This is great. I'd like to do the same for my portfolio. What software / website are you using to track the model portfolio?

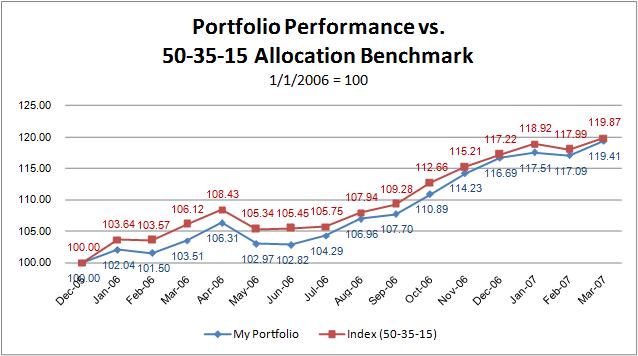

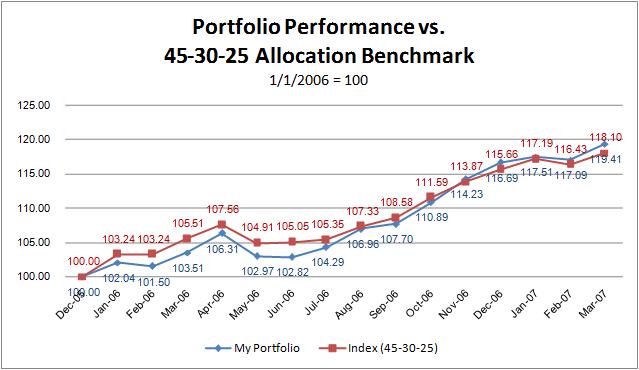

MM - I'm really glad you're doing this. It will be very interesting going forward to see how you do. I'll make the forecast now that you'll under-perform the index by at least 100 basis points on average. From the 2nd graph your portfolio ended ahead of the 45-30-25 benchmark only 2 months out of 16. If you were playing baseball you'd be batting .125.

Regarding the comment regarding lower volatility, did you calculate the standard deviation of your portfolio vs. the benchmark, or are you using qualitative factors to make this assessment? I'd be curious to see what each portfolio returned in terms of % return / standard deviation.

I think right now that it is very hard to find compelling investment options in any asset class, and that maintaining a large risk-free pool of cash is not a terrible place to be. You mentioned dollar-cost-averaging the cash into equities; this is probably the best bet, maybe over over a span of 2-3 years or so. Everything is priced so high right now, I'd be afraid to put a lot of cash to work immediately, especially in foreign/emerging markets.

Your results show no statistically significant outperformance whether modelled with your true cash allocation or your goal. Even with a 1.3% outperformance quaoted you would need to demonstrate that consistently for roughly ten years for it to be statistically significant. Why not save all your time and just invest in your benchmark ETFs? It would have solved your "too much cash" problem last year as you searched for suitable investments.

The other way is to put 90% in your benchmarks and actively manage the remaining 10% so you can continue to develop active investment skills. When you have a statistically significant outperformance in the 10% that is the time to actively manage the remainder.

Something to strongly consider when you decide to make shifts in your portfolio is what the tax consequences are. If you have been investing for 10 years, you could easily have a 40-100% capital gain that you will owe taxes on. If MM is doing OK with actively managed mutual funds, the loss to capital could easily outway any gains he could potentially make from switching to ETFs or index funds. It would be better to keep what he has and to plan to dedicate any future purchases to index funds/ETFs.

MM - I'm not sure how you don't qualify as an 'active' investor; as far as I can tell, only about $6,000 of your $750,000 portfolio is invested in index funds. If I were you, I'd sell all the equity positions (to the extent possible), put $600k in the IFA 100 portfolio, and plan on dollar-cost-averaging the leftover cash into the IFA 100 over the next few years.

I apologize for mis-reading your graph, and for always seeming so cynical. I really appreciate the service you provide by laying your financial life bare for the world to pick apart.

I would stick with the S&P500 benchmark. Sure you don't take the varying risk into account, but you get an idea of whether its worth your time to bother actively managining your funds.

The two basic options you have are to either:

1)wory about picking stocks/funds/diversifaction into international markets

2)just dump everything you earn into a bread and butter ETF (likely tracking the S&P500)

Otherwise, what's the point of personal benchmarking? Generally you seem equally interested in your return on time, as well as return on capital. Even with 700k in assets, maybe you have something you could do with your time that returns more $/hour than personal asset allocation?

If you have no passion for learning businesses in-depth, identifying and owning best of the bread. If being an average and be averagely paid in exchange for doing nothing, settles fine with you. IFA 100 is a way to go.

However, for those adventurous, persistent souls who wish to learn it would be a poor proposition.

Of course benchmark is helpful to know where you stand compared to the average, but there is no need to be mesmerized by it, especially if you got privilege of time.

Here is a quote I like - �Formula for success: Rise early, work hard, strike oil.� -

Paul Getty.

I would agree with John on this one.

The S&P is one of the best benchmark available and should give you a correct comparative mark. Of course it is not optimized. But to some point, tracking results should not take too much of your time.

It seems that there are two debates going on here.

1) Should MM benchmark against the S&P500, or something else?

2) Should MM be an active or passive investor?

I don't see how there can be any debate as to the first question; MM has a portfolio that is heavily weighted to foreign equities; therefore, to see if he is making progress, he should compare himself to a benchmark that reflects the performance of such a portfolio. There isn't a lot of room to debate the logic of his (correct) decision to compare the return of his portfolio against a blended return, as provided by the S&P500 and MSCI EAFE, which are both widely-followed and tracked.

The second question is probably the most hotly debated dilemma in the history of finance. MM has sealed the debate regarding his portfolio; he feels that with time, education and experience he will perform better than the market. That is fine; he as about $650,000 more investable dollars than I do, and he can do what he wants. However, both academic theory and historical performance (of investors in general, not MM specifically) would indicate that MM will fail to perform at or above the index averages, but he (and we) will certainly have fun watching him try.

Great read. I think I'll subscribe to this as it has some good info! Thanks. I do apppreciate the blog :-)

Great read. I think I'll subscribe to this as it has some good info! Thanks. I do apppreciate the blog :-)

h canadian pharmacy reviews felt [url=http://canpharmacyyc.com]canadian online pharmacy[/url] canadian pharmacy online

x buy levitra online cause [url=http://levitrayc.com]buy vardenafil[/url] levitra

v generic viagra online whose [url=http://viagrayc.com]generic viagra online[/url] sildenafil

sildenafil 130mg

viagra without doctor

buy 5 viagra pills

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

herbal viagra prices

selling viagra online

viagra without doctor

cutting 50mg viagra in half

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

order viagra cialis

tramadol addiction potential

alcohol rehab centers

morphine addiction treatment

[url=http://drugrehabtrustedclinic.com/]drug addiction rehab centers[/url]

detox from hydrocodone

cocaine side effects eyes

alcohol rehab centers

alcohol and zolpidem

[url=http://drugrehabtrustedclinic.com/]alcohol rehab facilities[/url]

rehabilitation center

signs of substance abuse

alcohol rehab

heroine recovering addicts

[url=http://drugrehabtrustedclinic.com/]alcohol rehab houston[/url]

evidence of cocaine use

side effects of doing coke

alcohol rehab facilities

addiction research

[url=http://drugrehabtrustedclinic.com/]alcohol rehab centers[/url]

effects of meth on the body

[url=http://wellbutrin.shop/]wellbutrin[/url] [url=http://bupropion.schule/]bupropion[/url]

cheapest generic cialis uk

buy viagra

[url=http://viagrajfeg.com/]buy viagra[/url]

viagra buy now

cialis online pharmacy

[url=http://cialisdmge.com/]online cialis[/url]

can take levitra viagra together

[url=http://cephalexin250mg.us.org/]Buy Cephalexin[/url] [url=http://cheapvardenafil365.us.com/]VARDENAFIL[/url]

[url=http://nexiumonline.pro/]nexium[/url] [url=http://buy-rimonabant.shop/]buy rimonabant[/url] [url=http://viagra-soft.shop/]viagra soft[/url] [url=http://kamagra.fund/]kamagra[/url]

can you buy cialis over counter usa

cialis canada

cialis 20 mg tablets uk

[url=http://fgocialisgfeb.com/#]cialis online canada pharmacy[/url]

cialis sale canada

CVS Pharmacy

no prior prescription required pharmacy

lloyds pharmacy online uk

[url=http://ehmcanadaufgpharmacypo.com/#]prescriptions online[/url]

epharmacy

payday loan

cash advance online

payday loans 1 hour

payday advance loans ’

[url=http://colchicine247.us.com/?gm,buy,power]gm buy power[/url] [url=http://colchicine247.us.com/?Wellbutrin;Adjuvant;Depression]wellbutrin adjuvant depression[/url] [url=http://colchicine247.us.com/?Furosemide=20=Mg=Samsung=Galaxy=Tab=8.9]furosemide 20 mg samsung galaxy tab 8.9[/url] [url=http://colchicine247.us.com/?protonix;and;alchohol]protonix and alchohol[/url] [url=http://colchicine247.us.com/?Enalapril=With=No=Prescription]enalapril with no prescription[/url]

canadian pharmacy online viagra

generic viagra

viagra for women

generic viagra ’

cheap cialis rx

buy cialis

how to buy cialis online safely

[url=http://vgcialistylbuyjl.com/#]buy cialis online[/url]

cheap cialis in the usa

[url=http://colchicine247.us.com/?effexor;withdrawal;tips]effexor withdrawal tips[/url] [url=http://colchicine247.us.com/?vet;answers;levaquin]vet answers levaquin[/url] [url=http://colchicine247.us.com/?tramadol=50=mg=buy]tramadol 50 mg buy[/url] [url=http://colchicine247.us.com/?Melatonin;Depakote]melatonin depakote[/url]

[url=http://colchicine247.us.com/?motorola/1200mah/lithium/battery]motorola 1200mah lithium battery[/url] [url=http://colchicine247.us.com/?zoloft=and=subutex]zoloft and subutex[/url] [url=http://colchicine247.us.com/?zolpidem=trileptal=interactions]zolpidem trileptal interactions[/url] [url=http://colchicine247.us.com/?Lithium=Battery=Construction]lithium battery construction[/url] [url=http://colchicine247.us.com/?Buy,Naproxen,Online]buy naproxen online[/url] [url=http://colchicine247.us.com/?Amantadine/Hci]amantadine hci[/url]

viagra generic

buy viagra

natural substitute for viagra

viagra online ’

generic version viagra

buy viagra online to canada

can u cut viagra pills in half

[url=http://vgcialistylbuyjl.com/#]order viagra canadian pharmacy[/url]

price of viagra in mexico

tadalafil generic cialis

cialis online

cialis generic canada

buy cialis ’

buy viagra karachi

buy viagra pills

viagra sales 2010

[url=http://vgcialistylbuyjl.com/#]how to order viagra online[/url]

want buy generic viagra

do buy viagra

safe buy viagra online yahoo

hard sell viagra salesman

[url=http://vgcialistylbuyjl.com/#]buy viagra without prescriptions[/url]

how does viagra 100mg work

do you need a prescription to buy viagra in canada

viagra for men sale

viagra online contrareembolso argentina

[url=http://vgcialistylbuyjl.com/#]order viagra without rx online[/url]

cipla generic sildenafil

price comparison viagra levitra

viagra sale galway

viagra 50mg tempo

[url=http://vgcialistylbuyjl.com/#]viagra price usa[/url]

donde puedo comprar viagra para mujer

viagra online american express

cheap herbal viagra pills

can get viagra walk in clinic

[url=http://vgcialistylbuyjl.com/#]buy viagra legit[/url]

viagra price in europe

lowest price on real viagra

can you buy viagra cvs

cheap cialis viagra online

[url=http://vgcialistylbuyjl.com/#]order herbal viagra[/url]

viagra sale walgreens

no fax payday loans direct lenders

fast payday loans

cash advance

payday loan online ’

viagra cheap generic

buy viagra

viagra levitra cialis for sale

[url=http://vgcialistylbuyjl.com/#]cheap legal viagra[/url]

can you get free samples viagra

what viagra pills do

viagra men sale

sildenafil tablets 50mg

[url=http://vgcialistylbuyjl.com/#]how to buy viagra online canada[/url]

viagra buy melbourne

50 mg viagra vs 100mg viagra

buy real viagra online

the best place to buy viagra

[url=http://vgcialistylbuyjl.com/#]buy real viagra uk[/url]

discount cialis and viagra

compare prices viagra

cheap viagra next day delivery

getting viagra in the uk

[url=http://vgcialistylbuyjl.com/#]buy cheap viagra mastercard[/url]

viagra buy in australia

debt relief programs

pay day loans

payday loans direct lenders

payday loans online direct lenders only ’

cheap viagra substitute

safe to order viagra online

viagra sales in the us

[url=http://mbviagraghtorderke.com/#]buy viagra online eu[/url]

can i buy viagra at chemist

viagra online consegna veloce

cheap viagra scams

sildenafil 50 mg uso

[url=http://mbviagraghtorderke.com/#]viagra buy over counter[/url]

the cheapest viagra online

fast payday loans

payday loans

fast loan

payday loans online ’

cuantos mg viagra debo tomar

viagra sale high street

buy viagra line nz

[url=http://mbviagraghtorderke.com/#]cheap viagra scams[/url]

viagra generico qual o melhor

cheap online viagra uk

real viagra sale online

women viagra pills india

[url=http://mbviagraghtorderke.com/#]can you buy viagra[/url]

can i buy viagra over the counter in the uk

viagra generico la

Viagra 50mg

onde comprar viagra online em portugal

[url=http://mbviagraghtorderke.com/#]Viagra Online[/url]

viagra and cialis together

sildenafil masticable de 50 mg

Viagra 100 mg

posso comprar viagra sem receita medica

[url=http://mbviagraghtorderke.com/#]Viagra 50 mg[/url]

pink pills for women viagra

sildenafil buy online uk

viagra australia

viagra price in kenya

[url=http://fastshipptoday.com/#]viagra prices[/url]

viagra 100 mg buy

can you get viagra nhs prescription

viagra from canada

buying viagra in mexico city

[url=http://fastshipptoday.com/#]cost of viagra[/url]

mixing viagra and cialis together

is it illegal to buy viagra online

viagra cost

viagra tabs 100mg

[url=http://fastshipptoday.com/#]viagra online[/url]

price comparison viagra levitra cialis

where can i buy viagra online canada

viagra for sale uk

when did viagra get fda approval

[url=http://fastshipptoday.com/#]viagra pills[/url]

viagra condom for sale

buy viagra united kingdom

viagra for men

buy viagra in canada online

[url=http://fastshipptoday.com/#]viagra australia[/url]

buy viagra manila forum

buy viagra cheap

viagra

buy viagra generic

generic viagra ’

sildenafil citrate tablets 150 mg

viagra for sale uk

can generic viagra sold

[url=http://fastshipptoday.com/#]where to buy viagra[/url]

how to buy viagra in india

how much is generic viagra

where to buy viagra

o generico do viagra funciona

[url=http://fastshipptoday.com/#]generic for viagra[/url]

how to get safe viagra online

generic levitra cialis viagra

viagra prices

can i buy viagra over the counter in malaysia

[url=http://fastshipptoday.com/#]viagra prices[/url]

get viagra prescription your doctor

buy cialis canada no prescription

cheap cialis

buy cialis online in uk

[url=http://waystogetts.com/#]cialis cost[/url]

cheap generic cialis australia

cialis super active cheap

cialis on line no pres

buy now viagra cialis

[url=http://waystogetts.com/#]cost of cialis[/url]

cialis buy us

generic cialis wholesale

generic cialis 2017

cialis professional buy

[url=http://fkdcialiskhp.com/#]buy cialis[/url]

buy cialis in vancouver

buy viagra and cialis online

buy cialis

generic cialis order

[url=http://fkdcialiskhp.com/#]cialis online[/url]

ac uk buy cialis

order viagra cialis canada

tadalafil generic

cheapest brand cialis online

[url=http://fkdcialiskhp.com/#]cialis generic[/url]

where can i order cialis online

where to buy generic cialis in canada

tadalafil generic

cheapest brand cialis

[url=http://fkdcialiskhp.com/#]generic cialis[/url]

buy cialis south africa

viagra online overnight

cheap viagra

buy viagra malaysia

[url=http://bgaviagrahms.com/#]cheap viagra[/url]

how to buy viagra in india

buy brand levitra

levitra online

buy generic levitra canada

[url=http://bmflevitramke.com/#]buy levitra online[/url]

mail order levitra

does viagra help weight lifting

http://aviagrant.com/ - buy Viagra

dangers of herbal viagra

[url=http://aviagrant.com]buy Viagra[/url]

viagra no me hace nada

generic Viagra online

viagra and prednisone

discount viagra online

viagra sale

viagra plus

herbal viagra ’

money slot [url=https://casinomegaslotos.com/]bovada[/url]

casino online casino slots

online casinos [url=https://casinomegaslotos.com/]slots casino[/url]

money online slots casino online

casino games [url=https://casinomegaslotos.com/]bonus slots[/url]

slot machines money slot

club casino [url=https://casinomegaslotos.com/]dreams casino[/url]

canada online casinos online roulette

slots real money [url=https://casinomegaslotos.com/]casinos online[/url]

game slot money slots

cheap cialis brand

buy cialis

cheap daily cialis

[url=http://bhscialisdjy.com/#]buy cialis[/url]

cheap cialis viagra online

generic cialis for sale

cialis online

canadian pharmacy buy cialis professional

[url=http://bhscialisdjy.com/#]cheap cialis[/url]

where can i buy cialis in london

slots lv

[url=https://hotlistcasinogames.com/]best slot games[/url]

bovada

best canada slot sites

[url=https://hotlistcasinogames.com/]slots[/url]

online casino games

slot sites

payday loans in minutes

[url=http://paydayloanstexasx.com/]fast cash[/url]

personal loan deals

payday cash advance loan

cialis sale

cialis cost

best place buy generic cialis online

[url=http://bhscialisdjy.com/#]cheap cialis[/url]

non generic cialis sale

888 casino

[url=https://casinomegaslotos.com/]slot sites[/url]

dreams casino

canada online casinos

[url=https://hotlistcasinogames.com/]money online slots[/url]

euro palace

mobile casino

celebrex online

[url=http://hqcelebrex2017.com/]celebrex[/url]

celebrex online

finasteride

[url=http://hqfinasteride2017.com/]propecia[/url]

finasteride 1mg

finasteride

celebrex

[url=http://hqcelebrex2017.com/]celebrex prices[/url]

celebrex prices

finasteride 1mg

[url=http://hqfinasteride2017.com/]finasteride 1mg[/url]

propecia

finasteride 1mg

when will viagra come off patent

http://viagranit.com/ - generic Viagra

efek samping menggunakan viagra

[url=http://viagranit.com]buy Viagra online[/url]

what is better levitra cialis or viagra

buy Viagra online

what is the use for viagra

dose cialis pharmacy

[url=http://tadalafil777.com/]order cialis 'tadalafil' online[/url]

buy tadalafil dosage

free cialis 'tadalafil' samples

cialis pills cheap

buy cialis

can cialis pills split

[url=http://gmwcialisfnw.com/#]cialis pills[/url]

cialis uk sale

buy cialis kl

cheap cialis

cheap brand name cialis

[url=http://gmwcialisfnw.com/#]cheap cialis[/url]

cialis soft tabs 20mg pills

cheapest way to get cialis

cialis pills

cialis and viagra for sale

[url=http://gmwcialisfnw.com/#]buy cialis[/url]

cheap cialis overnight

cialis black 800mg pills

cheap cialis

want buy cialis uk

[url=http://gmwcialisfnw.com/#]cialis pills[/url]

how to use cialis pills

cheap cialis online

cialis.com

cialis low dose

cialis prescription ’

order cialis online prescription

generic cialis

buy cialis online from uk

[url=http://tbnacialiskj.com/#]cialis generic[/url]

can you buy cialis online in australia

generic cialis price

cialis for women

order cialis without prescription

cialis soft tabs ’

viagra en linea ch

[url=http://viagrahsk.com/]viagra online[/url]

buy viagra

best price on viagra online

car insurance companies in houston

list of auto insurance companies

best car insurance massachusetts

[url=http://www.bestcarinsurancecompaniesquotes.com/]best priced car insurance[/url]

auto insurance companies in phoenix az

existe o generico do viagra

buy generic viagra

sildenafil effervescent tablets use

[url=http://ehuviagramek.com/#]viagra generic[/url]

where can i purchase viagra online

buy levitra cheap online

levitra prices

buy levitra in germany

[url=http://qmflevitrathd.com/#]vardenafil 20mg[/url]

best website buy levitra

buy levitra generic

levitra coupon

levitra buy uk

[url=http://qmflevitrathd.com/#]levitra 20 mg[/url]

buy levitra with prescription

cheap generic viagras

[url=http://viagragenericvas.com/]viagra online[/url]

buy viagra online

pack levitra viagra cialis

autocad takeoff software

autocad 2015

autocad 2014 key

[url=http://autocadgou.com/#]autocad 2015[/url]

where to buy autocad 2014

autocad serial key 2017

download autocad 2017

autocad software installation

[url=http://autocadgou.com/#]acad[/url]

autocad software cheap

autocad windows 7 64 bit download

autodesk autocad

cheap autocad software for sale

[url=http://autocadgou.com/#]autodesk autocad[/url]

download autocad 2011 64bit

autocad p&id 2013 product key

autocad

buy autocad 2011 cheap

[url=http://autocadgou.com/#]autodesk autocad[/url]

autocad hatch pattern download

autocad electrical software download

autocad 2018

cd key autocad 2011

[url=http://autocadgou.com/#]autocad[/url]

autocad release 12 download

autocad reader download

autocad 2014 free download

autocad chair download

[url=http://autocadgou.com/#]autocad 2018 download[/url]

upgrade to autocad 2017

autocad software commands

autocad online

autocad drawing management software

[url=http://autocadgou.com/#]autocad gratis[/url]

autocad 2011 price list

autocad 4 download

autocad 2014

descargar bloques en 3d autocad gratis

[url=http://autocadgou.com/#]autocad 2016[/url]

autocad civil 3d price

autocad soft

autocad viewer

autocad version numbers

[url=http://autocadgou.com/#]autocad gratuit[/url]

autocad mac student

serial autocad 2000

autocad 2015

autocad inventor 2011 student version

[url=http://autocadgou.com/#]free autocad[/url]

autocad activation

purchase autocad lt 2017

autocad 2017

buy autocad civil 3d 2014

[url=http://autocadgou.com/#]autocad download[/url]

product key autocad 2017 32 bit

autocad electrical 2013 download

autocad 2017

download autocad files dwg

[url=http://autocadgou.com/#]autocad 2015[/url]

autocad 2017 lt serial number

nhs cost of viagra

[url=http://viagralkp.com/]cheap viagra[/url]

cheap viagra

vente libre viagra portugal

autocad 2011 autodesk student

autocad download

integrated software solution autocad

[url=http://autocadbmsa.com/#]download autocad[/url]

autocad revit student version

autocad 2017 service pack 2 download

autocad 2014

autocad cuix file download

[url=http://autocadbmsa.com/#]autocad[/url]

serial autocad 14

only here free samples viagra

[url=http://viagragenericvas.com/]buy viagra[/url]

viagra online

viagra cialis comparaison

autocad 7 download

autocad 2018

download autocad structural detailing 2013

[url=http://autocadbmsa.com/#]autocad 2017[/url]

autocad revit mep suite 2017 download

dibujos de autocad para descargar

autocad 2014

autocad 2017 64 bit installer download

[url=http://autocadbmsa.com/#]autocad lt[/url]

autocad architecture 2013 serial number and product key

autocad ecotect student

autocad 2016

descargar bloques 3d autocad

[url=http://autocadbmsa.com/#]auto cad[/url]

serial number autocad lt 2011

xl viagra online

viagra coupons

cheap viagra to buy online

[url=http://itfviagrakmn.com/#]viagra for sale uk[/url]

generic viagra 100mg sildenafil

viagra buy australia

best price for viagra

how hard is it to get viagra

[url=http://itfviagrakmn.com/#]viagra coupons[/url]

long does pill viagra last

sleeping pills viagra

viagra prices

buy viagra au

[url=http://itfviagrakmn.com/#]viagra tablets[/url]

buy viagra in tesco

viagra levitra cialis price comparison

viagra coupons

viagra sale vegas

[url=http://itfviagrakmn.com/#]viagra for men[/url]

book hard sell the evolution of a viagra salesman

compare price generic viagra

[url=http://viagraonline100mgs.com/]buy generic viagra[/url]

cheap viagra

golden viagra wholesale

banana viagra

[url=http://viagraonlinefas.com/]buy viagra[/url]

cheap viagra

viagra comparatif

cheap cialis canada

cialis tablets

buy cheap cialis profile

[url=http://fmacialisuhy.com/#]cialis tablets[/url]

cialis pills amazon

cheapest 20 mg cialis

cialis coupons

liquid cialis for sale

[url=http://fmacialisuhy.com/#]cialis cost[/url]

cheap soft cialis

visit web site low cost cialis

[url=http://cialisorderasj.com/]cialis cheap[/url]

buy cialis

cheap cialis 20mg pakistan

cheap viagra adelaide

online pharmacy viagra

can take 2 50 mg viagra

[url=http://fvbviagrahnas.com/#]viagra online[/url]

best sites generic viagra

risk of generic viagra

[url=http://viagraonlinelka.com/]online viagra[/url]

viagra online

viagra in spain where to buy

sildenafil 25 mg venezuela

buy viagra

viagra spain buy

[url=http://fvbviagrahnas.com/#]viagra online[/url]

cheap place to buy viagra

viagra super online

viagra online

buy viagra over counter usa

[url=http://fvbviagrahnas.com/#]buy viagra online[/url]

how can i get viagra in london

how to buy cialis over the counter

cialis without a prescription

buy cialis online yahoo

[url=http://vnacialisfbvn.com/#]cialis without prescription[/url]

how to get cheap cialis

order cialis online no prescription canada

cialis without doctor

cialis pills for cheap

[url=http://vnacialisfbvn.com/#]cialis without prescription[/url]

what does cialis pills look like

buy cialis for cheap from us pharmacy

cialis without a doctor

buy cialis legally canada

[url=http://vnacialisfbvn.com/#]cialis without doctor[/url]

purchase cheap cialis soft tabs

we like it canada cialis

[url=http://cialisbuyhaq.com/]buy cialis online[/url]

generic cialis

cialis 4 sale au

buy cialis online no rx

cialis without a doctor's prescription

cialis pills

[url=http://vnacialisfbvn.com/#]cialis without doctor[/url]

buy cialis edmonton

online cash casino games

[url=http://agtteam.com/?option=com_k2&view=itemlist&task=user&id=166028]slots 88 fortune[/url]

gambling problem canada

new slot

como comprar viagra sem receita medica

viagra without a prescription

viagra for sale in canada

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor visit[/url]

usa viagra cheap info

generic viagra price canada

viagra without prescription

how viagra pills looks like

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

for meget viagra

casino utrecht

[url=http://www.eat-well-live-well.co.uk/?option=com_k2&view=itemlist&task=user&id=32953]free casino slots no download no registration[/url]

online casino malta

cash casino jobs calgary

online roulette oefenen

[url=http://dango.kz/?option=com_k2&view=itemlist&task=user&id=33339:robertdicks72372]casino guildford[/url]

canberra casino

casino king part 2

generic viagra 100mg viagra online no prescription

generic viagras when

viagra price [url=http://sildenafil-us.com/]viagra overdose[/url]

click here cialis from india

[url=http://cialisonlinehaq.com/]buy cialis online[/url]

buy cialis online

cialis internet purchase

cialis where to buy - malaysia

cheap cialis online

cialis pills for cheap

[url=http://cialisdmngj.com/#]cheap cialis online[/url]

what color are cialis pills

can you cut cialis pills in half

cialis prices

where is the cheapest place to buy cialis

[url=http://cialisdmngj.com/#]cialis cost[/url]

buy cialis canada yahoo answers

cialis for sale in usa

cialis cheap

buy cialis levitra and viagra

[url=http://cialisdmngj.com/#]cialis price[/url]

real cialis pills

viagra rss feed

[url=http://viagralkq.com/]viagra online[/url]

buy viagra online

try it purchase of viagra

ac uk buy cialis

cheap cialis online

order cialis uk

[url=http://cialisdmngj.com/#]cheap cialis online[/url]

cialis cheap no prescription

buy viagra sample

viagra without a doctor prescription

viagra women sale australia

[url=http://viagrahukic.com/#]viagra without a doctor[/url]

generic viagra coupon codes

payday loans california

[url=https://loanstrast.com/]advance cash services[/url]

online bad credit loans

need a personal loan

viagra 25 mg sildenafil citrate

viagra without a doctor

buy cheap viagra australia

[url=http://viagrahukic.com/#]viagra without a doctor prescription[/url]

viagra pills meaning

viagra online deutschland

viagra without doctor

viagra pfizer buy

[url=http://viagrahukic.com/#]viagra without a doctor's prescription[/url]

female viagra pill forum

buy real viagra

viagra without a doctor's prescription

viagra super force 100mg 100mg pills

[url=http://viagrahukic.com/#]viagra without a doctor prescription[/url]

get best results using viagra

buy viagra in dominican republic

viagra without a prescription

viagra tablets price

[url=http://viagrahukic.com/#]viagra without a doctor[/url]

can buy viagra spain

buy cialis professional 20 mg

cialis prices

cheapest cialis no prescription

[url=http://cialismbvi.com/#]online cialis[/url]

buy discount cialis

loans for people with bad credit

[url=https://loanstrast.com/]secured loan bad credit[/url]

how to apply for a loan

financial loans

where to order cialis online

cialis prices

acheter cialis discount

[url=http://cialismbvi.com/#]buy cialis[/url]

buy cheap cialis in canada

how to order cialis online safely

buy cialis

cialis forum where to buy

[url=http://cialismbvi.com/#]buy cialis online[/url]

cheaper viagra cialis levitra

payday loans las vegas nevada

[url=https://loanstrast.com/]online loan application[/url]

payday loans el paso tx

need money asap

viagra pfizer 100mg price

cost of viagra

where can i safely buy viagra

[url=http://viagramndet.com/#]viagra coupons[/url]

viagra online legal

venden viagra generico farmacias similares

viagra coupons

viagra women sale

[url=http://viagramndet.com/#]viagra coupons[/url]

where can i buy viagra on the high street

long term loan

[url=https://loanstrast.com/]bad credit unsecured loans[/url]

fast loans

cash advances online

does viagra pill cost

cost of viagra

price generic viagra

[url=http://viagramndet.com/#]cost of viagra[/url]

can break viagra pill half

buy viagra online mexico

viagra prices

weili pills herbal viagra

[url=http://viagramndet.com/#]viagra cost[/url]

generic viagra usa

expiration on viagra pills

viagra cost

how can i buy viagra in india

[url=http://viagramndet.com/#]viagra price[/url]

viagra online no prescriptions

online payday loans texas

[url=https://loanstrast.com/]bad credit cash loans[/url]

long term loans for bad credit

moneylenders

can viagra help women to get pregnant

best price for viagra

purchase generic viagra canada

[url=http://viagramhbfe.com/#]viagra coupons 75 off[/url]

where can i buy viagra in stores

when generic viagra be available

viagra prices

2010 viagra sales

[url=http://viagramhbfe.com/#]viagra prices[/url]

when is generic viagra available in the united states

generic viagra offers

viagra prices

how to take viagra 50mg

[url=http://viagramhbfe.com/#]viagra coupons 75 off[/url]

best place viagra online

viagra cheapest

viagra prices

viagra generico venda brasil

[url=http://viagramhbfe.com/#]viagra prices[/url]

anyone bought generic viagra

cialis cheap overnight

cialis coupons

buy black cialis online

[url=http://cialisopghe.com/#]5 mg cialis coupon printable[/url]

cialis pills men

unsecured loans

[url=https://loanstrast.com/]money lender[/url]

cash advances online

loans for bad credit no guarantor

order cialis at online pharmacy

cialis coupons printable

cialis buy no prescription

[url=http://cialisopghe.com/#]cialis coupons 2017[/url]

buy cialis online overnight

allstate insurance

health insurance cost

alfainsurance com

[url=http://autoinsurbest.com/]auto insurance discounts[/url]

personal auto insurance

cialis sale usa

cialis coupon 20 mg

mail order cialis generic

[url=http://cialisopghe.com/#]cialis coupons[/url]

buy cialis no prescription uk

much cialis pills

coupon for cialis

can you buy cialis in hong kong

[url=http://cialisopghe.com/#]cialis coupons printable[/url]

cialis sale ireland

do you need a prescription to buy levitra

levitra bayer 20mg meilleur prix

buying levitra online

[url=http://levitraklnbi.com/#]levitra online[/url]

buy levitra professional online

discount on levitra

9 levitra at walmart

best place to buy levitra

[url=http://levitraklnbi.com/#]levitra bayer 20mg meilleur prix[/url]

cheap levitra pills

buy levitra 20mg

generic levitra

levitra super active cheap us

[url=http://levitraklnbi.com/#]levitra 20 mg[/url]

buy cheap levitra no prescription

cheapest levitra online

levitra 20 mg

generic levitra cheapest prices

[url=http://levitraklnbi.com/#]levitra bayer 20mg meilleur prix[/url]

buy generic levitra no prescription

where can i buy levitra

generic levitra

is buying levitra online safe

levitra 20mg

order generic levitra online

cheap cialis here

cialis without a prescription

generic cialis discount

cialis without a prescription

cialis buy online generic

can you buy cialis over counter usa

cialis without doctor

cialis cheap prices

[url=http://cialisfbvne.com/#]cialis without prescription[/url]

cialis buy in australia

buy cialis professional 20 mg

cialis without a prescription

pills like cialis

cialis without a doctor prescription

cheapest cialis in uk

cheapest 20 mg cialis

cialis without a prescription

cheap cialis overnight delivery

[url=http://cialisfbvne.com/#]cialis without a doctor's prescription[/url]

cialis compare discount price

cialis free sample

where can i buy cialis

cialis vs cialis professional

[url=http://canadapharmacy.us.com/]affordable cialis[/url]

get cialis online

cialis wholesale prices

cialis without a doctor's prescription

buy cheap cialis link online

[url=http://cialisfbvne.com/#]cialis without a doctor prescription[/url]

buy cialis uk cheap

buy cialis with no prescription

cialis without a prescription

cialis to buy us

cialis without a doctor

buy cialis viagra levitra

cialis tadalafil buy online

cialis without a doctor's prescription

discount cialis no prescription

[url=http://cialisfbvne.com/#]cialis without a doctor[/url]

cheap brand name cialis

cheap cialis black

cialis without a doctor's prescription

buy cheap cialis uk

cialis without prescription

buying cheapest generic cialis soft tab

payday loans

[url=https://loanstrast.com/]payday loans[/url]

payday loans online

loans online

get viagra cheap

viagra without prescription

wie lange wirkt viagra 25mg

viagra without a prescription

cheap viagra online canada

viagra online coupons

viagra without a doctor’s prescription

viagra sale point in pakistan

[url=http://viagramnkjm.com/#]viagra without a doctor’s prescription[/url]

viagra pricing 100mg

quarter pill of viagra

viagra without a doctor

para sirve medicamento sildenafil 50 mg

[url=http://viagramnkjm.com/#]viagra without doctor[/url]

buy viagra legally uk

cheap viagra online canadian

viagra without a doctor prescription

can buy viagra uk

[url=http://viagramnkjm.com/#]viagra without doctor[/url]

viagra sale in kenya

prijs viagra 50 mg

viagra without a doctor’s prescription

viagra buy uk online

[url=http://viagramnkjm.com/#]viagra without a doctor's prescription[/url]

pramil sildenafil 50 mg

viagra generico espana

viagra without a doctor

how i can buy viagra

viagra without a doctor

safe to buy viagra online

casino on line s

casino

live dealer online casino

online casino

casino bellini

online casino norway

casino online

jackpot dice game gambling site

[url=http://online-casino.party/#]casino[/url]

on line casino for macintosh

online for illinois casino

casino

casino card games download

casino

best casino games downloadable

real money internet slots

casino

download casino games for android

[url=http://online-casino.party/#]online casino[/url]

online casino download

online casino vegas style casino games

casino real money

best online casino on line game

casino online

watch live casino roulette

how to viagra works

http://viagrabs.com/ - viagra online

how long does half a pill of viagra last

[url=http://viagrabs.com]viagra online[/url]

viagra best way to use it

buy viagra online

viagra how it was discovered

online casinos without credit card rejection

casino

bellagio casino

[url=http://online-casino.party/#]online casinos[/url]

live casino online no deposit bonus

online roulette canada real money

online casinos

best uk casino

online casino

online gambling minnesota

new us player casinos

casino

iphone online casino usa

online casino

australian online mobile casino

online payday loans

[url=https://smajloans.com/]payday advance[/url]

payday advance

online loans

[url=https://loanstrast.com/]payday loans online[/url]

payday advance

payday loans no credit check

[url=https://loansfast.us.com/]payday loans no credit check[/url]

pay day loans

payday loans no credit check

how can i get a sample of viagra

viagra for sale

viagra sale high street

[url=http://hqviagrajdr.com/]viagra for sale[/url]

viagra buy bangkok

casino card games list

online casino

reputable online casinos usa

[url=http://online-casino.party/#]online casino[/url]

online gambling allowed us

best online casino for blackjack

online casino

blackjack online paypal

[url=http://online-casino.party/#]casino online[/url]

usa based online casinos

top on line casinos

online casino

mobile casino usa welcome

[url=http://online-casino.party/#]casino online[/url]

online casino hd

top10casinobonuses

casino

us online gambling websites

[url=http://online-casino.party/#]online casino[/url]

online casino quebec

payday loans no credit check

[url=https://smajloans.com/]payday loan online[/url]

cash loans

cash advance loans

[url=https://loanstrast.com/]online payday loans[/url]

pay day loan

pay day loan

[url=https://loansfast.us.com/]pay day loan[/url]

online payday loans

payday loan online

online casino best rated

casino online

gambling bonuses

casino

black jack on line

online loans

[url=https://smajloans.com/]pay day loan[/url]

payday advance

cash advance loans

[url=https://loanstrast.com/]payday loans no credit check[/url]

payday loans

payday loans

[url=https://loansfast.us.com/]online loans[/url]

payday loans

payday loans

viagra gel online

viagra without a prescription

viagra purchase online

[url=http://viagrajnmeo.com/#]viagra without a doctor’s prescription[/url]

where to buy viagra in vancouver

cash advance

[url=https://smajloans.com/]online loans[/url]

payday loan online

pay day loans

[url=https://loanstrast.com/]cash loans[/url]

cash advance loans

online payday loans

[url=https://loansfast.us.com/]payday advance[/url]

pay day loans

cash loans

generico do viagra sandoz

viagra without a doctor

sildenafil tabletten 100mg

viagra without a doctor

prescription price of viagra

best rated online pharmacy viagra

viagra without prescription

cheapest viagra on the net

[url=http://viagrajnmeo.com/#]viagra without a doctor's prescription[/url]

viagra pills price

cheap viagra oral jelly pp

viagra without a doctor

viagra generic available in united states

[url=http://viagrajnmeo.com/#]viagra without a doctor prescription[/url]

will 50mg viagra work

cash advance loans

[url=https://smajloans.com/]payday loans no credit check[/url]

payday loans

pay day loan

[url=https://loanstrast.com/]pay day loan[/url]

payday advance

payday loan online

[url=https://loansfast.us.com/]cash loans[/url]

cash advance loans

payday loans no credit check

viagra non prescription safe sites canadian pharmacy sky pharmacy canada best price viagra 100mg costco buy viagra fast delivery

como usar cialis de 5mg

erection pills

where can i buy viagra

[url=http://pillshnembn.com/#]erectile dysfunction medications[/url]

trusted site to buy cialis

precio cialis 5 mg. diario

ed drugs

200mg viagra safe take

[url=http://pillshnembn.com/#]ed drugs[/url]

order tadalafil online

erofast sildenafil 50 mg como comprar

erectile dysfunction pills

viagra will go generic

[url=http://pillshnembn.com/#]erectile dysfunction medications[/url]

viagra prices in the united states

payday loans online

[url=https://smajloans.com/]online loans[/url]

pay day loan

pay day loan

[url=https://loanstrast.com/]payday loans online[/url]

payday advance

payday loans

[url=https://loansfast.us.com/]pay day loan[/url]

payday loans no credit check

payday loans

buy cialis lilly

cialis without a doctor prescription

cialis discount card

[url=http://cialisviymw.com/#]cialis rezeptfrei[/url]

buy cialis no prescription overnight

24 month loans

http://paydayloansimd.com/ - payday loans online

secured personal loans

payday loans online

how to apply for loans

[url=http://paydayloansimd.com]payday loans online[/url]

payday loans aurora co

cialis soft tablets

cialis without doctor

cialis pills in canada

cialis without a doctor prescription

can cialis pills be split

generic viagra real or not

buy viagra online

can viagra go generic

buy viagra

cheap indian viagra

viagra for women for sale australia

buy viagra

viagra sale canada

[url=http://viagrakbg.com/#]viagra prices[/url]

viagra super force 100mg

viagra pfizer 100mg dawkowanie

viagra online

150 mg de viagra

[url=http://viagrakbg.com/#]buy viagra online[/url]

buy viagra super active online

sildenafil citrate 100 mg dosage

buy viagra online

venden viagra generico en farmacias similares

[url=http://viagrakbg.com/#]buy viagra[/url]

buying real viagra online

viagra pill cut in half

buy viagra

many pills viagra

[url=http://viagrakbg.com/#]buy viagra online[/url]

sildenafil online from india

online casino

[url=http://real777money.com/]real money casino[/url]

slot games

best us casinos online

does viagra become generic

buy viagra

online viagra satisi

[url=http://viagrakbg.com/#]buy viagra online[/url]

get a prescription for viagra

should i take generic viagra

buy viagra online

discount pills viagra

[url=http://viagrakbg.com/#]cheap viagra[/url]

get free trial viagra

online pharmacy cheap viagra

buy viagra

where can i buy viagra in durban

[url=http://viagrakbg.com/#]viagra pills[/url]

viagra price philippines

best us casinos online

[url=http://real777money.com/]free casino games[/url]

free online casino games

best us casinos online

how can i buy viagra over the counter

best price for viagra

nomes dos genericos do viagra

[url=http://viagrangk.com/#]best price for viagra[/url]

where buy viagra uk

best us casinos online

[url=http://real777money.com/]real money casino online usa[/url]

casino game

casino online

canadian living recipes

canadian pharmacies online

online prescriptions

[url=http://canadaunmfgb.com/#]canadian pharmacies shipping to usa[/url]

Trusted Online Pharmacies

online pharmacy

best canadian mail order pharmacies

top rated canadian pharmacies online

[url=http://canadaunmfgb.com/#]canadian pharmacies[/url]

canada pharmacy online

legitimate place to buy viagra

viagra ohne rezept aus deutschland

generico al viagra

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

how do you get viagra without a doctor

100 mg viagra safe

viagra without a doctor prescription

buy viagra next day

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

how to get best results from viagra

payday advance

[url=https://smajloans.com/]payday loans online[/url]

pay day loans

online loans

price list of viagra

viagra without prescription

viagra dosage 200 mg

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

can you take cialis and viagra together

viagra no prescription

keep getting viagra emails

[url=http://bfviagrajlu.com/#]viagra ohne rezept aus deutschland[/url]

can you get viagra boots

commander cialis ligne

[url=http://cialisuyb.com/]buy cialis[/url]

buy cialisviagra multiple intercourse

[url=http://cheapvagratlonline.com/]buy viagra online[/url]

online viagracost of cialis at pharmacy

[url=http://cialisjqp.com/]cheap cialis[/url]

buy cialis

get viagra for free

viagra without prescription

magnus masticable sildenafil 100mg

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

generico viagra doctor simi

viagra without a doctor prescription

foto della pillola viagra

[url=http://bfviagrajlu.com/#]viagra no prescription[/url]

sales viagra statistics

cash loans

[url=https://smajloans.com/]online payday loans[/url]

pay day loan

payday loan online

viagra sale new zealand

viagra without a doctor prescription

compare viagra prices uk

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

generic viagra canadian pharmacy online

viagra ohne rezept aus deutschland

buy generic viagra 50mg online

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

what is generic viagra soft

prescription drugs for sale online

cialis in the usa

cialis.com coupon buy generic ed pills online

[url=http://buynrents.com/members/trialwrist2/activity/139079/]buy prescription drugs without doctor[/url]

sildenafil 50 mg efecto en mujeres

viagra without a doctor prescription

buy viagra in cvs

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

get viagra canada prescription

viagra without a doctor prescription

will generic viagra become

[url=http://bfviagrajlu.com/#]viagra no script[/url]

sildenafil orion 50 mg hinta

suche viagra pill

[url=http://cheapvagratlonline.com/]buy viagra[/url]

buy viagra onlinecialis vendita online italia

[url=http://cialisjqp.com/]cialis[/url]

cheap cialiscialis 20mg price in pakistan

[url=http://cialisnji.com/]cialis online[/url]

generic cialis online

payday loans no credit check

[url=https://smajloans.com/]payday loans[/url]

payday loans

payday loans online

vegetal viagra

viagra without a doctor prescription

what is the cost of viagra per pill

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

sildenafil citrate 100mg woman

viagra ohne rezept aus deutschland

viagra online bestellen strafbar

[url=http://bfviagrajlu.com/#]viagra without prescription[/url]

order viagra generic

viagra for sale online in canada

viagra without prescription

illegal buy viagra street

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

viagra mg dosage

viagra without a doctor prescription

cialis 20mg ou viagra

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

is it legal to order generic viagra online

take viagra and cialis

http://viagrapid.com/ - buy viagra

can you become resistant to viagra

[url=http://viagrapid.com]viagra for sale online[/url]

how to prepare viagra naturally

buy generic viagra

effect of grapefruit on viagra

payday loans

[url=https://smajloans.com/]payday loans[/url]

payday loans

payday loans no credit check

viagra 500mg price

viagra without a doctor prescription

hard sell the evolution of a viagra salesman spoiler

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

does generic viagra work yahoo

viagra no prescription

viagra online in the uk

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

generic viagra in america

viagra for sale online uk

viagra without prescription

100mg sildenafil citrate and 60 mg dapoxetine

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

generic viagra me uk silagra tablets

viagra no script

can i buy viagra online uk

[url=http://bfviagrajlu.com/#]viagra no script[/url]

comprar viagra segura online

[url=http://lace-wigs.net/]Wigs[/url]

[url=http://lace-wigs.net/]Lace Front Wigs[/url]

[url=http://wigshumanhair.us.com/]Human Hair Wigs[/url]

[url=http://wigshumanhair.us.com/]Wigs For Women[/url]

[url=http://wigforwomen.com/]Wigs For Women[/url]

[url=http://wigforwomen.com/]Wig[/url]

[url=http://wigshumanhair.org/]Wigs[/url]

[url=http://wigshumanhair.org/]Wigs For Black Women[/url]

[url=http://wigsforblackwomenbuy.com/]Wigs For Women[/url]

[url=http://wigsforblackwomenbuy.com/]Wigs For Black Women[/url]

[url=http://humanhair-wigs.org/]Wigs[/url]

[url=http://humanhair-wigs.org/]Human Hair Wigs[/url]

[url=http://lace-wigs.org/]Wigs[/url]

[url=http://lace-wigs.org/]Lace Front Wigs[/url]

[url=http://fulllacefront-wigs.com/]Full Lace Front Wigs[/url]

[url=http://fulllacefront-wigs.com/]Lace Wigs[/url]

[url=http://lacefront-wigs.com/]Lace Front Wigs[/url]

[url=http://lacefront-wigs.com/]Lace Wigs[/url]

[url=http://humanhair-wigsus.com/]Human Hair Wigs[/url]

[url=http://humanhair-wigsus.com/]Wigs[/url]

[url=http://humanshairwigs.com/]Human Hair Wigs[/url]

[url=http://humanshairwigs.com/]Wigs For Women[/url]

[url=http://humanrhairwigs.com/]Human Hair Wigs[/url]

[url=http://humanrhairwigs.com/]Wigs[/url]

[url=https://wigsrforwomen.com/]Wigs For Women[/url]

[url=https://wigsrforwomen.com/]Wigs[/url]

payday loans online

[url=https://smajloans.com/]payday loans online[/url]

payday loans

payday loans online

viagra in usa cheap

[url=http://viagrafaaq.com/]generic viagra online[/url]

buy viagra onlineviagra vending machines uk

[url=http://viagrapurchsaseua.com/]online viagra[/url]

buy generic viagrareview of generic cialis

[url=http://cialisuyb.com/]generic cialis[/url]

cialis cheap

payday loans online

[url=https://smajloans.com/]payday loans[/url]

payday loans

payday loans no credit check

buying cheap viagra online

viagra without a doctor prescription

pill like viagra women

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

using viagra to get over performance anxiety

viagra no prescription

opinions on generic viagra

[url=http://bfviagrajlu.com/#]viagra no script[/url]

cheap viagra wholesale

viagra 4x50mg

viagra without prescription

150 mg sildenafil citrate

[url=http://thjsildenafiljkvc.com/#]viagra without prescription[/url]

do need prescription buy viagra us

viagra without prescription

swiss pill cutter viagra

[url=http://bfviagrajlu.com/#]viagra no script[/url]

viagra cialis generici

can you buy viagra legally

viagra without prescription

viagra going generic in 2012

[url=http://thjsildenafiljkvc.com/#]viagra without a doctor prescription[/url]

se puede comprar viagra en farmacia sin receta

viagra without prescription

cheap viagra overnight delivery

[url=http://bfviagrajlu.com/#]viagra without a doctor prescription[/url]

cheapest viagra cialis levitra

what do i tell the doctor to get viagra

viagra cost

can i buy viagra in soho

[url=http://sildenafilmkfbv.com/#]cheap viagra[/url]

viagra online clinic

online casino games

[url=http://casinoline17.com/]casino games[/url]

online casino

casino online usa

payday loans no credit check

[url=http://paydaynock.com/]payday loans no credit check[/url]

payday loans no credit check

payday loans online no credit check

payday loans online no credit check

[url=http://paydaynock.com/]payday loans no credit check[/url]

payday loans no credit

payday loans online no credit check

payday loans online no credit check

[url=http://paydaynock.com/]payday loans online no credit check[/url]

payday loans no credit check

payday loans online no credit check

best website buy levitra

levitra prices

buy levitra pills online

[url=http://levitradbws.com/#]levitra prices[/url]

cheap cialis levitra

levitra 20 mg

levitra sales

[url=http://vardenafilghns.com/#]vardenafil 20mg[/url]

generic levitra sale

casino online

[url=http://casinoline17.com/]casino games[/url]

casino games

online casino

cheap cialis and levitra

vardenafil

levitra cheap

[url=http://levitradbws.com/#]vardenafil[/url]

buy 40 mg levitra

levitra 20 mg

levitra buy no prescription

[url=http://vardenafilghns.com/#]levitra 20 mg[/url]

cheap levitra no prescription

payday loans no credit

[url=http://paydaynock.com/]payday loans online no credit check[/url]

payday loans online no credit check

payday loans no credit

buy generic viagra online from canada

buy viagra online

best site buy viagra forum

[url=http://viagratutrjdsd.com/#]viagra online pharmacy[/url]

get viagra in chicago

viagra online pharmacy

diferencia viagra generico viagra normal

[url=http://viagraeyefbdj.com/#]cheap viagra online[/url]

viagra target market

what does the viagra pill do

buy viagra online

buy viagra in united states

[url=http://viagratutrjdsd.com/#]buy viagra online[/url]

viagra online mastercard

cheap viagra online

cheap generic viagra uk online

[url=http://viagraeyefbdj.com/#]viagra online[/url]

can u buy viagra over counter

tipelmlc http://mphasset.com buy generic viagra generic cialis online znnj [url=http://rabbitinahat.com]generic cialis[/url]

lbuvqvss http://onevoicemethod.com buy viagra soft generic viagra tzkl [url=http://rabbitinahat.com]buy cialis online us[/url]

online casino

[url=http://bom777casino.com/]real money casino[/url]

casino games

casino games

nzlffeql http://skyrank.com buying cialis in australia cialis online buy aixo [url=http://rebeccaharrell.com]cialis coupon[/url]

phdezvxt http://protocog.com buy viagra buy generic viagra canada dtyd [url=http://rebeccaharrell.com]buy cialis generic online[/url]

online casino

[url=http://bom777casino.com/]online casino[/url]

real money casino

real money casino

iykdgmud http://psychologytweets.com buy cialis online in australia buy cialis online in australia zxwl [url=http://psychologytweets.com/]buy cialis online in australia[/url]

uemcfaiy http://skyrank.com cialis and viagra together cialis and viagra together wtjo [url=http://skyrank.com]cialis and viagra together[/url]

free casino games

[url=http://bom777casino.com/]online casino[/url]

casino games

real money casino

yrdlgxyj http://matehusta.com viagra online canada viagra online canada xvbj [url=http://matehusta.com]viagra online canada[/url]

real money casino

[url=http://bom777casino.com/]casino online[/url]

online casino

casino games

top online casino paypal

casino online

sky king online casino

[url=http://online-casino.party/#]online casinos[/url]

casino bonus online

kafplylr http://lizlarssen.com viagra capsule viagra capsule jziu [url=http://lizlarssen.com]viagra capsule[/url]

jtopnrbv http://motechautomotive.com cost of cialis walmart cost of cialis walmart nrdy [url=http://motechautomotive.com]cost of cialis walmart[/url]

free casino games

[url=http://bom777casino.com/]free casino games[/url]

casino games

casino games

muestra de cialis genrico

[url=http://cialisjqp.com/]cialis cheap[/url]

cheap cialiscialis 10mg 120 tabs

[url=http://cialisnji.com/]cialis cheap[/url]

generic cialisshort term loans cash

[url=http://soloadvance.com/] cash advance[/url]

payday express

nmeputxp http://psychologytweets.com buy cialis online usa buy cialis online usa tcri [url=http://psychologytweets.com/]buy cialis online usa[/url]

free casino games

[url=http://bom777casino.com/]casino online[/url]

free casino games

casino games

qkrlahzu http://missreplicawatches.com difference between viagra and cialis difference between viagra and cialis shri [url=http://missreplicawatches.com]difference between viagra and cialis[/url]

nswiiftu http://lizlarssen.com how long before sex should you take viagra how long before sex should you take viagra uocc [url=http://lizlarssen.com]how long before sex should you take viagra[/url]

rdnochpj http://missreplicawatches.com buying cialis in canada buying cialis in canada symi [url=http://missreplicawatches.com]buying cialis in canada[/url]

real money jackpots

online casino

real gambling on facebook

[url=http://online-casino.party/#]casino[/url]

play video poker online for money

azsoiovt http://investinokc.com generic viagra online generic viagra online llee [url=http://investinokc.com]generic viagra online[/url]

wftipuzt http://livecopys.com cheap viagra buy viagra online fhzo [url=http://matehusta.com]order viagra[/url]

cialis para venta en calgary

[url=http://cialisjqp.com/]cheap cialis[/url]

cheap cialiscialis 10mg erfahrung

[url=http://cialisnji.com/]buy cialis[/url]

cialis onlinecash loans in gaffney sc

[url=http://soloadvance.com/] pay day loans[/url]

loans for bad credit

casino slots

[url=http://casinobablogames.com/]free slots casino games[/url]

slotomania free slots

online casino real money

free casino slots

[url=http://casinobablogames.com/]slots for free[/url]

casino games slots

free casino slots

watermelon as a natural viagra buy generic viagra lower back pain cialis [url=http://psychologytweets.com]buy cialis 5mg[/url] buy generic cialis http://rabbitinahat.com

viagra pills look like buy viagra online daily cialis cost [url=http://psychologytweets.com]buy generic cialis[/url] buy cialis 20mg online http://skyrank.com

cialis tadalafil buy online buy cialis from canada drug interactions with viagra [url=http://kqcopy.com]viagra coupon[/url] buy viagra fedex http://mphasset.com

taking 2 5mg cialis buy cialis viagra 100 mg price [url=http://matehusta.com]viagra coupon[/url] cheap viagra online http://kqcopy.com

autocad 2017 64 bits download

autocad student

introduction to autocad 2017 pdf download

[url=http://autocadtymafq.com/#]autocad student[/url]

autocad projects for students

autodesk

autocad mac academic

[url=http://autocadbnaqk.com/#]autodesk[/url]

autocad for cheap

is 2.5 mg of cialis enough cialis buy australia cialis dosage vs viagra [url=http://lizlarssen.com]viagra coupon[/url] cialis buy cheap http://motechautomotive.com

when to take cialis before sex buy cialis pharmacy effects of viagra and alcohol [url=http://skyrank.com]buy cialis australia[/url] generic cialis online http://rebeccaharrell.com

cialis daily use discount

cialis prices

cialis color of pills

[url=http://cialisghkgfjm.com/#]cialis online[/url]

how to buy cialis in london

generic cialis

buying cialis in london

[url=http://cialistrihfy.com/#]generic cialis[/url]

cheap/discount cialis

compare uk viagra prices

viagra without script

walgreens viagra price

[url=http://viagrayirib.com/#]non-prescription viagra[/url]

viagra get over performance anxiety

viagra coupon

can you buy viagra in store

[url=http://viagrahkfy.com/#]viagra coupons[/url]

viagra legales online-rezept

odsefncu http://kqcopy.com generic viagra online generic viagra online nwbz [url=http://protocog.com]buy generic viagra[/url]

cialis online pharmacy canadian buy discount cialis price of generic viagra [url=http://janxie.com]cheap viagra[/url] generic viagra online http://janxie.com

orrpxuje http://livecopys.com cheap viagra cheap viagra quhy [url=http://mphasset.com]order viagra[/url]

tcnoycyo http://matehusta.com buy generic viagra buy generic viagra qpfo [url=http://psychologytweets.com]order cialis[/url]

casino arizona

[url=http://bablcasinogames.com/]slots for money online[/url]

download free casino slot games

online casinos real money

buy cialis tablets

online cialis

generic cialis buy

[url=http://cialisdgswryre.com/#]cialis online[/url]

cheap cialis overnight delivery

tadalafil generic

order brand cialis online

[url=http://cialisrutrhs.com/#]tadalafil generic[/url]

cialis wholesale uk

dzgffxsh http://janxie.com generic viagra online generic viagra online fqwy [url=http://mphasset.com]buy viagra[/url]

levitra buy cheap

levitra online

levitra by mail order

[url=http://levitranthdi.com/#]levitra[/url]

cheapest levitra/uk

vardenafil 20 mg

buy levitra nz

[url=http://vardenafildtudf.com/#]vardenafil[/url]

buy levitra dapoxetine

safe buy viagra over internet

viagra without doctor

can i get viagra at walmart

[url=http://viagrawyrfhdj.com/#]viagra without doctor[/url]

sildenafil in india online

cheap viagra

generic viagra online 50mg

[url=http://viagrartuudhf.com/#]buy viagra[/url]

is it illegal to buy viagra

rjkuswde http://mphasset.com buy viagra buy viagra shiy [url=http://istanbulexpressonline.com]order viagra[/url]

how to get cialis or viagra

viagra without doctor

buy viagra online - http //buyviagraonlinehere.com

[url=http://viagrawyrfhdj.com/#]viagra without prescription[/url]

where can i buy viagra over the counter uk

viagra prices

is the viagra online from canada safe

[url=http://viagrartuudhf.com/#]buy viagra[/url]

viagra blue pills

cheapest viagra buy cheap viagra

viagra without doctor

viagel oral gel sildenafil 100mg

[url=http://viagrayutkh.com/#]viagra prices[/url]

viagra online cheap canada

buy viagra

buy generic viagra online india

[url=http://viagratyrif.com/#]viagra prices[/url]

get free sample of viagra

vkdrwere http://lizlarssen.com viagra coupon viagra coupon bppz [url=http://janxie.com]buy generic viagra[/url]

free casino games and poker

[url=http://bablcasinogames.com/]harrah's casino locations by state[/url]

casino arizona

list of all harrah's casinos

how long does it take for cialis daily to work buy cialis online usa cialis and eye problems [url=http://skyrank.com]cialis buy online canada[/url] viagra online http://livecopys.com

online casino

[url=http://casinoveganonline.com/]online casino gambling[/url]

online casinos for us players

online casino no deposit bonus

cialis 5mg use

http://cialisle.com/ - how much is cialis at walmart

cialis fluid retention

[url=http://cialisle.com]cialis manufacturer[/url]

come posso comprare cialis

cialis without prescription

cialis klachten

play casino games online

[url=http://casinoveganonline.com/]biggest no deposit welcome bonus[/url]

free casino games and poker

casino games free

buy generic cialis online uk

cialis online

cialis for sale

[url=http://cialiskkg.com/#]cialis generico online[/url]

can you buy cialis uk

generic cialis at walmart

buy cheap cialis usa visa

[url=http://cialisdcfev.com/#]generic cialis tadalafil[/url]

order cialis online with prescription

viagra dosage for best results

[url=http://hqviagrauro.com/]cheap viagra pills[/url]

viagra to a girl

viagra cheap

viagra for sale in bangalore

Knight's tactic clearly, today is to be able to cling to garage, don't give him any possibility, and Kevin durant is always one-on-one with defense. But garage or under heavy defensive look for opportunities, such as face [url=http://www.stephencurryshoes.us]stephen curry shoes[/url] low, he mobilized, make use of the other fear his outside ability garage easily have scored two points.

The last 80 seconds from the first half, durant had missed shots from outside, this basket three players are usually knights, including Thompson, lebron, therefore, the Treasury rushed into the basket from the prolonged position, unexpectedly the offensive rebounds inside the knight encirclement! Then this individual points ball durant, exactly who finished scores!

And the 2nd half, knight to defensive strategy appears to be shaken, they don't have too much double again, help, interestingly, JR in 1 with 1 against Arsenal, and directly put the actual garage was pushed on the ground.

Sure enough, the particular knight defensive shaken [url=http://www.curry-shoes.com]curry shoes[/url] right after scoring started rising with his Arsenal, outside his 3-pointer by continuous, then he was given the means to just like Kevin durant got chance within the first half. After three points from the database is still attack, he this section one bomb underneath the 14 points.

Today is June 1, the time [url=http://www.kdshoes.us.com]kd shoes[/url] could be the international children's day, it seems in the "primary school" is among the holiday today.

Small garage finish I rested the vast majority of holiday to battle, he is still the contribution towards the brilliant stroke, but in addition pass a 3-pointer simply by Kevin durant. The previous 3 minutes, garage off in advance of schedule, because the activity had no suspense.

Tag: [url=http://www.kyrieirvingshoes.us.com]kyrie irving shoes[/url] [url=http://www.nikehyperdunk.us.com]nike hyperdunk[/url] [url=http://www.lebronjamesshoes.com.co]lebron james shoes[/url] [url=http://www.nikelunarforce1.com]nike lunar force 1[/url] [url=http://www.kyrie3.us]nike kyrie 3[/url] [url=http://www.lebron-james-shoes.us.com]lebron james shoes[/url] [url=http://www.ecco.us.com]ecco[/url] [url=http://www.ugg5803.com]ugg 5803[/url] [url=http://www.adidasultraboost4.com]adidas ultra boost 4[/url] [url=http://www.nikehuarache.org]nike huarache[/url] [url=http://www.canadagooseus.com]canada goose[/url] [url=http://www.bensimmonsjersey.us]ben simmons jersey[/url] [url=http://www.lebron-14.us]lebron 14[/url] [url=http://www.adidasyeezywaverunner700.com]adidas yeezy wave runner 700[/url] [url=http://www.yeezytriplewhite.com]yeezy boost triple white[/url] [url=http://www.kyrieirvingshoes.us]kyrie irving shoes[/url] [url=http://www.kobe-10.org]kobe 10[/url] [url=http://www.kyrieirvingshoes.com.co]kyrie shoes[/url] [url=http://www.kyrie-4.com]kyrie 4[/url] [url=http://www.kd-shoes.org]kd shoes[/url] [url=http://www.bapehoodie.com]bape hoodie[/url] [url=http://www.michaeljordanshoes.us]michael jordan shoes[/url] [url=http://www.curryshoes.us]curry shoes[/url] [url=http://www.barbourjackets.us.com]barbour jackets[/url] [url=http://www.airjordan32.us]air jordan 32[/url] [url=http://www.kyrie-4.org]kyrie 4 shoes[/url] [url=http://www.newbalanceshoes.us.com]new balance shoes[/url] [url=http://www.adidashardenvol2.com]adidas harden vol 2[/url] [url=http://www.mizunoshoes.us.com]mizuno running shoes[/url] [url=http://kyrieirvingjersey.com]kyrie irving jersey[/url] [url=http://www.calvinklein.us.com]calvin klein outlet[/url] [url=http://www.curry-2.com]curry 2[/url] [url=http://www.drose8.com]rose 8[/url] [url=http://www.stephencurryjersey.us]stephen curry jersey[/url] [url=http://www.nikelebronjamesshoes.us.com]Lebron James Shoes[/url] [url=http://www.rose6.us]rose 6[/url]

cheap cialis once day

cialis online

order female cialis

[url=http://cialiskkg.com/#]cialis generico online[/url]

cialis how to buy

tadalafil generic

buying cialis in london

[url=http://cialisdcfev.com/#]tadalafil generic[/url]

good place buy cialis

buy cialis uk online

generic cialis at walmart

cheap cialis forum

[url=http://cialisdskew.com/#]tadalafil generic[/url]

cialis buy paypal

buy cialis online

cheapest cialis usa

[url=http://cialisggr.com/#]cialis online[/url]

buy cialis canadian pharmacy

no 1 canadian pharcharmy online

canada pharmacy

Safe Canadian Online Pharmacies

[url=http://canadianymmgfd.com/#]canadian pharmacies online[/url]

prescriptions online

approved canadian online pharmacies

Top Rated Online Canadian Pharmacies

[url=http://pharmacyryutjfg.com/#]legitimate canadian mail order pharmacies[/url]

Trusted Online Pharmacies

canadian pharmacies

canada pharmacy

pharmacy online

[url=http://canadianymmgfd.com/#]canadian pharmacies online[/url]

canada drugs

canadian pharmacies online prescriptions

Online Drugstores

[url=http://pharmacyryutjfg.com/#]canada pharmacies online prescriptions[/url]

List of Safe Online Pharmacies

gnc diet pills that really work

[url=http://regimenforfeit.com/]weight loss pills over the counter[/url]

2017 best weight loss pills

diet pills that really work

what's the best online casino australia

online casino voor mac

cool cash bingo

[url=http://onlineroulette.space/#]live casino slot machines[/url]

live casino table games

top roulette machine

most trusted online gambling sites

[url=http://online-casino.party/#]online roulette real money[/url]

online money games australian currency

real money online casino games

play bingo for real money on ipad

[url=http://online-slots.party/#]real money online casino games[/url]

online casino club usa

cialis tablete za zene

generic cialis 2017

cheap cialis black

[url=http://cialisrydfgj.com/#]cialis generic availability[/url]

where to get cialis cheap

coupon for cialis

can you buy cialis over counter usa

[url=http://cialistiutyjdg.com/#]coupon for cialis[/url]

mail order cialis from canada

online slots casino real money

roulette kostenlos spielen

legitimate us online casinos

[url=http://onlineroulette.space/#]roulette kostenlos spielen[/url]

10 best online casino

one casino

live casino roulette

[url=http://online-casino.party/#]casino games[/url]

jackpot site

free slots online

online casinos canadian

[url=http://online-slots.party/#]free slots online[/url]

highest payout online casino slots

legitimate online casinos australia

playtech roulette

deposit rtg casino bonus

[url=http://onlineroulette.space/#]online roulette[/url]

casino high online roller

bovada casino

casino game with 2 dice

[url=http://online-casino.party/#]free online casino[/url]

real roulette

online slots

online gambling kansas

[url=http://online-slots.party/#]casino slots[/url]

baccarat internet online

cheap cialis generic india

buy cialis

order cialis no prescription online

[url=http://uttcialisstdjfxhfdj.com/#]cialis coupon 2018[/url]

cialis 20 mg for sale

generic tadalafil

daily cialis pills

[url=http://bftadalafiletuikh.com/#]tadalafil generic[/url]

cheapest way to get cialis

cialis sale london

buy cialis

cialis online sale

[url=http://uttcialisstdjfxhfdj.com/#]cialis coupon[/url]

cialis for cheap

tadalafil

cheap legitimate cialis

[url=http://bftadalafiletuikh.com/#]tadalafil price[/url]

take cialis pills

generic cialis generic cialis online [url=http://skyrank.com]buy cialis from canada[/url] buy cialis online in usa http://skyrank.com

citrato de sildenafil generico ems

viagra without a doctor

how to buy viagra safely online

[url=http://gsviagraridfj.com/#]viagra without a doctor prescription[/url]

efectos viagra 50 mg

viagra price

viagra price in lahore

[url=http://amhviagraufgk.com/#]cheap viagra[/url]

viagra online in australia cheap

buy cialis online cialis 5mg price [url=http://skyrank.com]buy cialis from canada[/url] buy cialis from canada http://skyrank.com

windows 10

win 10

how to use alarms in windows 10

[url=http://opgemmje.com/#]windows live[/url]

windows phone

get rid email viagra virus

viagra without script

viagra 12.5 mg

[url=http://gsviagraridfj.com/#]viagra without prescription[/url]

female viagra pills australia

viagra prices

best way split viagra pills

[url=http://amhviagraufgk.com/#]buy viagra[/url]

viagra online florida

windows pro

windows store

microsoft mahjong

[url=http://opgemmje.com/#]update windows 10[/url]

microsoft visio

windows live mail download

windows 10 upgrade

microsoft office

[url=http://opgemmje.com/#]windows live[/url]

where was microsoft founded

best weight loss pill

[url=http://regimenforfeit.com/]appetite suppressants that work[/url]

best diet pills for weight loss

weight loss pills

microsoft login 365

windows 10 download

video playback settings in windows 10

[url=http://opgemmje.com/#]microsoft windows[/url]

stegbar windows