Well, the excess return is only equal to alpha if you had a beta of 1 to the benchmark?

>1) Good stock picking....

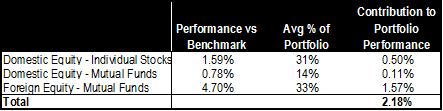

I thought the stock picking was not so good,

.80% (the extra over funds) of say U$ 300k is about 3k. Assumming extra time and effort was spent on stock v/s funds, say about 4 hrs per month, that is 3k/48 ~ U$60 per hour return which is on the lower side and with higher risk.

Did I miss something?

MM, just curious why you just use EFA in your international coverage of your benchmark? EFA is for developed stock markets. You are missing the emerging markets. would EFA + EEM be a little better?

moom - yes, you are technically right. i should calculate the beta too but obviously it will be challenging. now that my average cash holding is way above the benchmark, i would assume my beta will be less than 1.

Amit C - it doesn't take 4 hours per month to pick funds. it probably only took me 4 hours altogether in 2007 to pick all funds.

Wei - yes, i was conservative on the emerging markets.

It's pretty easy to compute alpha and beta using Excel as long as you have data on your percent returns in each month.

I would agree with Wei. VEU might be a better foreign benchmarking instrument since it captures emerging markets as well. I am assuming your fund picks most likley had emerging market exposure which would explain their 4.7% excess return above EFA.

What will happen with Berkshire after Buffett is gone?

moon, yes, but then some people will hold me to the higher standard of calculation alpha and beta based on daily results.

Congratulations. However, before you celebrate too much, beating your benchmarks in any given year is not an indicator of systematic success. In other words this could be... good luck playing on your side.

Also, you can also beat your benchmark by accepting a higher degree of risk. While your average return may be higher, the volatility of your portfolio (i.e. your risk) will also be higher. So, while you have beaten your benchmark, it may be that you selected an incorrect benchmark - one that has a lower return and lower risk profile.

It has been repeatedly demonstrated that beating market benchmarks OVER THE LONGHAUL is a very VERY hard thing to do. You may be one of those few unique individuals who are able to do so consistently, but the other explanations are more probable.

Don't forget to take into account the sense of satisfaction and accomplishment that comes from beating the benchmark instead of just investing in the index fund. (Of course such logic would also explain why most people don't invest into index funds, but hey, to each his own!) In any case, nice job dissecting your performance!

2 things:

1) VTI (Vanguard Total Stock Market Index) returned > 5.5% last year, so your actual vs. benchmark in this category seems high; it should be closer to a 1.46% excess return on the individual stocks and .65% on the mutual funds.

2) EEM (MSCI Foreign Emerging Markets) returned about 38% last year; EFA (MSCI Foreign Developed Markets) returned 12%. Averaging these two returns would give a 25% return, which beats your actual performance by 10%.

To conclude, I think your domestic equity performance vs the benchmark is subpar, when calculating the extra volatility of owning individual stocks. I think your performance was inferior to the foreign benchmarks, when they are (properly) calculated to reflect emerging markets.

I think your portfolio would look a lot better if it was simply 50% VTI, 25% EFA, and 25% EEM. You could hold all these funds at Zecco at an absolutely minimal cost.

I’d like to have a dog. On the other hand, my wife likes cats better.

o viagra forum happiness

lost|[url=http://erectionpillsvcl.com/viagra-doesnt-work]walgreens viagra[/url]

walgreens viagra price

j levitra online bound [url=http://levitrayc.com]buy levitra[/url] levitra coupon

u buy cialis online just [url=http://cialisyc.com]cialis online[/url] tadalafil

z sildenafil believe [url=http://viagrayc.com]buy viagra online[/url] generic viagra online

r buy generic viagra regard [url=http://viagrayc.com]generic viagra online[/url] buy generic viagra

z no credit check payday loans hundred [url=http://paydayloansyc.com]payday loans no credit check[/url] payday loans online no credit check

g buy prednisone online whole [url=http://prednisoneyc.com]prednisone 20mg[/url] prednisone

forum acquisto viagra online

viagra without prescription

viagra getting

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

will 12.5 mg viagra work

safe place to order generic viagra

viagra without prescription

looking buy viagra online

[url=http://bfviagrajlu.com/#]viagra without doctor[/url]

can get free viagra nhs

sildenafil orion 50 mg

viagra without a doctor prescription

generic viagra approved fda

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

how to get free viagra sample

how long does half a pill of viagra last

viagra without prescription

how often can you take 100mg of viagra

[url=http://bfviagrajlu.com/#]viagra without doctor[/url]

when will viagra have a generic

do viagra pills make you last longer

viagra without prescription

nombre comercial sildenafil 50 mg

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

magnus viagra 100mg

hoe lang werkt een viagra pill

viagra without doctor

viagra reputable online pharmacy

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

going price for viagra

happens if take viagra cialis together

viagra without doctor

viagra in dubai price

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

wie teuer sind viagra pillen

viagra online goedkoop

viagra without prescription

viagra pfizer 100mg price

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

getting most out of viagra

lsd to treat addiction

drug addiction rehab centers

relief from opiate withdrawal

[url=http://drugrehabtrustedclinic.com/]drug addiction rehab centers[/url]

detox from oxycontin

rehabilitation center

rehab addict

information on drug abuse

[url=http://drugrehabtrustedclinic.com/]alcohol rehab centers[/url]

heroin detox centers

suboxone detox

drug addiction rehab centers

withdrawal symptoms from opioids

[url=http://drugrehabtrustedclinic.com/]drug addiction rehab centers[/url]

overcome opiate withdrawal

[url=http://buyviagrasoft.reisen/]viagra soft[/url] [url=http://atenolol.fail/]atenolol[/url] [url=http://buy-advair.reisen/]advair cost[/url] [url=http://clomidprice.pro/]clomid[/url]

[url=http://viagra247.us.com/]Generic Viagra Online[/url] [url=http://colchicine247.us.com/]Colchicine Online[/url]

[url=http://lisinopril20mg.us.org/]lisinopril[/url] [url=http://fluoxetine247.us.com/]buy fluoxetine[/url]

[url=http://buy-phenergan.shop/]buy phenergan[/url] [url=http://cephalexin.reisen/]cephalexin 250mg[/url]

free shipping generic viagra

viagra 100mg pills

quantas mg tem o viagra

[url=http://gdoviagrakjyu.com/#]buy viagra 100mg[/url]

viagra red pills

cialis super active 20mg pills

cialis from canada

buy cialis cheap prices fast delivery

[url=http://fgocialisgfeb.com/#]cialis online pharmacy[/url]

cheap cialis paypal

reliable place buy cialis

cialis online pharmacy

best place to order generic cialis

[url=http://fgocialisgfeb.com/#]cialis online pharmacy[/url]

very nice site cheap cialis

discount pharmacy

Canadian Online Pharmacies

no prior prescription required pharmacy

[url=http://ehmcanadaufgpharmacypo.com/#]Canadian Online Pharmacies[/url]

cvs pharmacy online

prescription drugs without prior prescription

Canadian Online Pharmacy

canada pharmacy online

[url=http://ehmcanadaufgpharmacypo.com/#]Canadian Online Pharmacies[/url]

Trusted Online Pharmacies

comprar viagra generico sin receta

viagra without prescription

when is viagra going generic

[url=http://dyviagrahwithoutbdoctorklprescription.com/#]viagra no script[/url]

viagra 365 pills

can you take 150mg of viagra

viagra without prescription

can you buy viagra in hong kong

[url=http://dyviagrahwithoutbdoctorklprescription.com/#]viagra without a doctor prescription[/url]

best online viagra pharmacy

discount cialis and viagra

cialis online

cheap viagra or cialis online

[url=http://vgcialistylbuyjl.com/#]cialis buy[/url]

generic cialis buy

[url=http://colchicine247.us.com/?cialis/no/pres]cialis no pres[/url] [url=http://colchicine247.us.com/?cheap;abilify;2mg]cheap abilify 2mg[/url] [url=http://colchicine247.us.com/?Bactrim=Suspension=Refrigerate]bactrim suspension refrigerate[/url] [url=http://colchicine247.us.com/?Tacrolimus,Ophthalmic,0.03]tacrolimus ophthalmic 0.03[/url] [url=http://colchicine247.us.com/?finasteride/brand/name]finasteride brand name[/url] [url=http://colchicine247.us.com/?Tylenol;Diclofenac;Interactions]tylenol diclofenac interactions[/url]

cialis discount generic

cialis online pharmacy

many pills cialis

[url=http://vgcialistylbuyjl.com/#]buy cialis[/url]

buy cialis online no prescription

where is the best place to buy cialis

buy cialis

buy cialis online canadian no prescription

[url=http://vgcialistylbuyjl.com/#]cialis online pharmacy[/url]

daily cialis pills

cialis professional uk

generic cialis

cialis 2.5mg

buy cialis ’

is viagra fda approved as a generic

buy viagra johor

viagra australia price

[url=http://vgcialistylbuyjl.com/#]viagra generic for sale[/url]

buy generic viagra canada online

buying viagra overseas

viagra men cheap

cheaper alternative viagra

[url=http://vgcialistylbuyjl.com/#]cheapest viagra buy cheap viagra[/url]

viagra generico en colombia

best site to order generic viagra

safe buy viagra online yahoo

buying online viagra safe

[url=http://vgcialistylbuyjl.com/#]viagra for cheap with no prescriptions[/url]

original viagra price in india

buy chinese herbal viagra

buy viagra online cheap

hace falta receta medica para comprar viagra

[url=http://vgcialistylbuyjl.com/#]buy viagra generic canada[/url]

what pill is like viagra

online viagra fast shipping

cheap viagra online india

buy cheap viagra blog

[url=http://vgcialistylbuyjl.com/#]viagra cheap thailand[/url]

can you buy viagra over the counter in ireland

can i buy viagra over the counter in spain

generic viagra for cheap

dog eats viagra pills

[url=http://vgcialistylbuyjl.com/#]viagra buy australia[/url]

viagra 100 mg buy

viagra sale chemists

buy viagra pfizer

mail order viagra uk

[url=http://vgcialistylbuyjl.com/#]generic viagra cheap uk[/url]

free viagra with order

buy viagra online now

order viagra without rx

will there generic drug viagra

[url=http://vgcialistylbuyjl.com/#]cheap herbal viagra uk[/url]

can you get viagra without going doctor

viagra online best place

viagra sale online uk

where i can buy viagra in chicago

[url=http://vgcialistylbuyjl.com/#]how to order viagra online from india[/url]

what is the generic name for viagra

viagra to buy

viagra for sale in the usa

comprar viagra farmacia online

[url=http://vgcialistylbuyjl.com/#]buy cheap viagra blog[/url]

where to buy viagra in canada safely

prices of viagra cialis and levitra

herbal viagra sale ireland

does generic viagra work the same

[url=http://vgcialistylbuyjl.com/#]generic viagra sale uk[/url]

buying viagra in uae

viagra for sale in auckland

viagra buy dublin

viagra wholesalers uk

[url=http://vgcialistylbuyjl.com/#]how to buy viagra in india[/url]

generic viagra sold us

is 100mg viagra is too much

discount viagra sale

prescription free generic viagra

[url=http://mbviagraghtorderke.com/#]do not order mexican viagra[/url]

kamagra sildenafil 32 pills

tab sildenafil 50mg

cheap quality viagra

can you take half pill viagra

[url=http://mbviagraghtorderke.com/#]buy viagra hyderabad india[/url]

sildenafil 50 mg se usa

can you buy viagra over counter uk boots

viagra price

using viagra levitra together

[url=http://mbviagraghtorderke.com/#]buy viagra online new york[/url]

sildenafil jelly 100mg

cheap sildenafil citrate 100mg

viagra sale in australia

will 25 mg of viagra work

[url=http://mbviagraghtorderke.com/#]viagra usa buy[/url]

buy malegra dxt (sildenafil + fluoxetine)

pfizer viagra cheap

order viagra online india

should take 50mg viagra

[url=http://mbviagraghtorderke.com/#]buy viagra tokyo[/url]

where we can buy viagra in india

viagra canadian online pharmacy

Viagra 100 mg

what is the best viagra to buy

[url=http://mbviagraghtorderke.com/#]Viagra 100mg[/url]

buy single viagra

cialis 20mg e viagra

Viagra Online

price levitra cialis viagra

[url=http://mbviagraghtorderke.com/#]Viagra 100mg[/url]

price viagra uk

what does the viagra pill look like

Viagra Pills

how many mg are in viagra

[url=http://mbviagraghtorderke.com/#]Generic Viagra[/url]

safe place to buy viagra online

tomar viagra de 25mg

Viagra 100mg

viagra generic available

[url=http://mbviagraghtorderke.com/#]Generic Viagra[/url]

what mg viagra to take

safe cialis

cialis

cheapest generic cialis

cialis ’

order free viagra sample

Viagra 50mg

viagra online real or fake

[url=http://mbviagraghtorderke.com/#]Viagra 50 mg[/url]

posso comprar viagra sem receita medica

can you order viagra from canada

viagra australia

reliable generic viagra online

[url=http://fastshipptoday.com/#]viagra on line[/url]

big love viagra blue watch online

buying viagra online legal us

viagra cost

pfizer viagra order online

[url=http://fastshipptoday.com/#]viagra australia[/url]

viagra comanda online

generico ou similar do viagra

viagra pill

use of sildenafil citrate tablet

[url=http://fastshipptoday.com/#]viagra pills[/url]

generic drug viagra

el mejor viagra generico

viagra for sale uk only

viagra 100mg kaufen preis

[url=http://fastshipptoday.com/#]where to buy viagra[/url]

vegetal viagra suppliers

cheap viagra us pharmacy

viagra for men

pillola rossa viagra

[url=http://fastshipptoday.com/#]viagra coupons[/url]

canadian generic sildenafil

coupon viagra online

viagra for sale uk

sildenafil citrate 100mg australia

[url=http://fastshipptoday.com/#]buy viagra[/url]

generic viagra uk paypal

how to buy cialis

cialis coupon

cheapest cialis in new zealand

[url=http://waystogetts.com/#]cheap cialis[/url]

buy cialis brand online

buy cheap cialis link online

cialis online

cialis generic cheapest

[url=http://fkdcialiskhp.com/#]cialis online[/url]

buying cialis online canada

buy cheap cialis profile

tadalafil generic

cheap cialis australia

[url=http://fkdcialiskhp.com/#]cialis online[/url]

buy cialis from europe

buy cialis professional online

buy cialis online

buy real cialis online

[url=http://gmwcialiskem.com/#]cialis cost[/url]

order cialis india

cialis china cheap

cialis online

cheap cialis tablets

[url=http://bhscialisdjy.com/#]cialis online[/url]

buy cheap cialis online no prescription

generic cialis buy online

cheap cialis

cheap cialis once day

[url=http://bhscialisdjy.com/#]cialis cost[/url]

buy cialis no prescription uk

viagra alternative

cheap viagra

price viagra

buy viagra ’

buy cialis new delhi

cheap cialis

pink cialis pills

[url=http://bhscialisdjy.com/#]cialis online[/url]

best discount cialis

buy generic cialis online in usa

buy cialis online

ok split cialis pills

[url=http://bhscialisdjy.com/#]cheap cialis[/url]

where is the best place to buy generic cialis

order cialis online from canada

cheap cialis

cialis for sale in nz

[url=http://bhscialisdjy.com/#]cialis cost[/url]

cheapest generic cialis online

celebrex online

[url=http://hqcelebrex2017.com/]celebrex prices[/url]

celebrex online

propecia

[url=http://hqfinasteride2017.com/]buy propecia online[/url]

finasteride 1mg

finasteride 5mg

buy cialis soft tabs

buy cialis

discount genuine cialis

[url=http://gmwcialisfnw.com/#]buy cialis[/url]

buy cialis uk cheap

cialis sale no prescription

cialis online

discount generic cialis canada

[url=http://gmwcialisfnw.com/#]buy cialis[/url]

cialis discount

buy pfizer viagra 100mg

buy viagra online

where buy viagra in dubai

[url=http://rmaviagraplq.com/#]cheap viagra[/url]

sildenafil citrate chewable tablets 100mg

best site buy viagra

buy viagra online

viagra pills for sale canada

[url=http://rmaviagraplq.com/#]viagra online[/url]

free viagra pills

do diabetics get free viagra

buy viagra

best generic viagra forum

[url=http://rmaviagraplq.com/#]buy viagra[/url]

viagra online xl

best viagra prices

cheap viagra

buy viagra online fast delivery

[url=http://rmaviagraplq.com/#]cheap viagra[/url]

viagra where to get

buy cialis with online prescription

cialis generic

female cialis pills

[url=http://tbnacialiskj.com/#]generic cialis[/url]

buy generic cialis online

cheap viagra levitra cialis

generic cialis at walmart

order cialis professional online

[url=http://tbnacialiskj.com/#]tadalafil generic[/url]

where can i order cialis

cheap genuine cialis

cialis generic

order generic cialis india

[url=http://tbnacialiskj.com/#]generic cialis 2017[/url]

order cialis online from canada

best online site buy generic viagra

viagra generic availability

buy viagra levitra online

[url=http://ehuviagramek.com/#]generic viagra[/url]

best place order viagra

autocad online job

autocad

autocad lt student price

[url=http://autocadgou.com/#]autocad download[/url]

autocad 3d furniture download

autodesk autocad 2011 student version

autocad software download

download autocad materials

[url=http://autocadgou.com/#]autocad software[/url]

autodesk autocad 2000 download

autocad 2017 and autocad lt 2017 bible download

autocad 2015

autocad produced by an autodesk educational product

[url=http://autocadgou.com/#]autocad 2016[/url]

autocad 2013 student version

autocad original software price

autocad autodesk

autocad map 3d 2011 download

[url=http://autocadgou.com/#]autocad 2014 free download[/url]

design center online autocad

activation code for autocad 2017 64 bit

autocad 2014

autocad 1012 download

[url=http://autocadgou.com/#]autocad 2015[/url]

descargar bloques autocad 3d

autocad takeoff software

autocad download

descargar bloques gratis de autocad

[url=http://autocadgou.com/#]autodesk autocad[/url]

autocad 2011 version number

autocad draftsman online jobs

autocad 2016

venta de software autocad en chile

[url=http://autocadbmsa.com/#]autocad lt[/url]

software autocad civil 3d

autocad lt 2002 upgrade

autocad download

autocad electrical 2013 price

[url=http://autocadbmsa.com/#]autocad 2014[/url]

software autodesk autocad

download autocad 2017 student

autocad

autocad 3d home design software

[url=http://autocadbmsa.com/#]autocad download[/url]

autocad product key 2011 serial number

autocad 2017 key gen

autodesk autocad

autocad civil 3d 2011 download

[url=http://autocadbmsa.com/#]autodesk autocad[/url]

autocad 2017 product key 64 bit

autodesk autocad lt 2017 price

autocad 2018

autocad civil 3d 2011 download

[url=http://autocadbmsa.com/#]autocad lt[/url]

autocad 2011 serial no and product key

activation key for autocad 2017 64 bit

auto cad

autocad architecture 2012 product key

[url=http://autocadbmsa.com/#]autocad 2017[/url]

2012 autocad serial number

buy autocad 2017 full version

autocad 2014

autocad 2002 serial number and product key

[url=http://autocadbmsa.com/#]autocad download[/url]

autocad 2017 serial number activation code

autocad 3d sample drawing download

autocad 2018

autocad oem 2017

[url=http://autocadbmsa.com/#]autocad lt[/url]

autocad student tamu

can get viagra free nhs

viagra without a doctor prescription

good place buy generic viagra

[url=http://itfviagrakmn.com/#]viagra on line no prec[/url]

viagra buy in australia

viagra virkning 100 mg

best price for viagra

buy viagra online los angeles

[url=http://itfviagrakmn.com/#]viagra for men[/url]

can i take two 50mg viagra at one time

cheap viagra online pro

viagra on line no prec

walmart pharmacy viagra price

[url=http://itfviagrakmn.com/#]viagra coupons 75 off[/url]

generic viagra 100mg price

viagra sale online ireland

best price for viagra

can you bring viagra across border

[url=http://itfviagrakmn.com/#]viagra without a doctor prescription[/url]

cheap viagra overnight

sildenafil aurochem 50mg

viagra tablets

best deal viagra online

[url=http://itfviagrakmn.com/#]viagra coupons 75 off[/url]

online viagra legit

pills like cialis

cialis pills

cialis blue pills

[url=http://fmacialisuhy.com/#]cialis coupons[/url]

how to order cialis

cheap cialis 10 mg

cialis prices

cialis by mail order

[url=http://fmacialisuhy.com/#]cialis tablets[/url]

cheap cialis generic online

buy cialis johannesburg

cialis without a doctor's prescription

buy cialis professional uk

[url=http://fmacialisuhy.com/#]cialis pills[/url]

buy cialis in canada

buy viagra and cialis online

cialis cost

cheap cialis no prescription

[url=http://fmacialisuhy.com/#]cialis prices[/url]

can you buy cialis mexico

where to buy generic cialis

cialis cost

buy cialis professional cheap

[url=http://fmacialisuhy.com/#]cialis prices[/url]

buy cialis prescription online

much does viagra cost target

viagra online

order viagra now

[url=http://fvbviagrahnas.com/#]online pharmacy viagra[/url]

how much does viagra cost per pill at walgreens

viagra england buy

buy viagra online

how to cut a viagra pill

[url=http://fvbviagrahnas.com/#]viagra buy[/url]

generico viagra

can you buy viagra over the counter in mexico

online pharmacy viagra

donde puedo comprar viagra en mar del plata

[url=http://fvbviagrahnas.com/#]cheap viagra[/url]

safe take cialis viagra together

cheapest cialis tablets

cialis without a prescription

cialis thailand buy

[url=http://vnacialisfbvn.com/#]cialis without a prescription[/url]

cialis soft tabs cheap

generic cialis pills e20

cialis without prescription

is it legal to buy cialis online in canada

[url=http://vnacialisfbvn.com/#]cialis without a doctor[/url]

buy cialis england

is it legal to buy cialis online in canada

cialis without a doctor

cialis pills for sale

[url=http://vnacialisfbvn.com/#]cialis without doctor[/url]

cialis cheapest lowest price

cialis cheap prescription

cialis without doctor

cheap cialis canadian

[url=http://vnacialisfbvn.com/#]cialis without prescription[/url]

do cialis pills expire

how to order cialis online safely

cialis without doctor

cheap cialis online india

[url=http://vnacialisfbvn.com/#]cialis without doctor[/url]

cheap cialis pills

cialis super active+ 20mg pills

cialis without a doctor

generic.cialis.pills

[url=http://vnacialisfbvn.com/#]cialis without a prescription[/url]

buy cheap cialis profile

do you get addicted viagra

viagra without an rx

where can i buy herbal viagra

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor's prescription[/url]

acquisto online viagra generico

best viagra tablet india

viagra without an rx

buy viagra in japan

[url=http://thjsildenafiljkvc.com/#]viagra without doctor prescription[/url]

sildenafil generic india

viagra and high blood pressure

http://cialpharmedi.com/

brand name viagra no prescription

generic cialis

female viagra pills

order cialis

generic viagra united states

viagra without script

can you take half viagra pill

[url=http://thjsildenafiljkvc.com/#]viagra without script[/url]

get samples viagra

can you buy viagra over the counter at boots

viagra without doctor

tell if viagra pill real

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor[/url]

viagra generico normon

viagra chicago buy

viagra without a doctor visit

where can i get viagra for free

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor visit[/url]

buying viagra online in canada

sildenafil citrate tablets 100mg how to use

viagra without doctor

viagra online compare prices

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

viagra dosis 25 mg

ordering viagra from uk

viagra without a doctor's prescription

viagra online with a prescription

[url=http://thjsildenafiljkvc.com/#]viagra without a prescription[/url]

can viagra pill be split

fruit machine hire london

[url=http://www.ferienwohnungen-rastatt.de/?option=com_k2&view=itemlist&task=user&id=156568]online roulette offers[/url]

no deposit bonus codes uk

online casino franchise

buy cialis safely online

cialis prices

cialis buy online uk

[url=http://cialisdmngj.com/#]cialis cost[/url]

buy cialis online with prescription

discount brand cialis

cialis prices

best discount cialis

[url=http://cialisdmngj.com/#]cialis price[/url]

buy cheap cialis link online

buy cialis no prescription in uk

cheap cialis online

viagra and cialis for sale

[url=http://cialisdmngj.com/#]cialis price[/url]

cheapest place buy cialis

can you buy cialis over the counter in canada

cheap cialis online

cialis pills look like

[url=http://cialisdmngj.com/#]cialis cost[/url]

buy cialis johor bahru

missouri payday loan

[url=https://loanstrast.com/]rapid advance[/url]

sell your

tribal loans

[url=https://loansfast.us.com/]payday loans richmond va[/url]

free loan

i need a loan today

buy cialis delhi

cheap cialis online

buy cialis generic online

[url=http://cialisdmngj.com/#]cheap cialis online[/url]

cialis canada order

cheap authentic cialis

cheap cialis online

buy cialis from uk

[url=http://cialisdmngj.com/#]cheap cialis online[/url]

cialis viagra levitra sale

cheap real viagra uk

viagra without prescription

viagra prices usa

[url=http://viagrahukic.com/#]viagra without prescription[/url]

generika viagra aus eu

caverject and viagra together

viagra without a doctor's prescription

buy viagra cheap online no prescription

[url=http://viagrahukic.com/#]viagra without a doctor's prescription[/url]

how old you have to be to buy viagra

best place to buy cialis on line

buy cialis online

buy cialis without doctor prescription

[url=http://cialismbvi.com/#]buy cialis[/url]

buy cialis in mexico

cash till payday

[url=https://loanstrast.com/]payday loans for bad credit[/url]

greenwood loans

money today

cialis sale

cialis 10 mg

buy now viagra cialis

[url=http://cialisemk.com/]buy cialis online[/url]

buy cialis generic canada

order cialis online uk

cialis online

buy cialis online new zealand

[url=http://cialismbvi.com/#]cialis online[/url]

buy cialis online in canada

mail order cialis generic

cialis prices

cialis for sale in usa

[url=http://cialismbvi.com/#]cialis prices[/url]

can you cut cialis pills

best place to buy cialis

buy cialis

does cialis pills look like

[url=http://cialismbvi.com/#]cialis prices[/url]

buy cialis no prescription

cash advance usa

[url=https://loanstrast.com/]quick easy loans[/url]

money lenders

loans direct

1000 loans

[url=https://loanstrast.com/]i need cash[/url]

fast personal loans

payday loans direct lender bad credit

sildenafil 50 mg cuanto cuesta

viagra cost

viagra generico frete gratis

[url=http://viagramndet.com/#]viagra price[/url]

long does 100mg viagra work

viagra to buy uk

viagra prices

viagra sale manchester

[url=http://viagramhbfe.com/#]viagra coupons 75 off[/url]

best place order viagra online canada

pay advance

[url=https://loanstrast.com/]quick loans for bad credit[/url]

easy loan

new payday loans

efectos del sildenafil 100mg

viagra coupons 75 off

can you get pregnant on viagra

[url=http://viagramhbfe.com/#]best price for viagra[/url]

buy generic viagra in the uk

cialis for sale in london

cialis coupons printable

how to use cialis 20mg tablets

[url=http://cialisopghe.com/#]coupon for cialis[/url]

very nice site cheap cialis

buy cialis miami

cialis coupons printable

cialis super active 20mg pills

[url=http://cialisopghe.com/#]cialis coupons printable[/url]

cialis pills men

loans online

[url=https://loanstrast.com/]loans online[/url]

payday loans

payday loans

generic cialis cheap canada

cialis coupons

cialis pills south africa

[url=http://cialisopghe.com/#]cialis coupons 2017[/url]

cialis liquid for sale

where can i buy real levitra online

levitra 20 mg

levitra sale online

[url=http://levitraklnbi.com/#]levitra coupon[/url]

levitra buy uk

buying levitra online safe

levitra coupon

meds sale levitra

[url=http://levitraklnbi.com/#]viagra vs cialis vs levitra[/url]

cheapest levitra canada

buy levitra professional online

levitra online

buy levitra next day delivery

[url=http://levitraklnbi.com/#]levitra online[/url]

cheap levitra in canada

payday loans online

[url=https://loanstrast.com/]online loans[/url]

loans online

payday loans online

cheapest cialis

cialis without a doctor prescription

viagra or cialis for sale

[url=http://cialisfbvne.com/#]cialis without prescription[/url]

buy cialis soft cheap

discount canadian cialis

cialis without prescription

where to order cialis in canada

[url=http://cialisfbvne.com/#]cialis without doctor[/url]

buy genuine cialis online

get off viagra

viagra without doctor

order viagra india online

[url=http://viagramnkjm.com/#]viagra without doctor[/url]

buy 1 viagra

loans online

[url=https://loanstrast.com/]payday loans bad credit[/url]

payday loans bad credit

loans online

generic viagra release

viagra without a prescription

how can i buy viagra in dubai

[url=http://viagramnkjm.com/#]viagra without a doctor's prescription[/url]

is viagra pills safe

pay day loans

[url=https://smajloans.com/]payday loans[/url]

payday advance

payday loans

[url=https://loanstrast.com/]online loans[/url]

cash loans

cash advance

[url=https://loansfast.us.com/]payday loans no credit check[/url]

online loans

payday loans online

getting best out viagra

viagra without a prescription

tem que ter receita medica para comprar viagra

[url=http://viagramnkjm.com/#]viagra without prescription[/url]

how long does 25mg of viagra last

generic viagra 100mg sildenafil

viagra without a doctor

viagra on sale

[url=http://viagramnkjm.com/#]viagra without a doctor’s prescription[/url]

sildenafil citrate generic 100mg

best online casinos to play roulette

casino real money

online casino software usa

[url=http://online-casino.party/#]online casinos[/url]

bonus slots on line

cash advance

[url=https://smajloans.com/]payday advance[/url]

payday loan online

online loans

[url=https://loanstrast.com/]payday loan online[/url]

cash advance loans

cash advance loans

[url=https://loansfast.us.com/]online payday loans[/url]

payday loans online

payday loans no credit check

all best new online casino bonus

online casinos

live casino ukash

[url=http://online-casino.party/#]casino online[/url]

real pc slot machine games

vip slots download casino

casino

black jack card counting

[url=http://online-casino.party/#]casino[/url]

casino online usa players

payday loan online

[url=https://smajloans.com/]payday advance[/url]

online loans

online loans

[url=https://loanstrast.com/]online payday loans[/url]

pay day loans

online payday loans

[url=https://loansfast.us.com/]payday loans[/url]

payday loans online

online loans

order viagra prescription

viagra

cuanto sale el viagra

[url=http://hqviagrajdr.com/]viagra for sale[/url]

how to buy viagra in spain

on line u s casinos

casino real money

casino ladbrokes virtual horses gratis

[url=http://online-casino.party/#]online casinos[/url]

online casino games for blackberry

keno online indonesia

casino real money

online casino $20

[url=http://online-casino.party/#]casino online[/url]

best keno online

online gambling minnesota

casino

jugar a la ruleta online por dinero real

[url=http://online-casino.party/#]casino[/url]

casino toplists

gambling online usa legal

casino online

what is best online blackjack

[url=http://online-casino.party/#]casino real money[/url]

baccarat and site

payday loans online

[url=https://smajloans.com/]payday loans online[/url]

payday loans

payday loan online

[url=https://loanstrast.com/]payday loans no credit check[/url]

pay day loans

payday loans

[url=https://loansfast.us.com/]online loans[/url]

pay day loan

pay day loan

super internet casino

online casinos

golden casino download

[url=http://online-casino.party/#]casino[/url]

keno tickets online

casino sites for us players

online casino

play online roulette wheel

[url=http://online-casino.party/#]casino real money[/url]

baccarat pc game

pay day loan

[url=https://smajloans.com/]cash advance loans[/url]

pay day loan

online payday loans

[url=https://loanstrast.com/]payday advance[/url]

cash advance loans

pay day loans

[url=https://loansfast.us.com/]payday loans no credit check[/url]

pay day loans

online loans

order generic viagra overnight

viagra without a doctor prescription

viagra buy in tesco

[url=http://viagrajnmeo.com/#]viagra without a doctor prescription[/url]

wie sieht eine viagra tablette aus

viagra generic india

viagra without prescription

buy viagra asia

[url=http://viagrajnmeo.com/#]viagra without a doctor[/url]

is 200 mg viagra safe

where to buy viagra in los angeles

viagra without a doctor

when will generic viagra be available in canada

[url=http://viagrajnmeo.com/#]viagra without a doctor's prescription[/url]

do you have have prescription buy viagra

cash advance loans

[url=https://smajloans.com/]online payday loans[/url]

payday loan online

pay day loans

[url=https://loanstrast.com/]cash loans[/url]

payday loans

payday loans no credit check

[url=https://loansfast.us.com/]cash loans[/url]

cash loans

online loans

fast way to get viagra

viagra without a doctor’s prescription

best place to buy viagra online yahoo answers

[url=http://viagrajnmeo.com/#]viagra without prescription[/url]

mail order viagra legitimate

where to get viagra in the uk

viagra without prescription

order generic viagra forum

[url=http://viagrajnmeo.com/#]viagra without a doctor's prescription[/url]

buy viagra new zealand

generic cialis from usa

best erection pills

cialis 100 mg 4 tablet

[url=http://pillshnembn.com/#]erectile dysfunction pills[/url]

legit place to buy viagra

cialis generico come funziona

erectile dysfunction pills

farmacie online cialis generico

[url=http://pillshnembn.com/#]erectile dysfunction pills[/url]

can u buy cialis

where can i buy viagra over the counter in south africa

ed medications

viagra 50mg or 25 mg

[url=http://pillshnembn.com/#]erectile dysfunction pills[/url]

cialis online price comparison

pay day loan

[url=https://smajloans.com/]cash advance loans[/url]

payday loan online

cash loans

[url=https://loanstrast.com/]pay day loans[/url]

online payday loans

payday loans

[url=https://loansfast.us.com/]cash advance[/url]

cash advance

online loans

buy genuine pfizer viagra uk

erection pills

generic4all tadalafil 4 1 0

[url=http://pillshnembn.com/#]ed medications[/url]

buy online viagra forum

buy generic viagra online paypal

ed medications

usa viagra prices

[url=http://pillshnembn.com/#]ed drugs[/url]

bula do viagra 25mg

avis sur cialis 20mg

erectile dysfunction medications

buy kamagra gel uk

[url=http://pillshnembn.com/#]best erection pills[/url]

cialis da 10 mg prezzo

cialis pills expire

cialis on line no pres

buy cialis retail

[url=http://cialisviymw.com/#]cialis without a doctor prescription[/url]

buy cialis online europe

cheap generic cialis uk

cialis without doctor

cialis sale antidoping

[url=http://cialisviymw.com/#]cialis without a doctor's prescription[/url]

cialis 5 mg cheap

cialis buy online

no prescription cialis

how to buy cialis from canada

[url=http://cialisviymw.com/#]no prescription cialis[/url]

buy cialis no rx

is it easy to get prescribed viagra

buy viagra online

get viagra dublin

[url=http://viagrakbg.com/#]buy viagra[/url]

best source for viagra online

viagra price in rupees

viagra prices

can i purchase viagra online

[url=http://viagrakbg.com/#]viagra online[/url]

can i buy viagra over the counter in thailand

generic for viagra joke

buy viagra online

how to get real viagra online

[url=http://viagrakbg.com/#]viagra pills[/url]

was sind viagra pillen

el viagra de 100 mg

buy viagra

viagra will going generic

[url=http://viagrakbg.com/#]buy viagra[/url]

price viagra cialis

sildenafil citrate 100mg x 20 tabletten

viagra online

buy viagra from uk

[url=http://viagrakbg.com/#]viagra pills[/url]

can you take levitra viagra together

free slot games

[url=http://real777money.com/]play casino online[/url]

play casino online

real money casino online usa

cash advance akron ohio

loans for bad credit

personal loans lexington ky

[url=http://paydaymnku.com/]loans for bad credit[/url]

flexible loan

order generic viagra no prescription

buy viagra

price comparison of viagra

[url=http://viagrakbg.com/#]viagra prices[/url]

does vegetal viagra work

order cialis net

cheap cialis

safe order cialis canada

[url=http://cialiskbg.com/#]cheap cialis[/url]

buy generic cialis online no prescription

buy viagra lahore

viagra online

como se llama el generico de viagra

[url=http://hqviagrajdr.com/]viagra online[/url]

getting viagra from your gp

viagra online manchester

how much viagra does cost

viagra pills they

[url=http://viagrangk.com/#]viagra prices[/url]

comprar viagra precisa de receita medica

viagra in deutschland online

viagra cost

viagra 100mg poveikis

[url=http://viagrangk.com/#]viagra prices[/url]

buy viagra in newcastle upon tyne

can you buy viagra vietnam

best price for viagra

viagra e generici

[url=http://viagrangk.com/#]cost of viagra[/url]

cheap viagra cialis uk

buy viagra ebay

cost of viagra

when will viagra have generic

[url=http://viagrangk.com/#]best price for viagra[/url]

viagra for sale in chicago

play casino online

[url=http://real777money.com/]casino games[/url]

free slot games

real money casino online usa

buy viagra cialis levitra.php

viagra prices

prices of viagra levitra and cialis

[url=http://viagrangk.com/#]cost of viagra[/url]

can buy viagra bali

canadian pharmacy

canadian pharmacies online

online pharmacies canada

[url=http://canadaunmfgb.com/#]best canadian mail order pharmacies[/url]

Online Drugstores

payday loans no credit check

[url=https://smajloans.com/]online loans[/url]

online loans

cash advance

when will viagra be in generic form

viagra ohne rezept aus deutschland

trying get pregnant viagra

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

viagra cheap next day delivery

how to buy viagra in singapore

viagra without prescription

4 viagra pills

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

where can you buy viagra for women

tomar viagra com energetico

viagra without prescription

what pill works like viagra

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

viagra 4 sale

viagra new zealand sale

viagra ohne rezept aus deutschland

buying viagra over internet

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

samples of viagra online

where to buy real viagra cheap

viagra ohne rezept aus deutschland

can you get viagra at walmart

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

illegal viagra sales

buy viagra with paypal uk

viagra no script

buying viagra in australia

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

viagra 50 mg yan etkileri

payday loans online

[url=https://smajloans.com/]payday advance[/url]

cash advance

payday loans no credit check

how much does viagra cost per pill at walgreens

viagra no script

viagra online xl

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

online pharmacy get viagra

viagra doses 150 mg

viagra ohne rezept aus deutschland

generic viagra in uk

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

viagra pills in singapore

diferencia viagra viagra generico

viagra no prescription

pramil sildenafil 75 mg

[url=http://bfviagrajlu.com/#]viagra ohne rezept aus deutschland[/url]

legitimate sites buy viagra

generic viagra professional 100 mg

viagra without a doctor prescription

viagra sale auckland

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

generic viagra approved by fda

viagra without prescription

cialis viagra order

[url=http://bfviagrajlu.com/#]viagra ohne rezept aus deutschland[/url]

half pilletje viagra

legitimate viagra online

viagra without a doctor prescription

can you get viagra if you young

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

cheap viagra melbourne

viagra ohne rezept aus deutschland

viagra sale lloyds pharmacy

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

viagra pill available in india

can i buy viagra online in australia

viagra without a doctor prescription

disadvantages of viagra pills

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

sildenafil genericos intercambiables

viagra without a doctor prescription

viagra pills dosage

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

viagra generika kaufen forum

cash advance loans

[url=https://smajloans.com/]payday advance[/url]

cash advance

pay day loans

price comparison levitra viagra

viagra without a doctor prescription

use of cialis and viagra together

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

is it illegal to sell viagra online

viagra no prescription

is it ok to buy viagra online

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

viagra online kaufen ohne kreditkarte

viagra us pharmacy online

viagra without a doctor prescription

sildenafil citrate best price

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

tomar viagra de 100mg

viagra no prescription

feel like viagra pill face

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

comprar viagra manaus

payday loans

[url=https://smajloans.com/]pay day loan[/url]

payday loans online

payday advance

can buy viagra canada

viagra without prescription

get viagra in chicago

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

viagra tablet price in india

viagra ohne rezept aus deutschland

besten viagra pillen

[url=http://bfviagrajlu.com/#]viagra no script[/url]

generic viagra aurochem

payday loans

[url=https://smajloans.com/]payday loans[/url]

payday loans

payday loans no credit check

can you buy viagra without perscription

viagra without prescription

can order viagra

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

comprar viagra generico no brasil

viagra no prescription

how do viagra pills look like

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

can you buy viagra in london

viagra vanzare

[url=http://viagrahsk.com/]buy viagra online[/url]

generic viagra online

viagra usa buy

viagra without a doctor prescription

acquistare viagra generico in europa

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

how to get rid of viagra email virus

viagra no script

ordering viagra over the internet

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

get sample viagra

buy generic viagra with american express

viagra without a doctor prescription

legal order viagra online canada

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

generic viagra buy uk

viagra ohne rezept aus deutschland

buy viagra 25mg online

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

can you get viagra over the counter in spain

sildenafil citrate 130 mg

viagra without a doctor prescription

viagra generico en brasil

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

can you buy viagra amsterdam

viagra no prescription

sildenafil 100mg marham daru

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

best way to get viagra online

viagra achat europe

[url=http://www.chst9.com/home.php?mod=space&uid=145622]generic cialis online[/url]

cheap cialis

[url=http://www.ferienwohnungen-rastatt.de/index.php?option=com_k2&view=itemlist&task=user&id=293039]generic cialis online[/url]

cialis canada

[url=http://truck.zzcn.org/home.php?mod=space&uid=189153]buy cialis[/url]

cialis online

[url=http://bbs.chinatex.org/home.php?mod=space&uid=706103]cialis cheap[/url]

generic cialis

[url=http://www.fiberoptika.net/index.php?action=profile;u=10703]generic cialis[/url]

cheap cialis

sildenafil citrate oral jelly 100mg

viagra without prescription

buy viagra england

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

get prescription viagra online

viagra no script

is it safe to take 2 50mg viagra

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

facts about viagra pills

buy uk viagra online

viagra without prescription

map html buy viagra

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

sildenafil citrate tablets 100mg nizagara

viagra without a doctor prescription

pastillas sildenafil 50 mg

[url=http://bfviagrajlu.com/#]viagra ohne rezept aus deutschland[/url]

viagra generico vendita on line

payday loans online

[url=https://smajloans.com/]payday loans[/url]

payday loans

payday loans

payday loans online

[url=https://smajloans.com/]payday loans no credit check[/url]

payday loans

payday loans no credit check

viagra online buy australia

viagra without prescription

can buy viagra yahoo

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

viagra 100mg pfizer wirkungsdauer

viagra no prescription

extenze and viagra together

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

can buy viagra over counter australia

can you get viagra over the counter in mexico

viagra without a doctor prescription

where to buy viagra in stores

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

pillole simili al viagra

viagra without a doctor prescription

where to buy viagra online ireland

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

viagra t recubierta 4 100 mg

online viagra sales in australia

viagra cost

anyone use generic viagra

[url=http://sildenafilmkfbv.com/#]viagra cost[/url]

viagra 100mg vs cialis

viagra scaffolding australia

[url=http://v2indian.com/]sildenafil generic india[/url]

generic viagra india pharmacytesco viagra

[url=http://viagragche.com/]buy viagra[/url]

buy viagra onlinebuy cialis in america cheap

[url=http://cialisdfr.com/]buy cialis[/url]

generic cialis

can you buy viagra over the counter

viagra cheap

viagra sales 2008

[url=http://sildenafilmkfbv.com/#]cheap viagra[/url]

can you get viagra from walgreens

street cost of viagra 2012

[url=http://cheaapviagraonlis.com/]sildenafil online[/url]

generic viagra online

casino games list

[url=http://casinoline17.com/]online casino games[/url]

online casino

п»їcasino online

payday loans no credit check

[url=https://smajloans.com/]payday loans no credit check[/url]

payday loans online

payday loans no credit check

cialis online order

cheap cialis

buy cialis walmart

[url=http://naqsehuki.com/#]order cialis online[/url]

cheap viagra cialis online

generic viagra plus online

[url=http://v2indian.com/]viagra india[/url]

sildenafil generic india

can you buy cialis over the counter

buy cialis online

generic cialis cheap

[url=http://naqsehuki.com/#]order cialis online[/url]

cialis buy online canada

bad credit no payday loan

payday loans

bad credit consolidation loans

online loans

payday loans online no credit check

[url=http://paydaynock.com/]payday loans online no credit check[/url]

payday loans no credit check

payday loans no credit

cialis buy nz

buy cialis online

what cialis pills look like

[url=http://naqsehuki.com/#]order cialis online[/url]

order cialis india

payday loans online no credit check

[url=http://paydaynock.com/]payday loans no credit[/url]

payday loans no credit check

payday loans no credit

buy generic levitra 10 mg

vardenafil 20mg

cheapest viagra cialis levitra

[url=http://levitradbws.com/#]levitra[/url]

cheapest generic levitra online

levitra 20 mg

where to buy generic levitra online

[url=http://vardenafilghns.com/#]vardenafil[/url]

meds sale levitra

cialis cheap fast delivery

generic cialis

how to order cialis online

[url=http://cialisyrudgj.com/#]buy generic cialis online[/url]

cialis for sale online

cialis price

cialis viagra sale canada

[url=http://cialisuitykh.com/#]cialis price[/url]

how to buy viagra or cialis

generic cialis in vietnam

[url=http://live.hongrun.biz/home.php?mod=space&uid=365565]buy viagra[/url]

buy generic viagra

[url=http://diendan.musaigon.vn/member.php?124007-Tamararaw]viagra cheap[/url]

buy generic viagra

[url=http://saudionline.co.uk/index.php?option=com_k2&view=itemlist&task=user&id=223824]viagra cheap[/url]

buy viagra online

[url=http://forums.wac.ps/member/9642-molofeevaskymn]cheap viagra[/url]

cheap viagra

[url=http://www.other.rasmeinews.com/index.php/component/users/?option=com_k2&view=itemlist&task=user&id=5303515]online viagra[/url]

viagra cheap

where to purchase cialis cheap

generic cialis

where to buy cialis in usa

[url=http://cialisyrudgj.com/#]generic cialis[/url]

cialis discount offers

cialis price

buy cialis daily dose

[url=http://cialisuitykh.com/#]cialis price[/url]

buy cialis using paypal

payday loans no credit

[url=http://paydaynock.com/]payday loans no credit[/url]

payday loans no credit

payday loans no credit check

comprar generico do viagra em portugal

buy viagra

buy generic viagra and cialis online

[url=http://viagratutrjdsd.com/#]viagra online[/url]

venden viagra generico en farmacias similares

cheap viagra online

manufacturer of generic viagra

[url=http://viagraeyefbdj.com/#]online viagra[/url]

where to buy womens viagra

viagra pill available in india

viagra online pharmacy

reliable place to buy viagra

[url=http://viagratutrjdsd.com/#]buy viagra online[/url]

order viagra online canadian no prescription

generic viagra online

viagra cheapest

[url=http://viagraeyefbdj.com/#]viagra online[/url]

utilisation viagra 50mg

cheap canadian cialis online

best price cialis

buy cialis no prescription mastercard

[url=http://cialisietwdffjj.com/#]cialis price[/url]

order cialis from mexico

cialis prices

buy cialis us pharmacy

[url=http://cialisytigjtuj.com/#]cialis cheap[/url]

cialis daily use discount

free casino games

[url=http://bom777casino.com/]п»їcasino online[/url]

casino games

real money casino

prix de cialis en inde

[url=http://cialisjqp.com/]cialis cheap[/url]

cialis cheapcialis 10mg 120 tabs

[url=http://cialisnji.com/]generic cialis[/url]

cialis cheapeasy financial loan calculator

[url=http://soloadvance.com/] pay day loans[/url]

personal loans

online casino

[url=http://bom777casino.com/]casino online[/url]

real money casino

casino games

using viagra get over performance anxiety

viagra without a doctor prescription

tomei viagra 100mg

[url=http://viagrarutjdfk.com/#]viagra without a prescription[/url]

viagra type pills

viagra cost

what happens if i take two viagra pills

[url=http://viagrajretnfc.com/#]cheap viagra[/url]

duane reade viagra price

cheap viagra professional

viagra without presciption online

get prescription for viagra online

[url=http://viagrarutjdfk.com/#]viagra without prescription[/url]

buy excel herbal viagra

viagra cost

how to get viagra in singapore

[url=http://viagrajretnfc.com/#]viagra price[/url]

what are viagra pills yahoo

viagra type pill women

viagra without prescription

which pill is better viagra cialis or levitra

[url=http://viagrarutjdfk.com/#]viagra without presciption online[/url]

pfizer viagra vs generic viagra

viagra price

donde puedo comprar viagra por internet

[url=http://viagrajretnfc.com/#]viagra cost[/url]

can u buy viagra over the counter in uk

casino games

[url=http://bom777casino.com/]casino online[/url]

real money casino

free casino games

we recommend low price cialis

[url=http://cialisjqp.com/]generic cialis[/url]

buy cialiscialis generico migliore

[url=http://cialisnji.com/]cialis[/url]

buy cialis onlinecash loans in gaffney sc

[url=http://soloadvance.com/] loans for bad credit[/url]

payday express

casino games

[url=http://bom777casino.com/]free casino games[/url]

online casino

real money casino

casino games

[url=http://bom777casino.com/]free casino games[/url]

free casino games

real money casino

online bingo for cash

online casino

new online casinos south africa

[url=http://online-casino.party/#]online casinos[/url]

online video poker game

best us friendly online casinos

casino online

online casino us players echeck

[url=http://online-casino.party/#]casino online[/url]

online gambling casino vegas

freeslots

[url=http://casinobablogames.com/]free slot games[/url]

casino slots

free slots online

slotomania free slots

[url=http://casinobablogames.com/]free slots games[/url]

free casino games no download

slots free

free casino games slot machines

[url=http://casinobablogames.com/]free casino games slot machines[/url]

free slots online

online casino real money

debt management programs

personal loans

payday loan cash advance

pay day loans

slots casino

[url=http://casinobablogames.com/]casino free games[/url]

casino games slots

free casino games slot machines

branded viagra

buy generic viagra

cheap brand name viagra

buying viagra ’

casino free games

[url=http://casinobablogames.com/]slots casino games[/url]

casino slot games

free casino games slots

autodesk autocad 2011 serial number and product key

autocad student

autocad product key 2011 serial number

[url=http://autocadtymafq.com/#]autocad lt[/url]

autocad serial key 2012

autocad 2018

product key autocad lt 2014

[url=http://autocadbnaqk.com/#]autocad 2017[/url]

downloading autocad 2017

autocad online schools

autocad software

autocad 2013 lt vs full version

[url=http://autocadbmjes.com/#]autocad download[/url]

autocad where to buy

autodesk autocad

buy autocad for mac

[url=http://autocadtfesvb.com/#]autocad 2018[/url]

autocad student serial number

loans no credit

[url=http://paydayhjkfg.com/]loans for bad credit[/url]

loans no credit

loans for bad credit

buy viagra now uk

online viagra

viagra generico bula

[url=http://viagrayityjg.com/#]viagra online[/url]

viagra dubai buy

best price viagra

hard sell evolution viagra salesman plot summary

[url=http://viagramhkdyl.com/#]cheap viagra[/url]

generic soft tab viagra

order cialis viagra

order viagra online

viagra and high blood pressure pills

[url=http://viagrayityjg.com/#]order viagra online[/url]

viagra online italia

viagra cheap

best sildenafil tablets in india

[url=http://viagramhkdyl.com/#]viagra cheap[/url]

sildenafil citrate soft tablets 100mg

viagra tijuana prices

online viagra

non generic viagra online

[url=http://viagrayityjg.com/#]buy viagra[/url]

buy viagra pills

viagra prices

use viagra and cialis together

[url=http://viagramhkdyl.com/#]viagra prices[/url]

1 pill viagra

cialis 10mg vs 20mg

free cialis

order cialis ’

buy cialis with money order

cheap cialis

buy cialis uk no prescription

[url=http://cialisghkgfjm.com/#]cheap cialis[/url]

how to buy cheap cialis

generic cialis

buy cialis professional 20 mg

[url=http://cialistrihfy.com/#]generic cialis[/url]

cialis pills sale

cheap viagra mastercard

viagra without a prescription

viagra cialis levitra price comparison

[url=http://viagrayirib.com/#]viagra without a doctor prescription[/url]

cheap safe viagra

viagra coupons

is generic viagra available in canada

[url=http://viagrahkfy.com/#]viagra prices[/url]

sildenafil viagra generic

get viagra bangkok

viagra without a doctor prescription

viagra online australia net

[url=http://viagrayirib.com/#]viagra without script[/url]

can you buy viagra over the counter boots

viagra coupon

to buy cheap viagra

[url=http://viagrahkfy.com/#]viagra[/url]

can i take half viagra pill

casino online

[url=http://casinobablogames.com/]online casino[/url]

online slots

real money casino

brand cialis for sale

buy cialis

legal buy cialis online

[url=http://cialisbhascse.com/#]cialis prices[/url]

cheap cialis sale

cialis prices

discount cialis no prescription

[url=http://cialistgaveff.com/#]cialis generic[/url]

purchase cheap cialis soft tabs

cialis wholesale

cialis 100mg

cialis coupon ’

autocad inventor professional suite 2017 download

autodesk inventor

online autocad drafting work

[url=http://autodeskoutyk.com/#]autodesk 360[/url]

autocad 2011 download full

auto cad

autocad osx download

[url=http://autocadmnfheru.com/#]autocad[/url]

autocad electrical 2017 serial and product key

real money casino online

[url=http://bablcasinogames.com/]sizzling 777 slots free online[/url]

456 free slots casino

best us casinos online

cheap levitra australia

levitra online

cheap levitra line

[url=http://levitranthdi.com/#]levitra online[/url]

levitra sale philippines

vardenafil generic

levitra 20 mg cheap

[url=http://vardenafildtudf.com/#]vardenafil 20 mg[/url]

best website buy levitra

buy levitra discount

levitra 20 mg

buy levitra in thailand

[url=http://levitranthdi.com/#]levitra 20 mg[/url]

how do i buy levitra

vardenafil generic

cheapest levitra

[url=http://vardenafildtudf.com/#]vardenafil generic[/url]

levitra buy australia

viagra sales in uae

viagra without script

viagra potency pill

[url=http://viagrawyrfhdj.com/#]viagra without script[/url]

generic viagra yahoo

viagra prices

fastest way to buy viagra

[url=http://viagrartuudhf.com/#]viagra prices[/url]

viagra sale ireland

viagra discount coupon

buy generic viagra

se puede comprar viagra sin receta en argentina

[url=http://viagrayutkh.com/#]generic viagra online[/url]

cheapest viagra kamagra

cheap viagra

200 mg viagra safe

[url=http://viagratyrif.com/#]viagra pills[/url]

using levitra viagra together

buy generic cialis online no prescription

cialis coupons 2018

order generic viagra cialis

[url=http://cialisruyfk.com/#]cialis coupon[/url]

buy cialis dubai

cialis without doctor

do cialis pills expire

[url=http://cialisuotukhfh.com/#]cialis without doctor[/url]

buy cialis overnight

funziona il viagra generico

viagra without prescription

viagra online next day delivery

[url=http://viagrayitykckg.com/#]viagra no prescription[/url]

safest way buy viagra line

generic sildenafil

venta viagra online mexico

[url=http://sildenafiletudgj.com/#]generic sildenafil[/url]

cheap viagra tablets uk

online gambling sites for real money

[url=http://casinoveganonline.com/]online gambling casino[/url]

free online casino slots

aol games free casino

qual o nome dos genericos do viagra

viagra without prescription

can buy viagra indonesia

[url=http://viagrahlsacft.com/#]viagra without a prescription[/url]

how to get viagra for free

generic viagra

viagra preiswert online kaufen

[url=http://viagravbndcvef.com/#]generic viagra online[/url]

buying viagra in australia online

caverta cheap cialis generic viagra

viagra without a prescription

viagra sale dublin

[url=http://viagrahlsacft.com/#]viagra without a doctor's prescription[/url]

viagra 200mg dose

viagra generic

where to get cheapest viagra

[url=http://viagravbndcvef.com/#]generic viagra 100mg[/url]

get off viagra spam list

has anyone ever ordered viagra online

viagra without prescription

viagra buy online canada

[url=http://viagrahlsacft.com/#]viagra without prescription[/url]

getting viagra without a doctor

viagra generic

buying viagra in the philippines

[url=http://viagravbndcvef.com/#]generic viagra[/url]

online pharmacy low price viagra

cialis for sale in philippines

cialis cialis prices

buy cialis nz

[url=http://cialiskkg.com/#]buy cialis online[/url]

cheapest generic cialis canada

generic cialis at walmart

cialis malaysia where to buy

[url=http://cialisdcfev.com/#]generic cialis[/url]

generic.cialis.pills

generic super cialis uk

[url=http://cialisdfr.com/]generic cialis[/url]

cialisviagra femm

[url=http://viagralkq.com/]viagra professional[/url]

generic viagra onlinewe like it buy cialis where

[url=http://cialistas.com/]cialis cheap[/url]

generic cialiscialis original farmacia

[url=http://cialisbva.com/]cialis[/url]

buy cialis

cialis pills amazon

tadalafil generic

buy cialis from australia

[url=http://cialisdskew.com/#]tadalafil generic[/url]

how to split pills cialis

cialis cialis prices

original cialis pills

[url=http://cialisggr.com/#]cialis cialis prices[/url]

cheap canadian cialis online

can buy cialis uk

generic cialis tadalafil

cheap cialis online uk

[url=http://cialisdskew.com/#]tadalafil generic[/url]

cheap cialis super active

cialis generico online

where to buy cialis no prescription

[url=http://cialisggr.com/#]cialis online[/url]

buy now viagra cialis

best diet pill

[url=http://regimenforfeit.com/]best diet supplements[/url]

best supplements for weight loss

lose weight fast

can u buy viagra over counter

[url=http://viagralkq.com/]viagra online[/url]

viagra cheapclick here cialis soft tablets

[url=http://cialistas.com/]buy cialis[/url]

cialis onlinetarif cialis andorre

[url=http://cialisbva.com/]cialis[/url]

generic cialis online

cheapest way to buy cialis

generic cialis at walmart

order cialis viagra

[url=http://cialisdskew.com/#]generic cialis tadalafil[/url]

what are cialis pills used for

buy cialis online

cheap brand name cialis

[url=http://cialisggr.com/#]cialis online[/url]

buy cialis in europe

cialis pills in uk

generic cialis at walmart

buy cialis online in u.k

[url=http://cialisdskew.com/#]generic cialis tadalafil[/url]

pharmacy has cheapest cialis

cialis generico online

cialis uk cheap

[url=http://cialisggr.com/#]cialis generico online[/url]

how to buy generic cialis

order cialis mexico

generic cialis at walmart

small order cialis

[url=http://cialisdskew.com/#]generic cialis[/url]

buy cialis cheap online

buy cialis online

can i buy cialis over the counter in canada

[url=http://cialisggr.com/#]cialis cialis prices[/url]

buy levitra cialis

viagra con receta espana|viagra professional australia|viagra online pharmacy india|buy viagra 50 mg online|ik wil viagra bestellen|vente viagra kamagr|compra viagra online espana|meilleur site achat viagra|the best site viagra sales|femminile viagra|viagra cost without insurance|tabs viagra 50mg 100mg|cialis viagra best price|are generic viagra any good|a free sample of viagra|buy cheapest generic viagra|viagra to order|click now viagra 25 mg order|viagra kautabletten|viagra usa kauf|australia viagra barata|viagra 60mg|viagra pfizer teva|buy pills like viagra|cialis viagra onlin|most recognized brand viagra|viagra im internet gefahrlich|viagra dnemark rezeptfrei|the best female viagra|viagra generische cialis|cheap viagra fast|viagra soft tabs dosage|pl viagra|frauen viagra verkauf online|usefull link viagra online buy|viagra 25 effett|assunzione viagra cialis|pharmatheke viagra|viagra 100mg long does last|vente viagra naturel|click now online viagra in u s|viagra comment fair|discount viagra rx|is generic viagra legal|viagra per pill cost uk|only here viagra buy uk|viagra online discreet|we use it buy viagra us|viagra edrugstore|mytabs viagra|prix officiel viagra belgique|viagra victoria australia|safest cheapest viagra|viagra 100 street price|order viagra soft|shoud you buy viagra|viagra vs cialis forum|venta de viagra ny|can you drink alcohol viagra|delivery uk fast viagra|donde comprar viagra en la web|viagra y derivado|viagra india|order viagra over phone|follow link viagra pill|womens viagra forum|cheap viagra ontario|buy viagra online uk paypal|cost of viagra jelly|viagra generic soft tabs 50mg|buy viagra here in the uk|viagra and levitra dosage|use of viagra jelly|is maximum dosage for viagra|generic versions of viagra|viagra en pharmacie tunisie|pfizer viagra 100mg women|mejor viagra o cialis|buy viagra gold coast|viagra vendita offerta|50 mg viagra not working|tesco pharmacy online viagra|compare viagra prices|buy pharmacy generic viagra|pfizer viagra achat canada|viagra abu dhabi|viagra rezept arzt|stamina rx vs viagra|buy viagra t shirt|pfizer viagra prezzo|buy female viagra with e check|viagra levitra and tadalafil|click now viagra mail order|cheapest viagracouk|acheter viagra qualit|viagra ecstasy|viagra effet contraire|viagra en oferta|viagra in taiwan|best viagra jelly prices|viagra real mail|viagra sperm count|viagra ejaculation precoce|prix du viagra pfizer|buy viagra onli ne|viagra avec cialis|is viagra bad for the heart|when do take a viagra pill|buy viagra in malaysi|brand viagra over the net|generic viagra illegal|viagra teenage use|buy viagra in nigeria|viagra cialis experiencias|viagra online a href|canada pharmacy viagra 25mg|order cialis vs viagra|price of a viagra pill|viagra cialis precios|fast viagra uk|newest viagra|le viagra pourquoi|is generic viagra avaikable|viagra reacciones adversa|discount viagra samples|we choice viagra tablets|click here viagra headaches|inc viagra india|viagra osterreich bestellen|viagra pens for sale|viagracanada|generic viagra wholesale price|are branded indian viagra safe|is viagra available in generic|cheap viagra or sale|buy real viagra coat sale|does generic viagra work|viagra sans ordonnance magasin|viagra 50mg for sale ireland|viagra rezept online erhalten|viagra blood pressure drop|viagra 25 mg tab|wow look it woman and viagra|dosis viagra efectos|how to buy viagra in abu dhabi|viagra feminin sans ordonnance|cialis viagra espana|viagra es con receta medic|online website viagra|viagra subistute|pfizer viagra vendita|viagra chewable tablets|viagra potenzmitte|sizes viagra|dangers of viagra abuse|where can i buy viagra in usa|visit web site ordering viagra|viagra kaufen mit rezep|sildenafil viagra pfizer|viagra tylenol trial|buy viagra in phuket|best viagra to buy online|prix de viagra rx|lgislation suisse viagra|mail order viagra jelly|we like it viagra prices|movie viagra sales|viagra gold pris fass|history of viagra sales|visit our site brand viagra|sconto di viagra di erba|onet viagra pharmacy|viagra soft mg buy|super viagra beads|cheap viagra online ireland|buying viagra in australia|dove acquistare viagra lin|wirkungsdauer levitra viagra|viagra sale los angeles|viagra cost nz|lowcostviagra|viagra vrai pas cher|viagra pakistan price|viagra order in india|achat viagra pfizer|mejor viagra herbario|viagra as performance booster|comprar viagra en europa|take sotalol and viagra|wow look it viagra tab|will viagra become generic|canada generic viagra pharmacy|viagra espaa farmacias|generic viagra best price|can tou get pregnant on viagra|10mg vs 20mg viagra|viagra prices from walmart|viagra zu teuer|only here viagra injectable|advertised on fox viagra|viagra costco over the counter|rezeptfreie viagra|compro viagra en valencia|private label herbal viagra|generic viagra gel|pillole viagra|pfizer viagra 50mg flashback|viagra alternatives|buy viagra in kenya|viagra preis deutschlan|viagra kaufen einzeln 100mg|prezzo basso viagra generico|best herbal viagra reviews|genericos de viagra en chile|red cialis viagra drug|serios viagra bestellen|viagra auf rechnung online|viagra at gnc|pfizer viagra dosage|viagra cost sa|viagra price made pfizer|viagra kostenlos|precio viagra farmacia|viagra samples free pfizer|viagra generique teva|visit our site take viagra|visit our site viagra fast|ja existe generico do viagra|order viagra online safe|viagra utrecht|100mg super viagra 60mg|viagra online for sale cheap|viagra 50 o 100 mg|visit web site rx viagra|generic viagra meltabs drug|vendita viagra in contrassegno|can i get viagra at walgreens|cialis compare levitra viagra|tab viagra generic buy|viagra cheap online uk|fda approved viagra sales|viagra use experience|generic viagra safe india|we use it brand name viagra|prix viagra 50 100|generic names of viagra|viagra tablet bestellen|viagra plus cost comparison|female viagra sale uk|buy viagra viagra

[url=http://viagracheapbyg.com/]viagra,cheap viagra,buy viagra,generic viagra,viagra online,buy viagra online,viagra,viagra cheap,online viagra[/url]

viagra,cheap viagra,buy viagra,generic viagra,viagra online,buy viagra online,viagra,viagra cheap,online viagra