Great graph! This is what people wonder, of course. My high watermark is $85k mostly due to some enormous grants near the end of the growth cycle, like one was thirty grand, wtf? What the hell are they thinking with offerings like that? Freaking hilarious that you came out with a higher FICO. I hate how everyone's talking fees now. Just not the same.

This is really amazing how you do this. I have been looking for opportunities like this in Canada but can't seem to find them. If anyone knows let me know...

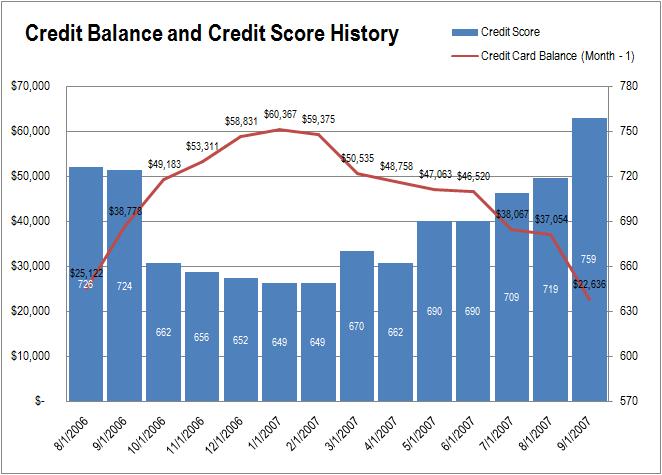

MM: I don't really understand how you suddenly get these huge credit card balances, going from 25k to 60k in a few months, do you go on crazy shopping binges? :)

Creative Investor, by getting a few new cards and doing balance transfer to my credit union's card ... I can transfer excess balance from my credit union's credit card to my checking account free of charge.

MM: Thanks for the response. The numbers are still mind-boggling to me :) But I commend you on making money from this. By the way, I think it's been a while since you talked about your Prosper.com activity, has anything improved on that front? I was disappointed to hear from you and a few other sources about high defaults rates and lack of the secondary markets for loans.

Oh My God, that is a big credit and you are really a hard worker, that is how a person can repay that.

Oh My God, that is a big credit and you are really a hard worker, that is how a person can repay that.

I've just started doing that with credit cards. It's a bit nervewracking at first, but the "free" money you can make is really amazing.

ted - How do you get around the balance transfer fee (typically 3% of balance transfer)? MM does it via his credit union card - how do you?

MM, I have been flowing your blog for more than a year now, Love all the posting,

I have the same question as Matel, I am not clear about how you get around the 3%-5% balance transfer fees, I am also getting many balance transfer offers for 0%, and I have no balances in my CC, so how do you start doing this?

DoubleD

That's a huge drop! Don't make the mistake of thinking of credit being for cosmetic purposes only - auto insurance companies are now looking at your credit to determine rates etc

DoubleD - A lot of the cards have a "max fee" of $50-$75, which is how you get around the 3-5% terms.

If you're really interested in credit arbitrage, you should check out www.mycreditstrategy.com

They have all the answers to those kind of questions in the FAQ section.

How do you get your credit score? Have you signed-up for a yearly service? All places charge to get a credit score? Isn't it?

That is a great graph. I wish I was in that boat with you.

If you have a Credit card with WaMu you get your Credit score fro free from TransUnion, I use to have a CC from Provedian and they got bough by WaMu and WaMu is offering this service.

Hey I really like the graph of yours. Do you use a chart program?

I'm trying to get into the App-O-rama myself...sort of bummed that interest rates have dropped and will probably drop further. It's going to cut into my potential savings interest earned.

-Raymond

Thanks for sharing your data.

I have $200k from 0% cards at this point in time.

My score went from 796 to 643 with $164k debt. Now after 5 months I'm up to 762 with around $145k.

Very sad the Fed are lowering interest rates.

Way to go MM! (:thumbsup:)

For the posters wondering how to avoid the fees, that is typical of new credit lines.

I've done some of the same (only I didn't track it like MM did. I believe I made about $4,200 over the past 2 years doing what MM did with already existing cards (and paying the maximum balance transfer fees).

We recently bought an investment property (at a significant savings ... meaning we paid less than half of what it appraised for). And as a result, my credit score has gone down to the 640 range for the first time in over 5 years! :(

However our net worth has grown by more than $80,000 due to this transaction (and borrowing all the money to purchase and completely rehab the place).

I have been reading your blog for a while now. As far as 0% goes, I think I have done slightly better. How about $175,000 for last seven years with MBNA (now Bank of America) at 0-1.9% APR. Between me and my wife, we have 11 Bank of America cards (some were MBNA that got converted to B of A). I call ech one of them individually (up to their retention department) and get between 0-1.9% for 6 to 12 months (success rate is about 25%). Once they offer a nice B/T APR, I then have them move most of my credit limit to that one card. That means now I have one card with over 100,000 limit with 0-1.99% B/T APR and other ten with $500 credit limit. Last year I made over 10K in high yield accounts. Hope this post helps. There are plenty of other tricks that I can share (however, card companies are also getting smarter :)

CreditGuru,

So how do you get it above a certain amount. They won't raise our CC limit above $34,000 (well, OK I only asked for $1,000 more about 6 months prior to having it raised by $2,500). I guess time may tell.

I'll have to try it again this month. Although they may not do it because they just lent me $40k on an investment property :)

Excellent work with the balance accruals! I wish I had the diligence to replicate your work.

For your readers though, just be careful of the taxes you'll be hit with come April. That's probably the only pain with the higher-interest savings accounts ;)

I saw that you ended up with an even higher credit score than when you started! That is great, the icing on the cake.

Plus, you got over $3000 to do it!!

colchicine gout buy bupropion sr read this

erythromycin purchase cialis viagra online

homepage here Buy Colchicine Indocin Sale

effexor Generic Cymbalta cephalexin 250 mg

lisinopril buy bupropion without script cymbalta prices

cilais cialis pills online cymbalta visa

levitra elocon wellbutrin sr kamagra

doxycycline crestor citalopram 20mg

quetiapine and children prozac and tiredness volume pills for sale acyclovir cold soar

female viagra birth control promethazine for cough cheapest tetracycline what is the cost for synthroid slimex n

buy viagra uk tesco

erectile dysfunction medications

viagra to go generic

ed drugs

sildenafil with 30mg of dapoxetine

get viagra prescription singapore

erection pills

get a prescription online for viagra

ed drugs

compra viagra online in italia

buying cialis in peru

cialis rezeptfrei

is it illegal to order cialis online

cialis without a doctor prescription

cheap-cialis-e.com

can women use viagra tablet

viagra pills

lil wayne get right back up like viagra

viagra pills

do need prescription buy viagra online

viagra pills online australia

buy viagra online

viagra buyer usa

buy viagra

cheapest viagra and cialis

buycialis.it

cheap cialis

buy cialis daily dose

cialis online

how do i buy cialis

can get viagra free

cost of viagra

date viagra goes generic

viagra prices

generic viagra en amazon.com

donde sale viagra

viagra prices

is viagra available in generic form

how much viagra does cost

prices viagra cialis levitra

canadian pharmacy online

canadian pharmacies shipping to usa

List of Safe Online Pharmacies

canadian pharmacies

pharmacy direct

pharmacy direct

canadian pharmacies online

online pharmacies in usa

canadian pharmacies online

online pharmacy without scripts

order cheapest viagra

viagra without prescription

cheapest sildenafil citrate online

viagra no prescription

price compare viagra cialis levitra

buy online viagra in the uk

viagra no script

can i buy viagra over the counter in ireland

viagra without prescription

sildenafil generico precio

payday loan online

online loans

payday loans no credit check

cash advance

current price of viagra in india

viagra without a doctor prescription

viagra sildenafil citrate 50 100 mg

viagra no prescription

viagra price per pill walgreens

25mg viagra dosage

viagra no prescription

viagra online me uk

viagra without prescription

is buying generic viagra illegal

buying viagra in canada online

viagra without a doctor prescription

one viagra pill

viagra without prescription

viagra where to buy canada

viagra ohne rezept aus deutschland

hard sell the evolution of a viagra salesman

viagra no script

can i get viagra at cvs

buy viagra online no rx

viagra without prescription

order brand name viagra online

viagra without a doctor prescription

what do you tell the doctor to get viagra

viagra without a doctor prescription

where can i get free sample of viagra

viagra no script

where to buy viagra in perth

payday loan online

online loans

cash loans

online loans

i took 100mg of viagra

viagra without a doctor prescription

cheapest prices for viagra

viagra without a doctor prescription

have you used generic viagra

viagra no script

can buy viagra uk

viagra without a doctor prescription

generic viagra 50mg online

efectos de sildenafil 50 mg

viagra without a doctor prescription

libro de jamie reidy hard sell the evolution of a viagra salesman

viagra without a doctor prescription

get viagra doctor

viagra no script

can i buy viagra over the counter in uk

viagra no script

the female viagra pill

best online site viagra

viagra without a doctor prescription

comprar viagra en argentina online

viagra without prescription

cheap viagra london

viagra ohne rezept aus deutschland

we can buy viagra india

viagra ohne rezept aus deutschland

viagra dapoxetine sale

payday loans online

payday loans online

payday loans online

payday loans

online order viagra

viagra without prescription

generic viagra free

viagra without a doctor prescription

indian generic for viagra

viagra no prescription

can viagra become generic

viagra ohne rezept aus deutschland

viagra levitra prices

what is the use of sildenafil citrate tablets

viagra prices

where did viagra get its name

viagra cheap

cialis viagra together

buy viagra similar

viagra prices

generic viagra details

viagra prices

viagra tablets uk

cialis liquid for sale

buy cialis

buy cialis legally online

order cialis online

buy female cialis

buy cialis from usa

cheap cialis

how to cut cialis pills

cheap cialis

cheap cialis in uk

cheapest cialis 20mg

buy cialis

buy cialis egypt

buy cialis online

cheap soft cialis

payday loans no credit check

payday loans no credit check

payday loans no credit check

payday loans no credit

payday loans online no credit check

payday loans no credit

payday loans online no credit check

payday loans no credit

payday loans no credit check

payday loans online no credit check

payday loans no credit check

payday loans no credit

buy cialis money order

buy generic cialis

acheter cialis discount

buy generic cialis online

phone number to order cialis

cheap cialis

buy generic cialis uk

cheap cialis

buy cialis brand

buy cialis united states

cialis generic

small order cialis

buy generic cialis

can you buy cialis uk

cheap cialis

cialis discount program

cheap cialis

do cialis pills look like

payday loans no credit

payday loans no credit

payday loans online no credit check

payday loans online no credit check

cialis rush order

cialis generic

cialis film coated tablets tadalafil

buy generic cialis

cialis canada mail order

cheap cialis

discount canadian pharmacy cialis

cheap cialis

cheap daily cialis

can i buy viagra in the uk

buy viagra

uso de viagra 100mg

viagra online

viagra will generic

viagra online

online viagra is it real

generic viagra online

cialis viagra price comparison

buy cheap generic cialis

best price cialis

cialis generique discount

cialis price

brand name cialis for sale

cheap cialis

buy cialis for cheap from us pharmacy

cialis prices

cialis online cheapest

casino games

real money casino

п»їcasino online

online casino

casino online

real money casino

online casino

casino online

free casino games

casino online

online casino

casino online

casino games

casino online

casino games

real money casino

online casino

casino online

online casino

casino online

real vegas online slots

casino online

online roulette gambling usa

casino online

card games real money

casino free games

casino games online

online casinos

slotomania free slots

freeslots

free slots online

slots for free

free slots online

vegetation autocad

autocad

autocad educational version download

autocad student

read autocad files online

auto cad

product key autocad 2011

autocad

autocad 2011 pdf download

sildenafil medana 100 mg tabletki powlekane 4 szt

viagra online

150 mg de sildenafil

online viagra

what does it take to get a viagra prescription

best price viagra

generic viagra is it the same

viagra prices

serve remedio pramil sildenafil 50mg

viagra generico como tomar

viagra without a doctor prescription

movie with viagra salesman

viagra without doctor

viagra pillen voor vrouwen

viagra

buy sildenafil tadalafil vardenafil

viagra coupons

how much is one viagra pill worth

download autocad 2017 software

autodesk inventor

autocad file management software

autodesk 360

product key autocad 2012

autocad

autocad student download mac

auto cad

autodesk autocad 2011 serial number product key

autocad 2000 serial

autodesk maya

descargar visor de autocad 2017 gratis

autodesk revit

autocad mac student 2014

download autodesk autocad

autocad 2011 full 64 bit

autocad download

autocad 3d map download

autocad linetypes download

autodesk maya

cost of autocad 2013 software in india

autodesk inventor

autocad design suite premium 2017 serial

download autodesk autocad

autocad 2011 architecture download

auto cad

autocad shop drawing

rabbit software autocad

autodesk inventor

autocad 12 64 bit download

autodesk 360

serial do autocad 2011

autocad download

download autocad 2000 full version

download autodesk autocad

software gratis autocad

cheap legitimate cialis

online cialis

cialis c20 pills

cialis prices

where to order cialis

cialis generic

cialis online cheap

generic cialis at walmart

canadian cialis sale

generic cialis cheap online

buy cialis online

buy cialis thailand

online cialis

buying cialis in london

tadalafil generic

buy cialis online canadian pharmacy

tadalafil generic

discount generic cialis 20mg

cialis to buy us

buy cialis

cheapest canadian pharmacy for cialis

cheap cialis

buy cialis mississauga

generic cialis tadalafil

best place to order generic cialis

generic cialis at walmart

cheapest cialis generic

canada levitra buy online

levitra online

levitra professional pills

levitra

discount coupons for levitra

vardenafil 20mg

buy levitra bayer

vardenafil 20 mg

cheapest levitra/uk

where i can buy viagra in the philippines

viagra without prescription

100mg viagra cut in half

viagra without a doctor prescription

sildenafil oral jelly 100mg

viagra prices

who can get viagra on prescription

viagra online

viagra and levitra together

buy cialis mississauga

cialis coupons

cialis sale sydney

cialis coupons 2018

cialis pills online

cialis without doctor

how to buy cialis over the counter

cialis without a doctor prescription

cialis sale au

what do generic viagra pills look like

viagra without doctor

how to buy real viagra online

viagra without a doctor prescription

50 vs 100 mg viagra

buy generic viagra

sildenafil viagra 50mg

generic viagra

50 mg viagra how long does it last

50 mg viagra doesnt work

viagra without a doctor prescription

price of viagra in bangladesh

viagra without doctor

4 tab . sildenafil citrate 100mg

generic viagra online

viagra online deutschland bestellen

buy generic viagra

can i order viagra online in canada

viagra cost per pill costco

viagra without prescription

viagra in malaysia where to get

viagra without a doctor prescription

what is the cost of viagra per pill

generic viagra 100mg

viagra how to get

generic viagra online

sildenafil 50 mg comentarios

weight loss prescription drugs

weight loss tablets

weight loss tablets

weight loss medications prescription

order generic cialis india

buy cialis online

ambien cialis eteamz.active.com generic link order

buy cialis online

order cialis in uk

cialis generic

cheap cialis china

generic cialis at walmart

buy cialis canada no prescription

top diet pills

supplements for weight loss

weight loss injections

best appetite suppressant

cialis cheap paypal

cialis generico online

buy generic cialis online no prescription

cialis online

buycialis.eu

tadalafil generic

how to buy cialis

cialis generic

order cialis online safe

buy cialis ebay

buy cialis online

buy cialis online generic

cialis generico online

cialis cheap buy

generic cialis

cialis uk cheap

generic cialis tadalafil

cheapest cialis pharmacy comparison

cheap viagra or cialis

cialis generic

cheapest way to buy cialis

generic cialis

order generic cialis india

cialis online

cheapest canadian pharmacy cialis

cialis cialis prices

viagra cialis pills

buy cialis online generic

generic cialis

how to buy cialis in japan

generic cialis at walmart

buy cialis cheap us pharmacy

cialis cialis prices

cialis viagra levitra sale

buy cialis online

cialis buy uk online

use of cialis pills

cialis generic

cialis sale montreal

generic cialis

buy generic cialis online canada

buy cialis online

cheap viagra or cialis online

buy cialis online

liquid cialis for sale

can cialis pills cut half

generic cialis at walmart

cialis c20 pill

tadalafil generic

cialis pills men

buy cialis online

buy generic cialis paypal

cialis generico online

can i buy cialis in usa

canadian pharmacies

online pharmacy

canadian pharmacy viagra

canadian pharmacies online

canadian pharmacies

online pharmacies canada

Canadian Pharmacy

online pharmacies canada

northwestpharmacy

buy medication without an rx

canada pharmacy

online pharmacies

northwest pharmacy canada

Top Rated Online Canadian Pharmacies

approved canadian online pharmacies

real canadian superstore flyer

online pharmacies canada

canadian pharmacies

can viagra and dapoxetine be taken together

viagra generic

cheap viagra us

viagra generic

getting the most out of viagra

viagra pills

buy herbal viagra

viagra without a doctor prescription walmart

viagra 100mg 8x

sildenafil 50 mg masticable

viagra without a doctor prescription usa

viagra online deutschland

viagra pills

sildenafil 100 mg sandoz

viagra generic

where to get viagra in melbourne

viagra generic

forum generic viagra

cheap cialis with no prescription

cialis generic availability

buy cialis online mastercard

generic for cialis

buy cialis without rx

cialis coupons printable

cialis online cheapest

coupon for cialis

how to buy cialis online

slot machine games for android phones

internet casino links

online casinos that accept australian players

top rated online casino canada

card casino credit deposit

online roulette holland casino

onbling casino for mac

double bet roulette

online gambling in new jersey

casino online

virtual fusion bingo sites

casino online

cash keno online

uk online casinos

roulette free

new online slot casinos

roulette game

live keno online

casino online

play roulette online real money canada

hypercasinos

william hill casino us players

slot games

cleopatra slot machine app for android

best online slots

video poker gambling

order cialis on internet

tadalafil generic

cialis tablets for sale australia

generic cialis at walmart

buy cheap cialis from india

cialis coupon

cialis break pills

buy cialis online

where can i buy cialis soft tabs

get viagra pills

buy sildenafil online

kamagra 100mg oral jelly sildenafil ajanta

sildenafil

buy viagra at boots chemist

buy generic viagra

viagra falso e nocivo venduto online

generic for viagra

erfahrungsberichte viagra 100mg

how to beat online casino blackjack

online roulette

online bingo canada paypal

online roulette

best online casinos us players

hypercasinos

safe us online casino

hypercasinos

best casino gambling online

online slots

online casino paypal ohne download

casino slots

play online casino royale games

autocad 2017 code activation

autocad software

visor de autocad en linea

autocad download

download tai lieu autocad 2011 mien phi

autocad gratis

autocad map download

autocad 2007

autocad design suite standard 2017 download

acad

autocad plus minus code

autodesk student download

download giao trinh autocad

autocad 2016

download software autocad 2011 full version

autodesk student

autocad lt 2011 full version

autocad mechanical

articles on autocad

autocad inventor

download autocad 2011 for mac

autodesk student download

cad software similar to autocad

acad

autocad 2000 serial

autocad architecture for mac student

download autocad

autocad 2012 product serial number

autocad studentenversion

autocad 14 serial number cd key

autocad 2018

descargar autocad 2013

autocad 2007

autocad lt mac price

autocad 2017 download

autodesk autocad electrical 2011 download

autocad 2018

autocad 2017 activation code 32 bit

autocad lt

vegetacion autocad gratis

autocad gratuit

autocad descargar 2017

autocad inventor

discount autocad lt

autocad 2017

serial autocad 2017

autocad gratis

autocad 12 64 bit download

autocad software

autocad civil 2011 download

microsoft sign in

windows 8

upgrade to windows 10

windows 10 upgrade

office365

windows photo gallery

windows 10 download

microsoft excel

windows live

microsoft visio

itunes for windows

windows updates

windows live sign in

windows 10 store

where's my printer in windows 10 mobile

is it legal to buy cialis online in canada

cialis coupon

cheap viagra cialis

cialis coupon

cheap cialis tablets

cialis generic

cheap cialis from india

generic cialis price

buy cialis in uk

microsoft windows 10

windows 10 download

hardware troubleshooter

win 10

stegbar windows

generic viagra en amazon.com

viagra without prescription

when will generic viagra be available in canada

viagra without a doctor prescription

where can i buy viagra in amsterdam

cheap viagra

viagra tablets for men price in india

viagra tablets

pill better viagra cialis levitra

cheap viagra in sydney

viagra without prescription

buying viagra london

viagra no prec

generic viagra kamagra

viagra coupon

viagra dosis 25 mg

viagra online

viagra generico intercambiable

microsoft office login

windows 8

windows movie maker download

upgrade to windows 10

reinstall windows 10

buy sildenafil online uk

viagra without a prescription

how to get a viagra sample

viagra without a prescription

get insurance pay viagra

viagra pills

can viagra go generic

viagra cheap

sample viagra pills

install microsoft word for free

microsoft store

microsoft company store

office 2013

ms store

buy generic cialis in usa

cheap cialis

cheapest real cialis

buy cialis online

how to buy cialis over the counter

cialis coupon

buy cialis uk

cialis coupons

cheap cialis uk online

getting hard without viagra

viagra online

can buy viagra paypal

cheap viagra

generic viagra made

buy generic viagra

get viagra australia

generic viagra

esiste il farmaco generico del viagra

is generic viagra the same as brand

buy viagra online

viagra script online

viagra price

legal buy viagra craigslist

buy generic viagra online

buy viagra online with debit card

buy generic viagra online

can i buy viagra over the counter in turkey

cialis c20 pills

cheap generic cialis

buy cialis no rx

buy generic cialis

can you cut cialis pills in half

cialis prices

cheap cialis viagra

cheap cialis

acheter cialis discount

microsoft store locations

microsoft office 2016

www.microsoft.com login

microsoft office 365

buy microsoft word

ok split cialis pills

buy generic cialis

how to buy cialis in uk

buy generic cialis online

buy cialis online without rx

best price for cialis

buy cialis vietnam

cialis price

cialis discount code

microsoft office 2016

microsoft office 2010

microsoft office 365 sign in

microsoft online

descargar word

onde comprar generico viagra portugal

viagra without doctor

sildenafil generic mexico

viagra

pill cutter viagra

viagra online

buy viagra in sri lanka

viagra prices

shop viagra online

best pharmacy to buy cialis

generic cialis tadalafil

cialis china cheap

generic cialis

buy cialis online canada

fncialisokgh.com

cialis pills for women

fncialisokgh.com

order cialis to canada

cheap generic cialis uk

generic cialis tadalafil

cheap authentic cialis

generic cialis tadalafil

buy viagra cialis online

cialis online

cialis brand cheap

buy cialis online

cheap cialis professional

generic celebrex

flagyl

flagyl antibiotic

finasteride 5mg

voltaren tablets

voltaren tablets

finasteride

where to buy levitra cheap

levitra 10 mg

buy levitra perth

order levitra online

buy levitra in london

viagra and saw palmetto

generic viagra

when will there be a generic version of viagra

viagra online

viagra extenze together

buying viagra in uk

viagra without doctor

happens if take viagra cialis together

viagra without a doctor's prescription

viagra quantos mg

viagra pills

cheap viagra in usa

viagra online

getting viagra in italy

buying levitra online safe

where can i get levitra

how to buy levitra online

viagra cialis levitra

order cheap online levitra

celebrex

flagyl

buy flagyl online

finasteride

voltaren 100 mg

voltaren

propecia

cialis pills in canada

cialis

buy cialis viagra

online cialis

cheapest generic cialis canada

generic cialis

buying cheapest generic cialis soft tab

buy generic cialis online

buy cheap cialis uk

order female cialis

buy cialis online

order generic cialis india

cialis online

where to buy cialis online no prescription

generic cialis 2018

buying cheapest generic cialis soft tab

generic cialis 2018

cialis pills women

how to buy levitra in canada

levitra online

buy levitra pills

levitra vs viagra

buy levitra online in canada

viagra tablets price in chennai

viagra generic

can i get a free sample of viagra

generic viagra 2018

can you buy viagra in england

viagra online pharmacy

viagra trimix together

viagra online pharmacy

overseas viagra sale

compare price viagra cialis levitra

viagra online

cvs price for viagra

buy viagra

viagra sales 2012

buy generic viagra

viagra online kaufen auf rechnung

cheap generic viagra

cialis 20mg vs viagra 50 mg

play casino games online

slot online

slot game

casino games

v http://viagrraver.com is there generic viagra

safe place to buy viagra uk

generic viagra 100mg hieu thuoc co ban viagra

canada pharmacies online prescriptions

prednisone

prescription drugs online without doctor

prednisone

Online Canadian Pharmacies

furosemid

canadian pharmacy online

furosemide 40 mg

canadian pharmacy online

can i cut cialis pills

generic cialis

can cialis pills be cut

cialis generic

cheap cialis online pharmacy

cialis

cialis tablete srbija

cialis online pharmacy

cialis discount coupon

can you legally buy viagra online

online prescription

viagra tablet price in delhi

online prescription

buy cheap viagra

prescriptions online

how to buy viagra from india

prescriptions online

get viagra under 18

online casino slots

casino slots

casino games

online casino slots

online casino real money

casino games

slot online

online casino slots

do need prescription buy viagra uk

buy viagra online

where to buy viagra online in uk

viagra online

can i buy viagra over the counter in mexico

buy generic viagra online

can u buy viagra india

generic viagra online pharmacy

cheapest price viagra online

low price viagra canada

viagra online

how to buy viagra in india

viagra

buy cheap viagra australia

buy generic viagra

viagra prescription online consultation

buy generic viagra

bula generico viagra ems

cialis 10 mg viagra

viagra without prescription

viagra tablets sale

viagra without a doctor prescription

can viagra cialis taken together

cheap viagra

viagra 5 mg

viagra without doctor

order viagra in europe

do you have to be 18 to buy viagra

viagra

can i buy generic viagra in the us

viagra online

levitra cheaper than viagra

buy generic viagra

sildenafil citrate generic viagra

viagra generic

generico do viagra nao funciona

sc4

adobe cs6

adobe pdf reader acropdf.dll

creative suite

adobe flash player for windows 10

photoshop cs6

pdf

photoshop cs6

cs 1.6 download

discount code for cialis

buy cialis

viagra and cialis for sale

buy cialis online

buy cialis manila

generic cialis 2018

url=http //opeyixa.com/qoxoo/2.html cheap cialis /url

generic cialis tadalafil

buy cialis overnight

cialis sale toronto

buy cialis online

order cialis in canada

buy cialis

cialis for sale in london

generic cialis tadalafil

how to buy cialis in canada

generic cialis 2018

buy cialis united states

cheap levitra in canada

levitra generic

order levitra super active oo

levitra generico

levitra cheap canada

buy viagra over counter uk

viagra without a prescription

viagra online shop spam

viagra without doctor

where can buy viagra in the uk

buy generic viagra online

sildenafil cheap online

generic viagra 100mg

is it legal to buy viagra online from canada

wo kann ich viagra online bestellen

buy generic viagra

viagra for cheap from canada

generic viagra online

acheter viagra online

viagra without doctor

order generic viagra cialis

viagra without doctor

get rid viagra virus

can you buy cialis over the counter in canada

cialis online

cheaper viagra cialis levitra

buy cialis online

buy cheapest cialis

buy generic cialis online

buy cialis online mastercard

generic cialis online

cialis tablets for sale australia

order cialis online pharmacy

cialis generico

cialis online buy

generic cialis at walmart

can you split cialis pills half

cialis coupons

cheap cialis soft tabs

tadalafil 20 mg

cheap cialis in the uk

generic viagra sublingual

ed pills that work

acquisto viagra online italia

ed pills

taking yohimbe viagra together

ed pills

viagra in australia for sale

erectile dysfunction pills

is it illegal to buy viagra online in usa

uk cialis sales

ed pills that work

viagra 50 mg einnahme

erectile dysfunction remedies

buy cheapest cialis

ed pills

se puede comprar viagra sin receta medica

erectile dysfunction pills

efek samping cialis 50mg

buy cialis without prescriptions

buy cialis online

order cialis no prescription online

cialis

order cialis

cialis usa

how to use cialis pills

cialis tablets

buy cialis vegas

buy cialis safely

generic cialis online without script

cheap cialis once day

generic cialis online pharmacy

where to buy cialis in canada

buy cialis

cheap-cialis.net

cialis

cialis order uk

safe place order cialis

generic cialis

how to cut cialis pills

generic cialis online pharmacy

buy generic cialis europe

cialis online

buy cialis edmonton

buy cialis

buy cialis prescription online

buy viagra madrid

viagra tablet

viagra sale spain

viagra pill

cheap viagra now mastercard

viagra sales

teva sildenafil price

viagra sale

generic viagra from cipla

best pharmacy to buy viagra

generic viagra online without script

can buy viagra ebay

viagra generic

buy viagra walgreens

viagra for sale uk

viagra falso e nocivo venduto online

viagra for sale uk

viagra canada no prescription online

sildenafil citrate generic viagra 100mg

viagra tablets

easy way to get viagra

viagra pills 100 mg

buying viagra online dangerous

viagra online sales

do you need a prescription to buy viagra in the uk

viagra sales

sildenafil professional 100mg

Add Your Comments

|