viagra|is 100mg viagra too much|try it buy viagra cheapest|viagra kamagra 100|viagra 50mg hinta|pldoras viagra baratas uk|nota de viagra 50mg|low cost viagra paypal|can u buy viagra online|looking to purchase viagra|viagra und alkohol|viagra shopping italia|where to buy viagra dublin|cheap viagra on line in uk|wirkung viagra animation|espn radio viagra promotion|el viagra sirve para durar ma|ordre par viagra|viagra 100mg price per pill|buy viagra where india from|viagra por orden telefnica|took two 100mg viagra|viagra purchase in melbourne|cialis vs viagra prices|comprar viagra barat|viagra maximum dose daily|only today viagra sale buy|comparatif prix viagra cialis|viagra shop in malaysia|comprar viagra online net|viagra online stellen|venta barata viagra|i where get viagra|different viagra commercials|viagra or cialis prices|viagra france pu|viagra kaufen auf rechnung|venta de viagrafor|viagra brescia|viagra ohne rezept review|tranny generic viagra|viagra en franais|levitra viagra side effects|viagra tutti i giorni|mejor precio en viagra genuino|price of viagra in dubai|viagra soft generico|viagra 100mg fta|viagra yeux|kann viagra sicher bestellen|red viagra barato comprar|bull 100 viagra wholesale|how to buy viagra for women|lowest price female viagra|viagra blood pressure|rx buys viagra|viagra through canada|50mg viagra paypal uk|womens viagra for sale uk|viagra effects in urdu|pfizer viagra acquisti|colour viagra tablets|only now viagra for women|wisconsin union lawsuit viagra|cheap online viagra|buy viagra bangkok|shop for viagra cheap|viagra 50 forum|viagra triangle chicag|generic viagra soft tab 50mg|free sample viagra canada|buy legal fda approved viagra|buy viagra ship fedex|for in women viagra|best ever viagra picture|order viagra nepal|viagra e pericoloso|viagra online uk|walk in clinic toronto viagra|viagra forums uk|viagra livraison escompte|viagra clinical trials|viagra for sale cheap ireland|try it cheap cialis viagra|only now viagra sale cheap|my viagra store|otc viagra in uk|viagra australia express|achat pillule viagra|click here buy viagra in us|side effects of viagra for men|viagra 25mg price|i was dared to take a viagra|places to buy viagra in nyc|schweiz viagra verkaufen|discount generic viagra uk|u 45976 buy viagra online|viagra online chennai|viagra generico in italia|buy australia viagra can|viagra for sale in thailand|buy cheap viagra in usa|viagra bestellen blog|viagra o cialis foro|viagra in sterreich|preis viagra generika|only today viagra mexico|get best results viagra|quanto costa viagra|viagra buy online get|viagra shopper|viagra online vergleich|acheter du viagra au qubec|viagra les risques|steroids viagra|osu viagra kosten|viagra barato para venta en uk|enter site viagra 25mg uk|wow best price for viagra|the price of viagra in mexico|coupon code for generic viagra|mexican made viagra|cost levitra viagra|comprar viagra en man|viagra for sale uk cheap|viagra online di sconto|cheapest pfizer brand viagra|viagra sale internet|send viagra|where to but viagra safe|viagra bumper stickers|we use it viagra buy usa|acheter viagra site serieux|ipad viagra online sicher|just try viagra health store|viagra dangereux|red viagra hjerte|how do you buy viagra|price viagra vs|cost of viagra australia|viagra enhanced erections|wow viagra no rx required|order viagra sterreich|viagra precio soles|generic viagra pfizer viagra|viagra is not generic|costo de la pastilla viagra|viagra femminile corriere|only here viagra sale|viagra generico venta|vente viagra tunisie|acquisto viagra con paypal|use of viagra after wat|buy viagra professional quick|viagra prix inde|viagra generico online|enter site 100mg viagra|to buy viagra plus click here|pills for girls viagra|cheap viagra 150mg on line|viagra finasteride|we use it viagra costs|ever use viagra|cialis preiswert viagra|viagra toronto store|where to buy pfizer viagra|generic viagra calgary|viagra sildenafil citrat 100mg|viagra generika 50mg kaufen|generic viagra vs generic|viagra sevill|male viagra cream|viagra for men side effects|only now viagra injectable|review levitra cialis viagra|best price viagra name brand|do do what viagra|viagra online pharmacy|available will version viagra|precio viagra madri|100mg viagra price|viagra gratis a los parado|buy viagra uk online paypal|is 10mg viagra enough|when did viagra hit the market|viagra women price india|online pharmacy meds viagra|viagra or cialis better|if women take viagra|best results viagra use|viagra yahoo|viagra ayuda alopecia|billige viagrapillen|us pharmacy viagra|viagra vendo chile|order by phone cheap viagra|buy viagra karachi pakistan|vente viagra 100mg|viagra in usa cheap|viagra generico doc on line|vendita viagra naturale|viagra en lnea canad|only today viagra in britain|viagra online bestellen paypal|tips buying viagra online|viagra online opinie|viagra in ghana|average viagra proce|prices for viagra prescription|en vente viagra|viagra occasion|viagra reseptilke|erfahrungen cialis viagra|viagra generic order|vente de viagra pfizer|viagra children|farmacias en lnea viagra|10 viagra pills uk|opinioni viagra online|denzel washington viagra|viagra y pastilla cialis|viagra fminin|is viagra a prescription drug|usefull link best viagra buy|viagra 88 keys lyrics|just try viagra cialis online|can you over use viagra|vente de viagra en ligne|acheter viagra cialis lign|viagra fruty pastillas suaves|viagra pack trial|viagra e paroxetin|mist halvalla viagraa|buy viagra pill|uk sample viagra|viagra usa overnight delivery|20 mg cialis vs viagra 100 mgs|viagra et avc|buy 1 viagra pill at a time

http://viagraoqss.com/ - buy viagra,buy viagra online,cheap viagra,online viagra,viagra online,viagra cheap,buy viagra,viagra,viagra

buy viagra,buy viagra online,cheap viagra,online viagra,viagra online,viagra cheap,buy viagra,viagra,viagra

viagra oregon|kpa viagra p ntet|viagra jingle|viagra on line generic|dr x discount viagra|viagra naturale in erboristeri|effects of viagra on men|what if woman take viagra|viagra y cocain|jual viagra online|genericviagrarx|i want to order viagra|is 100mg viagra too much|try it buy viagra cheapest|viagra kamagra 100|viagra 50mg hinta|pldoras viagra baratas uk|nota de viagra 50mg|low cost viagra paypal|can u buy viagra online|looking to purchase viagra|viagra und alkohol|viagra shopping italia|where to buy viagra dublin|cheap viagra on line in uk|wirkung viagra animation|espn radio viagra promotion|el viagra sirve para durar ma|ordre par viagra|viagra 100mg price per pill|buy viagra where india from|viagra por orden telefnica|took two 100mg viagra|viagra purchase in melbourne|cialis vs viagra prices|comprar viagra barat|viagra maximum dose daily|only today viagra sale buy|comparatif prix viagra cialis|viagra shop in malaysia|comprar viagra online net|viagra online stellen|venta barata viagra|i where get viagra|different viagra commercials|viagra or cialis prices|viagra france pu|viagra kaufen auf rechnung|venta de viagrafor|viagra brescia|viagra ohne rezept review|tranny generic viagra|viagra en franais|levitra viagra side effects|viagra tutti i giorni|mejor precio en viagra genuino|price of viagra in dubai|viagra soft generico|viagra 100mg fta|viagra yeux|kann viagra sicher bestellen|red viagra barato comprar|bull 100 viagra wholesale|how to buy viagra for women|lowest price female viagra|viagra blood pressure|rx buys viagra|viagra through canada|50mg viagra paypal uk|womens viagra for sale uk|viagra effects in urdu|pfizer viagra acquisti|colour viagra tablets|only now viagra for women|wisconsin union lawsuit viagra|cheap online viagra|buy viagra bangkok|shop for viagra cheap|viagra 50 forum|viagra triangle chicag|generic viagra soft tab 50mg|free sample viagra canada|buy legal fda approved viagra|buy viagra ship fedex|for in women viagra|best ever viagra picture|order viagra nepal|viagra e pericoloso|viagra online uk|walk in clinic toronto viagra|viagra forums uk|viagra livraison escompte|viagra clinical trials|viagra for sale cheap ireland|try it cheap cialis viagra|only now viagra sale cheap|my viagra store|otc viagra in uk|viagra australia express|achat pillule viagra|click here buy viagra in us|side effects of viagra for men|viagra 25mg price|i was dared to take a viagra|places to buy viagra in nyc|schweiz viagra verkaufen|discount generic viagra uk|u 45976 buy viagra online|viagra online chennai|viagra generico in italia|buy australia viagra can|viagra for sale in thailand|buy cheap viagra in usa|viagra bestellen blog|viagra o cialis foro|viagra in sterreich|preis viagra generika|only today viagra mexico|get best results viagra|quanto costa viagra|viagra buy online get|viagra shopper|viagra online vergleich|acheter du viagra au qubec|viagra les risques|steroids viagra|osu viagra kosten|viagra barato para venta en uk|enter site viagra 25mg uk|wow best price for viagra|the price of viagra in mexico|coupon code for generic viagra|mexican made viagra|cost levitra viagra|comprar viagra en man|viagra for sale uk cheap|viagra online di sconto|cheapest pfizer brand viagra|viagra sale internet|send viagra|where to but viagra safe|viagra bumper stickers|we use it viagra buy usa|acheter viagra site serieux|ipad viagra online sicher|just try viagra health store|viagra dangereux|red viagra hjerte|how do you buy viagra|price viagra vs|cost of viagra australia|viagra enhanced erections|wow viagra no rx required|order viagra sterreich|viagra precio soles|generic viagra pfizer viagra|viagra is not generic|costo de la pastilla viagra|viagra femminile corriere|only here viagra sale|viagra generico venta|vente viagra tunisie|acquisto viagra con paypal|use of viagra after wat|buy viagra professional quick|viagra prix inde|viagra generico online|enter site 100mg viagra|to buy viagra plus click here|pills for girls viagra|cheap viagra 150mg on line|viagra finasteride|we use it viagra costs|ever use viagra|cialis preiswert viagra|viagra toronto store|where to buy pfizer viagra|generic viagra calgary|viagra sildenafil citrat 100mg|viagra generika 50mg kaufen|generic viagra vs generic|viagra sevill|male viagra cream|viagra for men side effects|only now viagra injectable|review levitra cialis viagra|best price viagra name brand|do do what viagra|viagra online pharmacy|available will version viagra|precio viagra madri|100mg viagra price|viagra gratis a los parado|buy viagra uk online paypal|is 10mg viagra enough|when did viagra hit the market|viagra women price india|online pharmacy meds viagra|viagra or cialis better|if women take viagra|best results viagra use|viagra yahoo|viagra ayuda alopecia|billige viagrapillen|us pharmacy viagra|viagra vendo chile|order by phone cheap viagra|buy viagra karachi pakistan|vente viagra 100mg|viagra in usa cheap|viagra generico doc on line|vendita viagra naturale|viagra en lnea canad|only today viagra in britain|viagra online bestellen paypal|tips buying viagra online|viagra online opinie|viagra in ghana|average viagra proce|prices for viagra prescription|en vente viagra|viagra occasion|viagra reseptilke|erfahrungen cialis viagra|viagra generic order|vente de viagra pfizer|viagra children|farmacias en lnea viagra|10 viagra pills uk|opinioni viagra online|denzel washington viagra|viagra y pastilla cialis|viagra fminin|is viagra a prescription drug|usefull link best viagra buy|viagra 88 keys lyrics|just try viagra cialis online|can you over use viagra|vente de viagra en ligne|acheter viagra cialis lign|viagra fruty pastillas suaves|viagra pack trial|viagra e paroxetin|mist halvalla viagraa|buy viagra pill|uk sample viagra|viagra usa overnight delivery|20 mg cialis vs viagra 100 mgs|viagra et avc|buy 1 viagra pill at a time

buy cialis eli lilly

cialis price

buy cialis pills online

buy cialis online

how to buy real cialis online

cialis coupon

cheap cialis tablets

cialis coupon 20 mg

cheapest cialis new zealand

microsoft office 2010

microsoft office 2010

microsoft word

microsoft windows

word office

sildenafil citrate equivalent sildenafil 100mg

buy viagra online

viagra online bestellen in der schweiz

viagra pills

sildenafil de 75 mg

viagra generic

will viagra available generically

viagra generic

legally buy viagra uk